Since the People’s Bank of China (“PBOC”) issued the PBOC Announcement [2016] No. 3 (“Announcement [2016] No. 3”) in February 2016 to deepen the opening-up of China Interbank Bond Market (“CIBM”), more and more overseas institutions have participated in the CIBM investment via different routes and schemes. In April 2019, RMB-denominated Chinese government bonds and policy bank bonds were officially included in the Bloomberg Barclays Global Aggregate Index (BBGA); from February 2020, nine Chinese government bonds were included in the JPMorgan Government Bond Index - Emerging Markets (GBI-EM) flagship series; from October 2021, RMB government bonds were officially included in the FTSE World Government Bond Index (WGBI), and the weighting will be increased in stages over 36 months after that. From then on, Chinese bonds have been included in the three major global bond indices, which marks a new milestone in the opening-up of China’s bond market on the one hand, and, on the other, further boosts the foreign holdings of Chinese bonds. The figures reveal that the number of overseas institutions allowed to invest in the CIBM has risen from 373 at the end of October 2016 to 1,071 at the end of November 2022, and the bond depositary balance held by overseas institutions has increased from about RMB630.63 billion at the end of April 2016 to RMB3.33 trillion at the end of November 2022. Both of the number of overseas institutions and the volume of bonds held by them have risen significantly over the past six years.

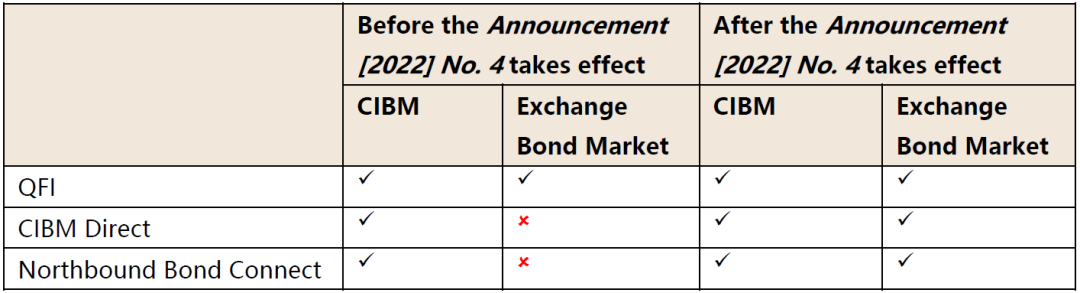

China’s bond market is dominated by the CIBM and the exchange bond market, and supplemented by the commercial bank over-the-counter bond market. Prior to the new policy in 2022 (as described below), the routes available to overseas commercial institutional investors (“OII”) investing in CIBM include qualified foreign institutional investor (“QFI”), CIBM Direct and Northbound Bond Connect, while the only way for OIIs to invest in the exchange bond market is QFI. In 2022, PBOC and the State Administration of Foreign Exchange (“SAFE”) issued certain new rules on coordinating the opening-up of China’s bond market (including the CIBM and the exchange bond market) to further facilitate the investments by OIIs and enhance the attractiveness of China’s bond market to OIIs, which include (i) the Joint Announcement [2022] No. 4 on matters relating to further facilitating OIIs’ investment in China’s bond market (“Announcement [2022] No. 4”) issued by PBOC, the China Securities Regulatory Commission (“CSRC”) and SAFE on 27 May 2022 and effective from 30 June 2022, and (ii) the Rules on Funds Invested by Overseas Institutional Investors in China’s Bond Market (“Rules on Funds Invested by OIIs in Bond Market”) jointly issued by PBOC and SAFE on 18 November 2022 and effective from 1 January 2023. With the continuation of the scope of investors under the Announcement [2016] No. 3, the Announcement [2022] No. 4 is a pioneering move to simultaneously coordinate and promote the interconnectivity between the CIBM and the exchange bond market as well as their opening-up, extending the investment scope of OIIs allowed to enter into the CIBM to the exchange bond market and thus realizing the expanded opening-up of the exchange bond market. According to the Announcement [2022] No. 4, OIIs can enter into the exchange bond market by virtue of the CIBM filing with PBOC, and no separate approval from CSRC is required. As a supporting policy to the Announcement [2022] No. 4, the Rules on Funds Invested by OIIs in Bond Market integrates previous foreign exchange (“FX”) management requirements and further unifies and standardizes the management of OIIs’ cross-border capital flow, which has come into effect on 1 January 2023. The following is our review of the opening-up policy of China’s bond market based on the Announcement [2022] No. 4 and the Rules on Funds Invested by OIIs in Bond Market, and our outlook for more measures to deepen the opening-up.

Review of 2022

I Building up the Entity-based Filing

On 8 March 2021, the Financial Market Management Department of the PBOC Shanghai Head Office issued the Notice on Updating the Investment Filing Form for Overseas Institutions, stating that OIIs only need to file once in the name of the institution; on 19 March 2021, the PBOC General Administration Department issued the Notice on Further Optimizing the Services for the Opening-up of Interbank Bond Market Infrastructures and Strengthening the In-process and Post Management, requiring that China Foreign Exchange Trade System & National Interbank Funding Center (“CFETS”) shall optimize the trading service and support OIIs to apply for the entity-based networking and conclude transactions with counterparties in the name of the investment manager. The Q&A of the Announcement [2022] No. 4 reemphasizes that OIIs should enter into the CIBM in the name of legal persons, and there is no need to conduct the PBOC filing for new products on a product-by-product basis, regardless of whether they are the products of the existing CIBM investors or those investors which are about to enter into the CIBM. Similarly, FX registration is also conducted at the entity level, and it is not required to apply for FX registration for each product individually.

II Expanding the Scope of OIIs Investing in the Exchange Bond Market

More eligible OIIs can participate in the exchange bond market under the Announcement [2022] No. 4. Specifically, the route for OIIs’ participation in the exchange bond market is no longer limited to QFI, and those allowed to participate in the CIBM Direct and Northbound Bond Connect can invest in the exchange bond market directly or through the mutual market access scheme between the CIBM and the exchange bond market (“Interbank-Exchange Bond Connect”).

1. Direct investment in the exchange bond market

In order to facilitate and regulate OIIs’ direct investment in the exchange bond market and to coordinate the implementation of the Announcement [2022] No. 4, Shanghai Stock Exchange (“SSE”) and Shenzhen Stock Exchange (“SZSE”) respectively formulated the implementation rules on bond trading, registration and settlement for OIIs with China Securities Depository and Clearing Corporation Limited (“CSDC”). In accordance with such implementation rules,

(1) OIIs can directly participate in the exchange bond market in the name of legal persons, and directly open securities accounts at CSDC based on the CIBM filing certificates from PBOC;

(2) OIIs shall appoint qualified commercial banks as custodians, appoint domestic securities companies with SSE/SZSE membership as trading participants to participate in bond trading, and appoint domestic securities companies with CSDC settlement participant qualification to handle the settlement;

(3) OIIs can participate in the subscription, trading or transfer of bonds (including exchangeable corporate bonds and convertible corporate bonds), asset-backed securities, bond lending, derivatives for risk management purposes, bond funds and other products in the exchange bond market;

(4) OIIs can conduct the two-way non-trading transfers of bonds and other varieties between their securities accounts and their QFI securities accounts based on their needs for portfolio management.

2. Investment in the exchange bond market through the Interbank-Exchange Bond Connect

In accordance with the Interim Measures for the Connectivity Business between the Interbank Bond Market and the Exchange Bond Market, OIIs can, after the realization of interconnectivity between the CIBM and the exchange bond market, invest in the exchange bond market via the Exchange-bound Connect under the Interbank-Exchange Bond Connect.

III Exploring the Multi-level Custody Model for Custodian Banks

The Announcement [2022] No. 4 proposes to study and explore the establishment of a sound institutional arrangement for multi-level custody (“Custodian Bank Model”), with the settlement agency model and the Custodian Bank Model running in parallel for OIIs to select. Under the Custodian Bank Model, OIIs can, directly or through their global custodian banks, appoint eligible domestic custodian banks for bond depositary services. Bonds purchased by OIIs through domestic custodian banks shall be registered in the name of the domestic custodian banks, and OIIs shall be entitled to the rights and interests in the bonds according to the law. In order to ensure the OIIs’ asset safety, the Announcement [2022] No. 4 requires domestic custodian banks to establish and enhance relevant mechanisms to strictly segregate OIIs’ assets under their custody from the domestic custodian banks’ proprietary assets and all the other assets under their custody, and to effectively perform their independent custody duties.

The multi-level custody model is not an initiative, and has been practiced in the areas of commercial bank over-the-counter bond market, cross-market transfer of depository of bonds and the Bond Connect[1]. We observe that for investment funds in many offshore jurisdictions, the trustee/depositary is responsible for appointing a global custodian, which in turn appoints a sub-custodian based on the custody agreement with the local custodian. Exploring the development of the Custodian Bank Model will facilitate OIIs’ access to the CIBM with no change to their original trading habits and modes, which will allow them to rely on the existing custodian network of the trustee/depositary to enter into the CIBM without having to appoint a separate settlement agent and create new legal relationships.

IV Optimizing the Consistency Management of Inbound and Outbound Currencies

The Rules on Funds Invested by OIIs in Bond Market requires OIIs to maintain, in principle, the same currency when remitting and repatriating funds for investment in China’s bond market, and not to engage in arbitrage between the RMB and any foreign currency. Starting from 1 January 2023, please be attentive to the following when remitting funds out of China according to the Rules on Funds Invested by OIIs in Bond Market:

1. if OIIs only remit funds in RMB for investment, the outbound remittance should be in RMB with no percentage limitation;

2. if OIIs only remit funds in foreign currency for investment, the outbound remittance should be in foreign currency with no percentage limitation;

3. if OIIs remit funds in both RMB and foreign currency for investment, the amount of accumulated outward remittance in foreign currency shall not exceed 1.2 times the accumulated inward remittance in foreign currency (except for the bond investment liquidation). The above restriction can be relaxed as appropriate for OIIs with the aim of engaging in long-term investment in China’s bond market.

The principle of maintaining the consistency between inbound and outbound currencies is to avoid currency arbitrage due to the currency exchange. From the initial requirement that “the ratio of RMB to foreign currency in the OII’s accumulated outward remittance shall basically be in-line with that of the accumulated inward remittance, with a maximum permissible deviation of 10%” to the current requirement that “the amount of accumulated outward remittance in foreign currency shall not exceed 1.2 times the accumulated inward remittance in foreign currency”, this optimization can effectively satisfy the remittance needs of OIIs and further encourage OIIs to actively invest in China’s bond market from the perspective of facilitating their capital remittance.

V Enhancing the Management of Spot Purchase and Sale of FX and FX Risk

The Rules on Funds Invested by OIIs in Bond Market consolidates the Circular of the State Administration of Foreign Exchange on the Improvement of Foreign Exchange Risk Management by Overseas Institutional Investors in the Interbank Bond Market (Huifa No. 2 [2020]) and the related Policy Q&A, and further improves and optimizes the management of spot FX purchase and sale and FX risk. In particular, there is no more restriction on the number of domestic financial institutions with which OIIs may enter into spot FX purchase and sale and FX derivative transactions. OIIs that carry out spot FX purchase and sale and FX derivative transactions can choose to trade directly with domestic financial institutions, or become a CFETS member and enter into prime brokerage to trade in the interbank FX market. If the OII is a banking institution, it may additionally choose to become a CFETS member to directly trade in the interbank FX market.

Outlook for 2023

The report to the 20th National Congress of the Communist Party of China mentions that China will promote high-standard opening-up and RMB internationalization in an orderly way. The opening-up of the bond market is an integral part of the RMB internationalization, and they are complementary to each other. The opening-up of the bond market will attract more offshore investors to hold more RMB assets and promote RMB internationalization, and RMB internationalization will in turn enhance the attractiveness of RMB bonds and deepen the opening-up of China’s bond market. Looking ahead, we believe there will be more measures and policies to deepen the development of China’s bond market, and we are looking forward to the early realization of the Custodian Bank Model, the launch of the Swap Connect as scheduled, the official implementation of the Interbank-Exchange Bond Connect in the coming year.

【Endnote】

[1] In the custody model of commercial bank over-the-counter bond market, investors open secondary depositary accounts at commercial banks to keep track of their bond holdings and changes therein; commercial banks open omnibus accounts (primary depositary accounts) at the bond registration, depositary and settlement institution to record the total amount of bonds held for their secondary customers. Under this model, the Measures for the Administration of Over-the-Counter Business in the National Interbank Bond Market imposes the requirement on assets segregation, requiring commercial banks to strictly separate their own bonds from the bonds held in custody for investors and not to misappropriate investors’ bonds.

Review and Outlook - Opening-up Policies for Bond Market in 2022

作者:SandraLu LilyLuo ElaineWang来源:通力律师

Since the People’s Bank of China (“PBOC”) issued the PBOC Announcement [2016] No.