Overview

As the third-largest national economy in the Eurozone, Italy has had a long history of public control of industries strategic for its economy. In its time, the public sector has been one of the most influential shareholders of companies of national interest.

Many of those (among which railways, telecommunications, gas, water and electricity providers) used to be wholly state-owned. During the 90s, at the height of privatisation (a wave partially initiated within the European Union), a law was introduced granting the State partial control through the exercise of the so-called "golden share" which, even in the case of the holding of a minority of capital, allowed it to veto certain decisions, for example, mergers.

This law was heavily criticised at the European level (and severely condemned by the European Court of Justice): it created two tiers of shareholders, allowing a potentially discriminatory practice towards the private sector, thus distorting the free market.

Ten years ago, control of strategic sectors moved in a different direction: in 2012, Italy introduced a law to safeguard areas of strategic national interest.

Law 56/12 (converting, with amendments, Decree 21/2012) was the first to grant the Government special veto powers for any transaction involving a change in control, ownership, availability or use of "strategic assets". Any such transaction required prior notification to, and approval by, the Italian Government. Without authorisation, the change in control could not go ahead. The Italian Government was reserving the right tout court to veto a change of control, and this power is known as “the golden power”.

The Italian Government was the recipient of exceptional powers concerning foreign companies that carry out activities of strategic importance, no longer limited to privatised companies and regardless of the State's ownership of relevant shareholdings.

The European Commission accepts the exercise of veto powers provided their basis is not one of economic consideration, thus distorting free movement and competition, but it is entirely motivated by reasons of higher general public interest such as order, safety or health (EU Communication C220).

The powers of intervention granted to the Government, which differ depending on the case and must align with objective and non-discriminatory criteria, are as follows:

1. opposition to the purchase of equity;

2. veto the adoption of company resolutions;

3. the imposition of specific requirements and conditions.

Evolution

The new framework of laws in Italy established limits and conditions for exercising such extraordinary powers. Several layers of laws, statutes and further regulations were the complex foundation of the overall framework.

To begin with, the “strategic assets” were within the

defence and national security sectors

, as well as in specific strategic areas in the

energy, transport and communications

sectors.

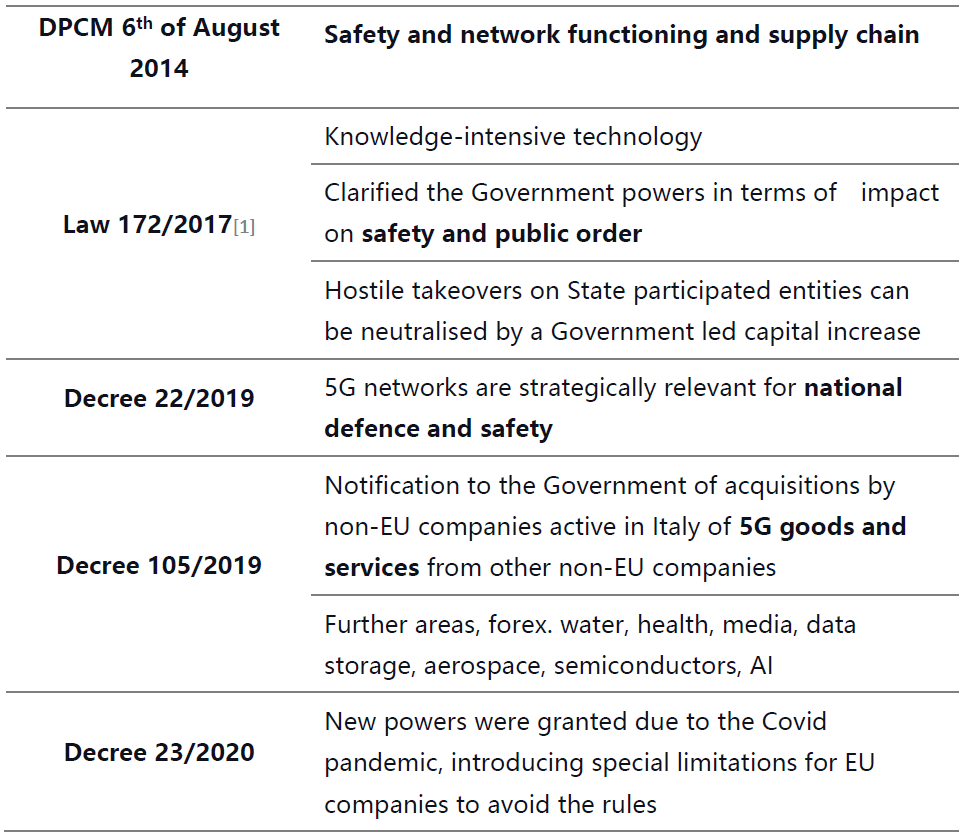

With time, more areas were added either by rule of law or by decree:

The last piece of legislation came into force on 22 March 2022, in response to the Ukrainian crisis: Governmental Decree 21/2022 introduces significant changes to the Italian regulations around foreign investment.

The innovations are both substantial, increasing the areas falling under the Golden Power perimeter, and procedural.

Overall, industry sectors subject to the golden power rules are aligned to Regulation (EU) 452/2019 (“EU Regulation”), devoted to foreign direct investment into the European Union:

1、Defence and homeland security (which also encompasses agreements relating to the development, structuring, maintenance and management of networks concerning 5G technology)

2、Communications

3、Critical infrastructures, such as energy, transportation, water, health, media, data collection, processing or storage (including cloud technology), electoral or financial infrastructure, and sensitive facilities

4、Critical technologies and dual-use items, including artificial intelligence, robotics, semiconductors, cybersecurity, energy storage, quantum computing, supply of essential inputs and nuclear technologies, as well as nanotechnologies and biotechnologies

5、Food safety, sensitive information – including personal data and its transfer – and media freedom

Other sectors, specific to Italy are finance, including credit and insurance, as well as

manufacturing, import and distribution of medical and surgical devices and personal protective equipment (PPE).

The amendments approved by Decree 21/2022 affect the foreign investment process vis-à-vis the Italian Government and somehow simplify the notification and clearance process, but tighten the requirements for specific industry sectors with increased strategic relevance as a result of the current international scenario.

Changes in control of companies in the telecommunications, energy, transport, health, agri-food and financial sectors, including credit and insurance, are now subject to the prior notification to the Presidency of the Council of Ministers regardless of the nationality of the Investor. The provision does not make allowances for EU or even Italian residents.

In the telecommunications network, sectors and broadband electronic communication services based on 5G technology together with other services, goods, relationships, activities and technologies relevant to cybersecurity (including those related to cloud technology) have been deemed in need of increased security. In those sectors, aside from asking for approval in advance, the purchaser faces a further governance cost: providing the Government with a yearly analytical plan containing a detailed description of the transaction and the technologies functional to the same, together with forecasts and modalities of development of the digitisation systems.

The procedure

Decree 21/2022 allows an investor who acquires control over an entity operating in a strategic sector to make a joint notification with the target company or invite the target to join the notification process. Should the target decide not to join, it has the possibility to present its comments within 15 days from the date of the notification to relevant authorities.

Note that a specific team of ten experts in law, economics, and international relations has been established within the Government to evaluate every transaction with the help of the financial police (Guardia di Finanza). The Government then has 45 days to decide, the outcome being (i) an explicit approval, (ii) subject to a condition, or (iii) a veto of the transaction altogether. The 45 days may be extended should there be additional information or should the EU coordination mechanism need to be completed under the EU Regulation. It is possible to approach the team requesting a preliminary evaluation of the deal, and, although their determination would not ultimately be binding for the Government, it would offer good, qualified guidance to the investor.

A transaction carried out before receiving governmental clearance or in breach is

null and void. The Government may also oblige the parties to reinstate, at their expense, the ex-ante situation with the application of criminal sanctions, should those apply.

Furthermore, an administrative monetary sanction applies up to twice as much as the value of the transaction for no less than 1% of the aggregate turnover of the last fiscal year. Sanctions apply to both the investor and the target.

What next?

The introduction of such tight measures is mainly due to the fact that foreign acquisitions have grown exponentially in the past few years. In 2021 the total number was 496: 22 were approved upon conditions and 2 vetoed. 2022 has seen a more prudent approach by the authorities with cross-examination requests and increasing financial police investigations on present and past deals.

The new, more stringent regime transpires clearly from the provisions of the recent Government Decree 21/2022. Government decrees are urgent measures that must be converted into law by Parliament within 60 days from their entry into force. The expectation is for a timely conversion into law, possibly with amendments and even more demanding requirements.

The pandemic and the current geopolitical crisis have heightened the need to enlarge and scrutinise strategic sectors. While this can be rational at a political level, it is undoubtful that deals’ structures will have to be reconsidered due to the stiff obligations and rigorous compliance requests with, in some sectors, the increase of recurrent obligations and governance costs. Therefore, it will be necessary to be aware of the new timelines at the outset of the project and of the political risks attached.

【Endnote】

[1] Law 4 December 2017, n. 172, converting Law Decree 16 October 2017, n.148.

As the third-largest national economy in the Eurozone, Italy has had a long history of public control of industries strategic for its economy. In its time, the public sector has been one of the most influential shareholders of companies of national interest.

Many of those (among which railways, telecommunications, gas, water and electricity providers) used to be wholly state-owned. During the 90s, at the height of privatisation (a wave partially initiated within the European Union), a law was introduced granting the State partial control through the exercise of the so-called "golden share" which, even in the case of the holding of a minority of capital, allowed it to veto certain decisions, for example, mergers.

This law was heavily criticised at the European level (and severely condemned by the European Court of Justice): it created two tiers of shareholders, allowing a potentially discriminatory practice towards the private sector, thus distorting the free market.

Ten years ago, control of strategic sectors moved in a different direction: in 2012, Italy introduced a law to safeguard areas of strategic national interest.

Law 56/12 (converting, with amendments, Decree 21/2012) was the first to grant the Government special veto powers for any transaction involving a change in control, ownership, availability or use of "strategic assets". Any such transaction required prior notification to, and approval by, the Italian Government. Without authorisation, the change in control could not go ahead. The Italian Government was reserving the right tout court to veto a change of control, and this power is known as “the golden power”.

The Italian Government was the recipient of exceptional powers concerning foreign companies that carry out activities of strategic importance, no longer limited to privatised companies and regardless of the State's ownership of relevant shareholdings.

The European Commission accepts the exercise of veto powers provided their basis is not one of economic consideration, thus distorting free movement and competition, but it is entirely motivated by reasons of higher general public interest such as order, safety or health (EU Communication C220).

The powers of intervention granted to the Government, which differ depending on the case and must align with objective and non-discriminatory criteria, are as follows:

1. opposition to the purchase of equity;

2. veto the adoption of company resolutions;

3. the imposition of specific requirements and conditions.

Evolution

The new framework of laws in Italy established limits and conditions for exercising such extraordinary powers. Several layers of laws, statutes and further regulations were the complex foundation of the overall framework.

To begin with, the “strategic assets” were within the

defence and national security sectors

, as well as in specific strategic areas in the

energy, transport and communications

sectors.

With time, more areas were added either by rule of law or by decree:

The last piece of legislation came into force on 22 March 2022, in response to the Ukrainian crisis: Governmental Decree 21/2022 introduces significant changes to the Italian regulations around foreign investment.

The innovations are both substantial, increasing the areas falling under the Golden Power perimeter, and procedural.

Overall, industry sectors subject to the golden power rules are aligned to Regulation (EU) 452/2019 (“EU Regulation”), devoted to foreign direct investment into the European Union:

1、Defence and homeland security (which also encompasses agreements relating to the development, structuring, maintenance and management of networks concerning 5G technology)

2、Communications

3、Critical infrastructures, such as energy, transportation, water, health, media, data collection, processing or storage (including cloud technology), electoral or financial infrastructure, and sensitive facilities

4、Critical technologies and dual-use items, including artificial intelligence, robotics, semiconductors, cybersecurity, energy storage, quantum computing, supply of essential inputs and nuclear technologies, as well as nanotechnologies and biotechnologies

5、Food safety, sensitive information – including personal data and its transfer – and media freedom

Other sectors, specific to Italy are finance, including credit and insurance, as well as

manufacturing, import and distribution of medical and surgical devices and personal protective equipment (PPE).

The amendments approved by Decree 21/2022 affect the foreign investment process vis-à-vis the Italian Government and somehow simplify the notification and clearance process, but tighten the requirements for specific industry sectors with increased strategic relevance as a result of the current international scenario.

Changes in control of companies in the telecommunications, energy, transport, health, agri-food and financial sectors, including credit and insurance, are now subject to the prior notification to the Presidency of the Council of Ministers regardless of the nationality of the Investor. The provision does not make allowances for EU or even Italian residents.

In the telecommunications network, sectors and broadband electronic communication services based on 5G technology together with other services, goods, relationships, activities and technologies relevant to cybersecurity (including those related to cloud technology) have been deemed in need of increased security. In those sectors, aside from asking for approval in advance, the purchaser faces a further governance cost: providing the Government with a yearly analytical plan containing a detailed description of the transaction and the technologies functional to the same, together with forecasts and modalities of development of the digitisation systems.

The procedure

Decree 21/2022 allows an investor who acquires control over an entity operating in a strategic sector to make a joint notification with the target company or invite the target to join the notification process. Should the target decide not to join, it has the possibility to present its comments within 15 days from the date of the notification to relevant authorities.

Note that a specific team of ten experts in law, economics, and international relations has been established within the Government to evaluate every transaction with the help of the financial police (Guardia di Finanza). The Government then has 45 days to decide, the outcome being (i) an explicit approval, (ii) subject to a condition, or (iii) a veto of the transaction altogether. The 45 days may be extended should there be additional information or should the EU coordination mechanism need to be completed under the EU Regulation. It is possible to approach the team requesting a preliminary evaluation of the deal, and, although their determination would not ultimately be binding for the Government, it would offer good, qualified guidance to the investor.

A transaction carried out before receiving governmental clearance or in breach is

null and void. The Government may also oblige the parties to reinstate, at their expense, the ex-ante situation with the application of criminal sanctions, should those apply.

Furthermore, an administrative monetary sanction applies up to twice as much as the value of the transaction for no less than 1% of the aggregate turnover of the last fiscal year. Sanctions apply to both the investor and the target.

What next?

The introduction of such tight measures is mainly due to the fact that foreign acquisitions have grown exponentially in the past few years. In 2021 the total number was 496: 22 were approved upon conditions and 2 vetoed. 2022 has seen a more prudent approach by the authorities with cross-examination requests and increasing financial police investigations on present and past deals.

The new, more stringent regime transpires clearly from the provisions of the recent Government Decree 21/2022. Government decrees are urgent measures that must be converted into law by Parliament within 60 days from their entry into force. The expectation is for a timely conversion into law, possibly with amendments and even more demanding requirements.

The pandemic and the current geopolitical crisis have heightened the need to enlarge and scrutinise strategic sectors. While this can be rational at a political level, it is undoubtful that deals’ structures will have to be reconsidered due to the stiff obligations and rigorous compliance requests with, in some sectors, the increase of recurrent obligations and governance costs. Therefore, it will be necessary to be aware of the new timelines at the outset of the project and of the political risks attached.

【Endnote】

[1] Law 4 December 2017, n. 172, converting Law Decree 16 October 2017, n.148.