中国企业“走出去”境外投资并购:

Outbound Investment by Chinese Enterprises:

对外投资概况、交易流程及架构、挑战及策略

Outbound Investment Overlook, Transaction Planning and Structuring, Challenges and Strategies

第一部分中国企业“走出去”境外投资并购:

Part 1 Outbound Investment by Chinese Enterprises:

对外投资概况、交易流程及架构、挑战及策略 Outbound Investment Overlook, Transaction Planning and Structuring, Challenges and Strategies

目录

目录第一节 关于大成

Section 1 About Dentons

第二节 投资概况 ———

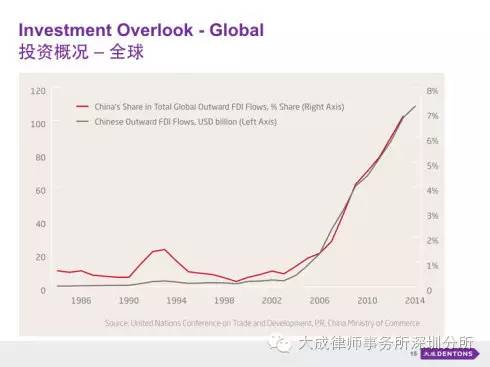

Section 2 Investment Overlook - Global

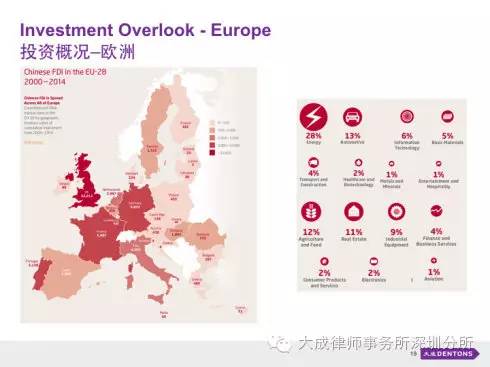

投资概况 –全球

China`s global foreign assets currently amountto US$ 6.4 Trillion

中国的全球外汇资产总计达6.4万亿美元

Assuming full convertibility of the RMB by 2020, China‘s global foreign assets are expected to amount to US$ 18 Trillion by 2020

至2020年,假设人民币完全可兑换,中国的全球外汇资产预计可达18万亿美元

Outward Foreign Direct Investment by Chinese enterprises is currently at an annual level of more than US$ 100 Billion

当前中国企业境外直接投资年均为1000亿美元以上

Investment focus is shifting from natural resources in developing countries to high-tech industry and real estate in developed countries

投资焦点从发展中国家的自然资源转向发达国家的高科技工业和不动产领域

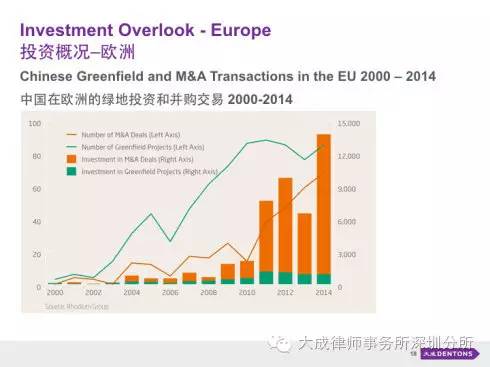

Between 2009 and 2014 the volume of Chinese OFDI in Europe has quadrupled.

在2009至2014年间,中国对外直接投资总量翻了两番

Between 2012 and 2013 the volume of Chinese OFDI in Europe has doubled

在2012至2013年间,中国在欧洲的对外直接投资翻倍

In 2015 company acquisitions/participations by Chinese investors in Europe have reached an all time high.

2015年,中国投资者在欧洲的并购和参股创造了新高

In the first quarter of 2016 the volume of Chinese OFDI in Europe has already reached US$ 53.8 Billion (due to the US$ 43 Billion acquisition of Syngenta by China National Chemical Corporation)

2016年第一季度,中国在欧洲的对外直接投资已经达到538亿美元(归因于中国化工集团对先正达430亿美元的收购)

Chinese Greenfield and M&A Transaction in the EU 2000 – 2014

中国在欧洲的绿地投资和并购交易 2000-2014

The Chinese government encourages Chinese companies to investabroad in order to operate more competitively in the global market.

走出去:中国政府鼓励中国企业去国外投资使其在全球市场中更有竞争力。

The Chinese government promotes investments particularly in technology companies (mechanical engineering, automotive, renewable energies, information technology) to acquire technical know-how and to become market leader in core industries.

中国政府促进对德国的技术公司(机械工程、汽车工业、再生能源、信息科技)进行投资,尤其是获得技术知识从而成为核心产业市场的领导者。

Especially private equity companies will increasingly open up to strategic Chinese investors in the next years.

在未来数年,特别是德国的私人股权公司将加快开放给中国的战略投资者。

Germany is the second-largest recipient of Chinese OFDI in Europe (after the United Kingdom)

德国是欧洲第二大接收中国对外直接投资最多的国家(位于英国之后)

Total investments by Chinese enterprises in Germany between 2000 to 2014 amount to appr. € 6.9billion

2000至2014年间中国企业在德国投资总额合计约69亿欧元

Chinese OFDI in Germany have significantly increased since 2011, reaching a stable level of € 1 – 2 billion annually in the last years

中国在德国的境外直接投资在2011年之后显著增长,最近几年达到了每年10至20亿欧元的稳定增长水平

Chinese investors are focusing on Germany‘s advanced manufacturing companies: automotive and industrial equipment account for more than 65 per cent of total Chinese investments since 2000.

中国投资者聚焦于德国的高端制造企业:自2000年以来,汽车和工业装备行业占据中国总投资额的65%

Germany is and will remain one of the most popular destination in Europe for Chinese investors seeking investment opportunities

德国是并将保持作为寻求海外投资机会的中国投资者在欧洲的首选之地

Excellent reputation of German brands ("Made in Germany")

“德国制造”的良好品牌信誉

Access to key industries (automotive,information technologies, mechanical engineering, renewableenergies)

德国企业在基础工业中强有力的竞争力支持(汽车工业、信息技术、机械工程、可再生能源)

Access to highly developed distribution and sales networks in Germany and Europe

德国企业在德国和欧洲拥有高度发达的分销和销售网络

Trade between Germany and China has increased substantially over the last decade - China is now Germany’s fourth main trading partner (after France, the UK and the US)

过去十年里中德贸易显著增长。中国目前是德国第四大贸易合作伙伴(仅次于法国、英国与美国)

Chinese investors are particularly interested in German small- and medium-sized companies with high-quality technology assets. Such investments are beneficial for both parties.

中国投资者对德国高质量技术资产型的中小型公司特别感兴趣。这样的投资对双方都有益处。

German companies gain access to an established distribution network in China.

德国公司获得并建立在中国的分销网络。

German family-owned businesses can solve the succession problem.

德国家族企业能解决继承问题。

Chinese companies acquire advanced German technology and know-how as well as access to the German market.

中国公司收购德国先进技术以及深入德国市场的技术诀窍。

Section 3 Planning and Structuring of the Transaction

第三节 交易安排与结构设计

Planning and Structuring of the Transaction 交易安排与结构设计 A typical M&A process has three phases:

一个典型的并购有以下三个阶段:

Preparation 准备

Implementation 执行

Post Closing 交割后续工作

These phases are not distinct – there is an overlap!

以上步骤并非独立而是交错进行的。

Phase I: Preparation 阶段一:准备

Analysis and Identification of: 分析并辨识:

Objectives of the Transaction 交易目的

Competitors 竞争者

Potential Targets 潜在标的

Potential Economies of Scale 潜在经济规模

Determination / Finalisation of Financing Structure 决策/最终确定融资结构

Determination / Finalisation of Buyer‘s Holding / Tax Structure 决策/最终确定买方持股数额/税务结构

Phase II: Implementation (I) 阶段二:执行

Agreement on Confidentiality 保密协议

Agreement on Exclusivity (potentially also at later stage) 排他性协议(也可能出现在之后的阶段)

Due Diligence and Valuation of Target 尽职调查与标的评估

Agreement on the Fundamental Aspects of the Transaction (Purchase Price, Transaction Structure) 交易的框架协议(购买价格、交易结构)

Execution of Letter of Intent / Memorandum of Understanding 执行意向书/谅解备忘录

Remedying of issues discovered during Due Diligence 解决尽职调查中发现的问题

Contract Negotiations 合同谈判

Signing and Closing 签署与交割

Phase III: Post Closing

阶段三:交割后续工作 Planning

of Integration Process 融合进程规划

Integration at every level of the Target 目标公司各层面的融合

Legal Restructuring of Target and Target‘s Affiliates 标的及标的关联公司的法律重组

Post Merger Audit 并购后的审计

Verificiation of Achievement of Objectives 验证目标是否实现

Section 4 Principal Challenges of an OFDI

第四节 对外直接投资的主要挑战

Principal Challenges of an OFDI 对外直接投资的主要挑战

1.Identification of the target 寻找目标公司

Knowledge of the market and important players 洞察市场环境,发现重要的竞争者

Current reluctance to sell (Inflation scare /Euro crisis)目前缺乏愿意出售的意愿(通胀恐慌/欧元危机)

Considering distressed/insolvent enterprises: low acquisition cost vs.turn-around investment

考虑面临困境或破产的企业:低并购成本vs.扭转局面的投资

2.Concerns and Perceptions at the Seller /Target (I) 关注并理解卖方/标的(1)

There are perceptions and concerns that might refrain sellers from seriously considering a sale to a Chinese company:

某些理解与认知可能会让卖方避免认真考虑向一家中国公司进行出售:

Buyer’s motivation unclear 买方动机不明确 Process might only be an information gatheringexercise 过程可能只为收集信息

Chinese buyer might be interested only in portion of the target’s business and/or assets 中国买方可能只对节标的业务及/或资产感兴趣

Motivation and final decision might be depend on, or be influenced by, Chinese authorities 动因或最终决策可能依赖于或受到中国政府机构影响

Chinese buyer might not deliver on all objectives of the seller / target (transaction reliability, target growth strategy, protection of target’s business)

中国买方可能不兑现卖方/目标公司的所有目标(交易可靠性、目标成长战略、保护 标的业务)

3.Due Diligence (analysis of corporate history, tax, finance, employment and pending litigation) 尽职调查(公司历史,税务,财务,劳动雇佣以及未决诉讼的分析)

Files in a foreign language 用外语作文件归档

Local management may not be fluent in English 本地管理层很可能无法流利的用英语交流

Documentation may be incomplete and/or outdated 资料可能不完整和/或已过时

4.Acquisition Structure 并购方式 Share Deal - Rule 股权并购 -规则

Asset Deal -Exception 资产并购 - 例外

5. Post closing integration 并购后的整合

Interaction with local management 与地方管理的互动

Different management cultures 管理文化的差异

Cultural barriers 文化障碍

Communication - Language proficiency 交流 -语言能力

Complexity and rigidity of European tax, labour and social laws 欧洲税法,劳动法和社会法复杂且严格

Different accounting standards 不同的会计准则

Section 5 Strategies for Chinese Investors

第五节 中国投资者策略

Determine a strategy, objectives and motivation for a M&A Investment in Europe

为一项欧洲并购投资确定战略、目标及动机

Build relationships with relevant market participants (professional service providers, M&A advisors, industry associations, poitical institutions)

与相关市场参与者建立关系(专业的服务提供商、并购咨询师、行业协会、政治团体)

Get in touch with the market and potential target companies pro-actively (i.e. not necessarily with a view to an immediate acquisition), e.g. during trade fairs

积极主动地接触市场及潜在的目标公司(即不一定立即收购),如在交易会期间

Make yourself familiar with specific legal issues and structures (co-determination, employee protection, tender offer procedures)

熟悉特殊的法律问题及结构(共同决策制、劳工保护、招标程序等)

Once you have identified a suitable target,start building a relationship to the decision makers at the seller(s). Present your company‘s strengths!

一旦确定一个合适的目标公司,即刻与卖方的决策者建立管理。保持公司优势!

Present a clear concept about your plans for the target and the advantages of the acquisition

向目标公司清晰陈述您的计划以及并购优势

Make an effort to convince everybody at the target: management, employees, works council, trade unions, other shareholders

努力说服目标公司的每个人:管理层、员工、 劳资委员会、工会、其他股东

Make sure that the banks and other main creditors of the target are supportive

确信得到目标公司的银行及其他主要的贷款人的支持

Find a European representative or adviser (to be placed at or close to the target) to build trust and facilitate communication

寻找一个欧洲代表或顾问(放置于或接近目标公司)建立信任、促进沟通

第二部分:跨境并购协议之条款设计要点:中国律师视角

Part 2: Drafting an Outbound M&A

Contract: Chinese Lawyers' Perspective

第一节 排他交易条款

Section 1 No solicitation Clause

排他交易条款:释义与目的

Solicitation Clause: Definition &purpose A no-shop clause is a clause in an agreement between a seller and a potential buyer that bars the seller from soliciting a purchase proposal from any other party. In other words, the seller cannot "shop" the business or asset around once a letter of intent or agreement in principle is entered into between the seller and the potential buyer. A no-shop clause is generally only in effect for a finite period.

排他交易条款是并购交易中买方为潜在卖方设置的障碍,使卖方不能与任何第三方谈判相同或相似交易。换句话说,卖方在与潜在买方签订并购意向书后不能主动“招揽”交易。排他交易条款的约束通常是时间限制的。

Source: Investopedia

买方积极寻找第三方买家 (Market Canvas):禁止(NO Shop) 第三方主动加入交易竞争(Passive Market Test):允许上市公司管理层的信托责任(Fiduciary Duty)

忠诚义务(Duty of Loyalty):将股东利益放在第一位勤勉义务(Duty of Care):“谨慎的理性人”标准(Reasonable prudent person)判断目标公司管理层是否已尽到信托责任的标准:看交易对股东而言是否“最划算”,“最划算”:综合考虑交易价格和成交几率

Fiduciary Out条款:即使在签署并购条款之后,买方如果收到来自第三方的更优报价,则买方董事有权与该第三方进行接触并在与第三方达成协议的情况下终止原收购协议。

排他交易条款:示例 No Solicitation Clause: Sample Section 4.2 No solicitation Section 4.2(a) Starwood shall not: (i) solicit any inquiries regarding any

proposal the consummation of which would constitute a Starwood Alternative Transaction; or (ii) participate in any discussions or negotiations with any person with respect to any such inquiries, provided, however, that if, at any time prior to obtaining the Starwood Stockholder Approval, the Board of Directors of Starwood determines in good faith that any such proposal that did not result from a breach of this Section 4.2(a) constitutes or is reasonably likely to lead to a Starwood Superior Proposal, subject to compliance with Section 4.2(c), Starwood and its Representatives may (A) furnish information to the person making such proposal and (B) participate in discussions or negotiations with the person making such proposal.

在签署并购协议后,喜达屋不可以主动向潜在第三方买家洽谈交易,也不可以与潜在第三方买家进行任何商谈,除非,在喜达屋股东会投票通过与万豪的合并之前,喜达屋董事会收到一个“不请自来”第三方要约,并且喜达屋董事会决定该第三方要约可能构成一个更优报价。

资料来源 Sources:"Agreement and Plan of Merger Between Marriott and Starwood" SEC. SEC, 15 Nov. 2015. Web.15 Nov. 2015. Section 4.2(b) In the event that prior to obtaining the Starwood Stockholder Approval, the Board of Directors of Starwood determines in good faith, after it has received a Starwood Superior Proposal that the failure to do so would be inconsistent with its duties under Applicable Law, the Board of Directors of Starwood may terminate this Agreement in order to enter into a definitive agreement providing for such Starwood Superior Proposal, but only:(i) at a time that is after (x) the 5th business day following Marriott’s receipt of written notice from Starwood advising Marriott that the Board of Directors of Starwood has received a Starwood Superior Proposal specifying the material terms and conditions of such Starwood Superior Proposal, identifying the person making such Starwood Superior Proposal and stating that it intends to terminate this Agreement and (y) Starwood has negotiated in good faith with Marriott during such 5 business day period with respect to any revisions to this Agreement proposed by Marriott in response to the Starwood Superior Proposal and (ii) following the Board of Directors of Starwood having taken into account any changes to the terms of this Agreement proposed by Marriott and any other information provided by Marriott in response to such notice; provided that in the event of a subsequent modification to the material terms and conditions of such Starwood Superior Proposal, a new notice shall be delivered and a period of negotiation commenced, which period shall be 3 business days.

4.2(b)明确喜达屋董事会在收到第三方更优报价的情况下,董事会可以终止与万豪的并购协议并与该第三方签订新的并购协议。但是,在终止与万豪的并购协议之前,喜达屋必须履行4.3(c)下的通知义务通知万豪,并且在通知后的5天内继续与万豪就万豪修改的并购方案进行谈判。在这5天的谈判期间中,万豪可以选择修改并购方案,使其方案比第三方的报价更优。

万豪修改并购方案后,第三方也可以重新修改并购方案,使其重新满足更优报价的定义。如果第三方再次修改,则上述的5天谈判期变为3天。

资料来源 Sources:"Agreement and Plan of Merger Between Marriott and Starwood" SEC. SEC, 15 Nov. 2015. Web.15 Nov. 2015. Section 4.2(c) Starwood shall promptly, and in any event within 24 hours of receipt thereof, advise Marriott orally and in writing if Starwood receives any proposal relating to a Starwood Alternative Transaction, and Starwood shall keep Marriott

reasonably informed of the status of any such proposal (including any material changes, modifications or amendments thereto).

喜达屋应该在收到任何与此次交易相关的意向书时,在24小时之内以书面或口头的形式及时告知万豪。喜达屋应该让万豪持续获悉一切与关系到交易进展相关的第三方意向书等信息(包括任何重大变化、修改等)。

资料来源 Sources:"Agreement and Plan of Merger Between Marriott and Starwood" SEC. SEC, 15 Nov. 2015. Web.15 Nov. 2015.

SECTION 8.3 Definitions “Superior Proposal” A “Starwood Superior Proposal” means any bona fide written proposal (on its most recently amended or modifiedterms, if amended or modified) made by a Starwood Third Party to enter into a Starwood Alternative Transaction that (1) did not result from a breach of Section 4.2(a), (2) is on terms that

the Board of Directors of Starwood determines in good faith to be more favorable from a financial point of view to Starwood’s stockholders than the transactions contemplated by this Agreement, taking into account all relevant factors (including any changes to this Agreement that may be proposed by Marriott) and (3) that the Board of Directors of Starwood determines in good faith is reasonably likely to be completed, taking into account all financial, regulatory, legal and other aspects of such proposal.

更优报价需满足3个要求:(1) Starwood只能是被动等更优报价,而不能主动招揽,否则不成立更优报价。(2) Starwood董事会必须认为,对Starwood股东而言,更优报价下的交易比Marriott提出的并购更“划算”。明确Marriott若是提议修改并购方案,则Starwood董事会必须用修改后的并购方案与更优报价进行比较。(3) Starwood董事会必须认为更优报价是有可行性的。

资料来源 Sources:"Agreement and Plan of Merger Between Marriott and Starwood" SEC. SEC, 15 Nov. 2015. Web.15 Nov. 2015.

排他交易条款:设计要点 No Solicitation Clause: Key Issues 明确目标公司不主动招揽第三方原则(No Shop) 明确目标公司可以与第三方商谈的情形(Fiduciary Out)

明确第三方“更优报价”(Superior Proposal)必须具有“可行性” 明确买方可以修改并购方案阻却第三方“更优报价”(Superior Proposal)及时通知义务:目标公司收到任何意向书都需要在短时间(比如24小时)内通知买方第三方更优报价出现——买方修改并购方案(谈判期如5天)——第三方可以修改并购方案使其继续满足“更优报价”(谈判期如3天)

第二节对赌条款

Section 2 Value Adjustment

Mechanism Clause 对赌条款:释义和目的

VAM Clause: Definition & Purpose VAM / Valuation Adjustment Mechanism 估值调整机制是投资方与被投资公司原股东对于企业未来经营绩效的不确定性“暂不争议”,而是在投/融资协议中约定:未来根据运营的实际绩效调整企业的估值并重新划定双方的股权比例。在此定义下,VAM被用来协调投资后的公司的股东(包括投资方与原股东)之间的关系。VAM常见于创投资本和成长资本等不以取得被投资公司控股权为目的的投资案例中。VAM的目的主要是“获取增值的股权价值”,正激励原企业股东(往往也是企业运营的控制者)为企业效力。VAM可以被视为对未来不确定性的争议的妥协,否则就没有该笔投资。

Private equity (PE) investors commonly adopt a price or valuation adjustment mechanism (commonly referred to as VAM) when making growth capital or venture capital investments to mitigate against the uncertainty of the future financial performance of the investee company following the investment. The investment documents would usually provide that if the actual financial performance of the investee company post-investment turns out to be worse than an estimated or target financial threshold agreed by the investee company when the PE investor made its investment, the PE investor should be compensated by either cash or additional shares in the investee company.

资料来源:“甘肃世恒有色资源再利用有限公司、香港迪亚有限公司与苏州工业园区海富投资有限公司、陆波增资纠纷民事判决书”(2011年民申第1522号)

“目标公司2008年净利润不低于3000万元人民币;如果目标公司2008年实际净利润完不成3000万元,投资者有权要求目标公司予以补偿,如果目标公司未能履行补偿义务,投资者有权要求原股东履行补偿义务;补偿金额的计算公式为(1-2008年实际净利润/3000万元)×本次投资金额”。——海富《增资协议书》第7条第二款

With respect of Shiheng’s performance target, if by the end of 2008 Shiheng’s net profits was less than RMB30 million, Haifu shall be entitled to obtain compensation from Shiheng; and if Shiheng fail to fulfill its obligation, to claim the same from Wisdom. The formula for calculating the preceding compensation payable is (1 – the actual net profits of 2008 /RMB30 million) × the invested amount (RMB20 million). ——Article 7(b) of the Capital Increase Agreement

对赌条款:设计要点 VAM Clause: Key Issues 企业价值:交易价值 价值调整(特定情形) 投资者与目标公司对赌:无效投资者与原股东对赌:有效海富投资对赌案(对赌协议第一案)解析

第三节“分手费”条款

Section 3 Breakup Fee Clause “分手费”条款:释义与目的

Breakup Fee Clause: Definition & Purpose A breakup fee is a common fee used in takeover agreements if the seller backs out of a deal to sell to the purchaser. A breakup fee, or termination fee, is required to compensate the prospective purchaser for the time and resources used to facilitate the deal. Breakup fees are normally 1-3% of the deal's value. 分手费是在收购协议中卖方退出与买方的交易谈判时常用的费用约定。分手费或终止费用来弥补潜在买方为成就交易而花费的时间和资源。分手费的金额通常在交易总额的1%至3%之间。

Source:Investopedia “反向分手费”条款:释义与目的

Reverse Breakup Fee Clause: Definition & Purpose A reverse breakup fee is a penalty to be paid to the target company if the acquirer backs out of the deal,

usually because it can’t obtain financing. Reasons for such fees include the possibility of lawsuits, disruption of business operations, and the loss of key personnel during the period

when the company is "in play." 反向分手费是对目标公司的惩罚,如果买方退出交易(通常是因为买方出现融资困难无法解决)。反向分手费的支付范围包括因为交易谈判导致的潜在诉讼费用、停止业务运营的损失以及主要员工的流失。

Source: Investopedia “分手费”条款:示例 Breakup Fee Clause: Sample Section 7.2 Effect of Termination Section 7.2(b) If this Agreement is terminated … (ii) by Starwood pursuant to Section 7.1(h)…, then Starwood shall pay to Marriott, … a termination fee of $400,000,000 (the“Termination Fee”). Notwithstanding the foregoing, no Termination Fee shall be payable by Starwood to Marriott in any circumstance in which the Marriott stockholders vote to disapprove this Agreement or the transactions contemplated hereby.

若Starwood终止与Marriott的并购协议,则Starwood需要向Marriott支付4亿美金的分手费。在2016年3月20日,双方同意修改原并购协议提高收购价格的同时,该分手费也被提高至4.5亿美金。

“分手费”条款:设计要点 Breakup Fee Clause: Key Issues “分手费”约定在中国可行:只要不违反强制性效力性规定 买方为中国公司:一些外国公司要求买方在第三方托管账户中预付分手费成为“越来越普遍的做法” 分手费金额一般情况:交易总价的1%到3%特殊情况:(如买方已就并购方案作出修改但卖方仍然单方终止交易),分手费金额会被提高

资料来源 Sources:"Becoming common practice”:Some of the U.S. targets may ask China buyers for prenup breakup feeswhich would be held in an escrow account

Bloomberg,. Bloomberg,, 16 Feb. 2016. Web.16 Feb. 2016.

第四节 中国政府审批要求及流程

Section 4 Chinese Government Approval Requirements/Procedure

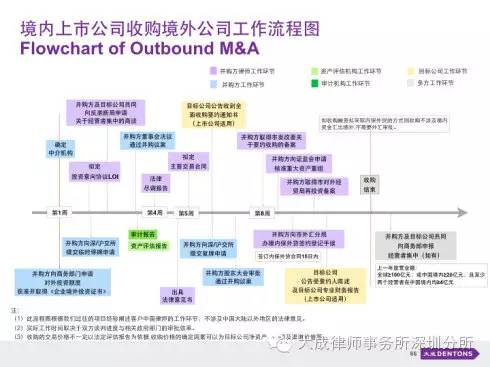

第五节 境内上市公司收购境外公司工作流程图 Section 5 Flowchart of Outbound M&A

第三部分 了解更多,请浏览www.Dentons.com