On 28 December 2019, the 15th Meeting of the Standing Committee of the 13th National People's Congress adopted revisions to the Securities Law of the People's Republic of China (the "Securities Law 2019"), which will become effective on 1 March 2020.

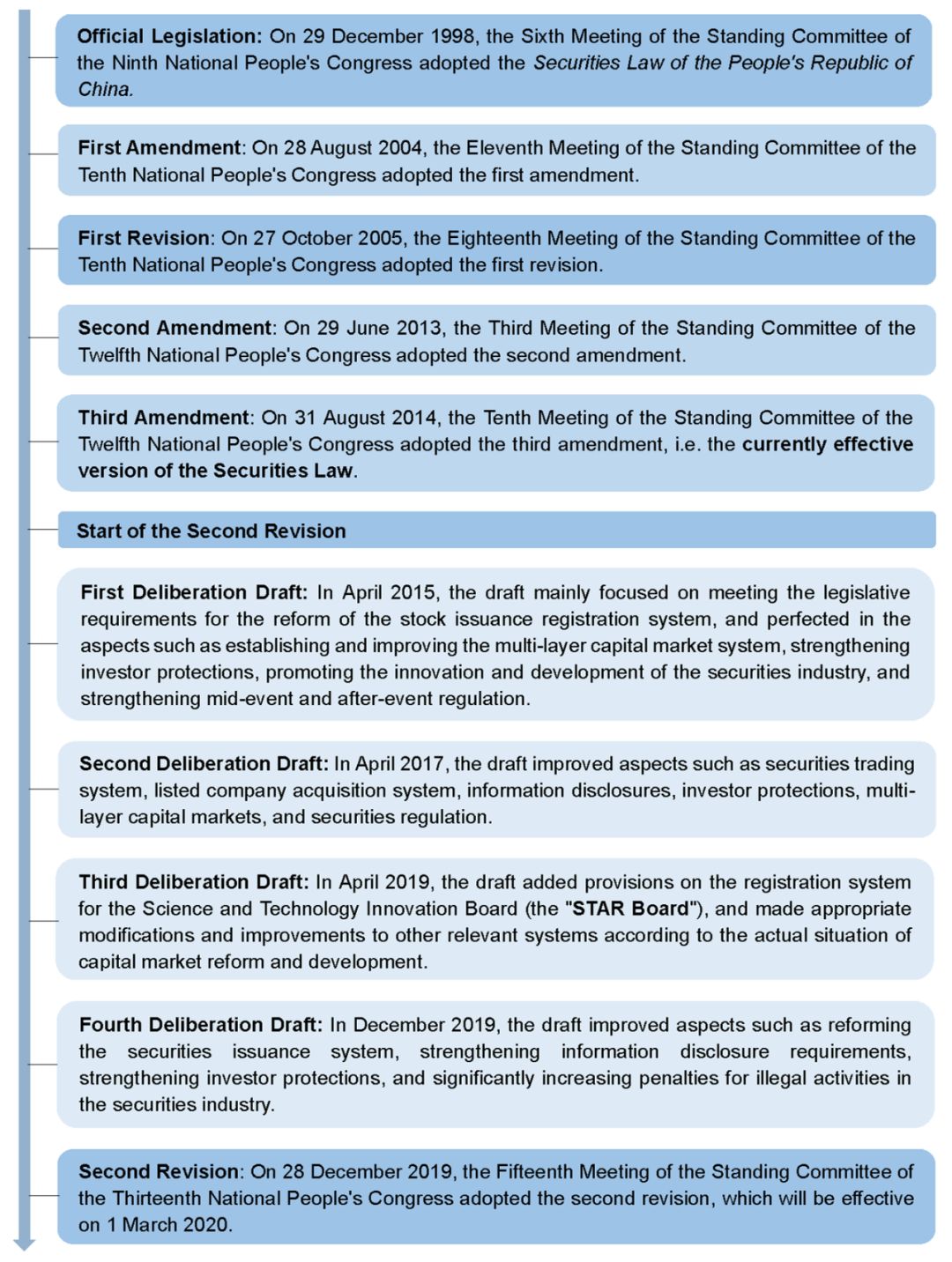

Since China first officially adopted the Securities Law of the People's Republic of China (the "Securities Law") in 1998, the Securities Law has undergone three amendments and two revisions over the past 20 years. The Securities Law 2019 is widely regarded as unfurling a new chapter for the comprehensive implementation of the securities issuance registration system, marking a significant step for China's capital markets on the road to marketization, rule of law, and internationalization.

I. Historical Review of the Securities Law

II. Key Revisions to the Securities Law

As compared to the currently effective version of the Securities Law last amended in 2014 (the "Securities Law 2014"), the key revisions in the Securities Law 2019 are as follows:

1. Comprehensive implementation of the "securities issuance registration system"

The comprehensive implementation of the "securities issuance registration system" is one of the highlights of the Securities Law 2019. On 27 December 2015, the Eighteenth Meeting of the Standing Committee of the Twelfth National People's Congress adopted the Decision on Authorizing the State Council to Adjust the Application of Relevant Provisions of the Securities Law of the People's Republic of China during the Reform of the Stock Issuance Registration System (the "Authorizing Decision"), authorizing the State Council to apply flexibly the provisions of the Securities Law in the stock issuance approval system based on the requirements for the reform of the stock issuance registration system, and to make flexible arrangements for the registration system. The Authorizing Decision, which came into effect on 1 March 2016, was renewed once in February 2018, and is slated to expire on 29 February 2020. After the Authorizing Decision was adopted, the registration system was first piloted on the STAR Board in March 2019. After nearly ten months of operation, the registration system on the STAR Board was considered fully practiced and tested.

Highlights of the registration system under the Securities Law 2019:

(1) The registration system applies to all "public securities offerings". The Securities Law 2019 explicitly provides that public securities offerings are required to satisfy the criteria provided in the laws and administrative regulations, and be registered with the securities regulatory authority under the State Council (i.e. CSRC) or other departments legally authorized by the State Council. No organization or individual may publicly issue securities without registration in accordance with law.

(2) Discretion remains for the design of specific systems within the registration system. The newly added Article 18 in the Securities Law 2019 provides for the requirements on application documents, and the addition of Article 9, which states in part "the specific scope and implementation steps of the registration system shall be formulated by the State Council" leave space for the issuance system of the STAR Board and the link between the issuance and the direct transfer-board systems of the National Equities Exchange and Quotations ("NEEQ"), which reflects more mature legislative skills.

(3) Employee stock option plans ("ESOPs") will no longer be subject to the 200-investor limitation on a look-through basis. The Securities Law 2019 clearly provides that the number of employees in an ESOP implemented in accordance with the law is not counted within the scope of a "public offering" of securities to more than 200 specific investors. In combination with the Q&A of the Shanghai Stock Exchange on the Review of the Issuance and Listing of Stocks on the Science and Technology Innovation Board and the further clarification of relevant supporting rules, (i) ESOPs that follow the "closed loop principle"

[1]; and (ii) other ESOPs that are legally established, normatively operated, have been filed with the Asset Management Association of China in accordance with the laws and regulations, or otherwise permitted under the applicable rules and regulatory framework, can be deemed to be an ESOP that will no longer be subject to the 200-investor limitation on a look-through basis provided by the Securities Law 2019.

(4) The key of the registration system is to entrust the rights of choice to the market under a developed information disclosure system. Therefore, the Securities Law 2019 has correspondently revised the following conditions for initial public offerings:

(a) From "sustainable profitability" to "sustainable operating ability". Under the registration system, regulators are no longer concerned whether issuers are profitable, in the same manner as the profitability of high-tech innovation companies is not a necessary condition for initial public offerings under the STAR Board issuance system. The above revisions in the Securities Law 2019 also create space for other stock exchange boards other than the STAR Board to remove the financial requirements of "profitability" as a criterion for initial public offerings.

(b) From "in good financial standing; no false entries in its financial and accounting documents for the preceding three years" to "audit report with unqualified opinion is issued on the financial and accounting documents in the preceding three years". The Securities Law 2014 requires substantive regulatory review to determine whether an issuer is in "good" financial standing and has "no false entries". In contrast, the Securities Law 2019 is revised to require an "audit report with an unqualified opinion". While the responsibility of judging the issuer's financial standing is compressed into the work of intermediaries, regulatory reviews will be adjusted from subjective determinations to objective standards to meet the requirements of the registration system.

(c) From "has not committed a major violation of law" to "its issuer, controlling shareholder and actual controller have not committed any crimes such as corruption, bribery, embezzlement of property, misappropriation of property or destruction of the order of the socialist market economy in the preceding three years". The Securities Law 2019 refines the compliance requirements for IPO issuers, specifying types of crimes while also expanding the scope of applicable subjects to include the issuer's controlling shareholder and actual controller, which is more in line with practical regulatory standards.

(5) Under the registration system, the requirements for public offerings of corporate bonds have been reduced. The requirements for the issuer's minimum net assets and the ratio of outstanding bond balances to net assets of the company have been replaced by "have a sound and well-functioning organizational structure". The Securities Law 2019 reflects a more market-oriented bond pricing mechanism by removing the previous requirements that: (i) the use of funds raised in the public offering be approved, and (ii) the coupon rate of the corporate bonds not exceed the coupon rate stipulated by the State Council.

(6) Clarification on the scope of duties of the regulators under the registration system. According to Article 21 of the Securities Law 2019, the registrar is the securities regulatory authority under the State Council (i.e. CSRC) or another department authorized by the State Council. The review bodies are the stock exchanges. At the same time, Article 21 clarifies that the review bodies are mainly responsible for judging whether an issuer meets the issuance conditions and information disclosure requirements, and supervising and urging issuers to improve information disclosures. Based on the operation practices of the STAR Board, the review bodies reveal potential risks and problems of the issuers mainly by supervising and urging issuers and intermediaries to continuously improve disclosures of information. The core content of the registration system is that review bodies, issuers, and intermediaries each perform their duties, and issuers and intermediaries are fully accountable.

The Securities Law 2019 clarifies the principle of comprehensively implementing the registration system for public securities offerings, and the scope of the registration system has been expanded in legislation. However, public securities offerings may involve different securities markets, enterprises of different economic types, and diversified securities types. In practice, regulators will formulate and adjust supporting implementation rules in multiple stages and steps combined with the development stages of the securities markets and actual needs to support the real economy.

2. Provisions on the sale of shares

The Securities Law 2019 does not reflect the restriction, as provided in the third deliberation draft and the rules and implementation measures of CSRC and stock exchanges on the sale of stocks, i.e., the total shares sold by a shareholder of a listed company through centralized price competition within three months may not exceed 1% of the total shares of the company. Instead, the Securities Law 2019 adds Article 36, which states that:

"The sale of shares by shareholders holding more than 5% of the shares, actual controllers, directors, supervisors, senior management personnel, and other shareholders of listed companies holding shares issued before initial public offerings or shares issued to specific targets shall not violate regulations regarding such as the lock-up period, time, amount and method of sale, and information disclosure provided by the laws, administrative regulations and other regulatory requirements by the securities regulators, and shall comply with the business rules of the stock exchanges".

This revision leaves discretion for CSRC and the stock exchanges to adjust specific regulations regarding the lock-up period, and the requirements regarding time, amount, methods and disclosure obligations for sale of shares based on the needs of the capital markets. In addition, the Securities Law 2019 clearly provides punishments for illegal share sales, i.e. orders to correct, warnings, confiscation of illegal income, and fines below the equivalent value of securities traded, and providing a more direct legal basis for administrative punishments for illegal share sales.

3. Short-swing trading

The revisions in the Securities Law 2019 on short-swing trading mainly focus on the following aspects:

(1) The rules for short-swing trading apply not only to listed companies, but also to companies whose shares are listed on other nationwide securities trading agencies approved by the State Council, such as NEEQ-listed companies.

(2) Short-swing trading rules apply not only to stocks, but also to depositary receipts, convertible bonds, and other equity-type securities recognized by the State Council in accordance with law.

(3) The scope of restrictions on short-swing trading has been expanded. In addition to directors, supervisors, senior management personnel, and shareholders holding more than 5% of the shares as currently required, the revised Article 44 of the Securities Law 2019 also applies the short-swing trading rules to shares or other equity-type securities held by or held through others' accounts, including by spouses, parents and children of directors, supervisors, senior management personnel and natural person shareholders.

4. Changes of equity interest

The Securities Law 2019 revises the rules on changes of equity interest mainly in the following aspects:

(1) In determining reportable changes of equity interest, the Securities Law 2019 specifies that "voting shares" be considered the basis of an investor's equity interest in a listed company. This differs from the Securities Law 2014, which considers the investor's overall shareholding ratio as the basis for determining changes of equity interest. This change to "voting shares" supplements and improves the core element regarding changes of equity interest. Specifically, the revised Article 63 provides:

(a) When the shareholding of an investor reaches 5% of the voting shares issued by a listed company, the investor shall, within three days from the date on which such shareholding becomes a fact, report in writing to the securities regulatory authority under the State Council and the stock exchange, inform the said listed company of the fact and make an announcement thereof. The investor shall not continue to purchase or sell the shares of the said listed company within three days from the date on which such shareholding becomes a fact, unless otherwise stipulated by the securities regulatory authority under the State Council.

(b) When the shareholding of an investor has reached 5% of the issued voting shares of a listed company, for every 5% increase or decrease in such shareholdings thereafter, the investor shall, within three days from the date on which such shareholding becomes a fact, report in writing to the securities regulatory authority under the State Council and the stock exchange, inform the said listed company of the fact and make an announcement thereof. From the date of occurrence of the fact until three days after the announcement, the investor shall not further purchase or sell the shares of the listed company, unless otherwise stipulated by the securities regulatory authority under the State Council.

The revisions to Article 63 cause the sensitive period for changes of equity interest to be more complete, rigorous and strict. The Securities Law 2019 changes the expression of the benchmark of the sensitive period from "during the period of report … and after the report and announcement" to "from the date of occurrence of the fact until the public announcement". This change means that the sensitive period is based on the occurrence of an objective fact, which makes determination of the sensitive period stricter and clearer. The revisions also extend the sensitive period from two days to three days, further extending the duration of the sensitive period.

(c) In case of purchase of voting shares of a listed company within the sensitive period in violation of the above two provisions, the voting rights shall not be exercised for the shares in excess of the prescribed ratio within 36 months after the purchase.

This is a new requirement of the Securities Law 2019, the voting rights of shares purchased in violation of the sensitive period are restricted from being exercised for a period of up to 36 months.

(d) When the shareholding of an investor has reached 5% of the issued voting shares of a listed company, for every 1% increase or decrease in such shareholdings thereafter, the investor shall notify the listed company on the day following occurrence of the fact and make an announcement thereof.

This is a new requirement in the Securities Law 2019. It should be noted that this provision only requires investors to perform a disclosure obligation and does not prohibit investors from buying or selling shares in the listed company during the sensitive period.

(2) The content of the public change of equity interest announcement includes:

(a) name and domicile of the shareholder;

(b) name and the amount of the shares held;

(c) the date on which the shareholding or any increase or decrease in the shareholding reaches the statutory percentage, and the source of funds used to purchase the shares; and

(d) The time and manner of the change in the voting shares of the listed company. Compared with the Securities Law 2014, the Securities Law 2019 imposes new requirements on the disclosure of the source of funds used to purchase the shares as well as time and manner of change in the voting shares.

5. Acquisition of listed companies

The revisions made to the relevant rules on the acquisition of the listed company by the Securities Law 2019 mainly include:

(1) Prohibition on certain additional changes to the terms of an acquisition offer:

(a) reducing the purchase price;

(b) reducing the amount of the proposed acquisition shares in the acquisition offer;

(c) shortening the acquisition period; and

(d) other circumstance stipulated by the securities regulators.

(2) In the event of the listed company issuing different share classes, the acquirer may put forward different acquisition conditions for different share classes.

(3) Extension of the lock-up period. During the acquisition of a listed company, the shares in such company held by the acquirer may not be transferred for a period of 18 months following completion of the acquisition. The Securities Law 2019 lengthens the lock-up period compared with the 12-month period as stipulated in the Securities Law 2014.

6. Information disclosure

The newly added Chapter V of the Securities Law 2019 contains provisions on the information disclosure system, and is intended to improve the information disclosure system in a systematic manner, impose higher requirements on information disclosure obligors, better protect the right to know of investors, especially small- and medium-sized investors, and lay a solid foundation for the implementation of the registration system reforms. The main points of the information disclosure system under the Securities Law 2019 are as follows:

(1) Broadening the scope of information disclosure obligors from the issuers to other information disclosure obligors stipulated by laws, administrative regulations, and securities regulators.

(2) Setting forth explicit quality requirements on information disclosure by law. Information disclosed is required to be true, accurate and complete, concise and clear, easy to understand, and shall not contain any false information, misleading representations or major omissions.

(3) Information disclosed domestically required to be synchronized with that disclosed overseas. Where the securities are publicly issued and traded domestically and overseas at the same time, the information disclosed overseas by the information disclosure obligors shall be simultaneously disclosed domestically.

(4) Specifying the content of information disclosure. Details are provided on the significant events that have a significant impact on stock and bond trading prices.

(5) Substantiating the obligations of the board of directors, supervisors and senior management personnel of the issuer in the information disclosure process, and granting them the right to raise and disclosing their explicit objections to the content in information disclosures.

7. Insider trading

The revisions in the Securities Law 2019 further improve the regulations regarding the scope of persons with access to insider information and the scope of insider information, and enhance the punishment for illegal insider trading. Any individual who engages in insider trading in violation of Article 53 of the Securities Law 2019 will be ordered to dispose of the illegally held securities in accordance with law; the illegal income shall be confiscated and a fine shall be concurrently imposed ranging from one to ten times the illegal income; where there is no illegal income or the amount of illegal income is below CNY 500,000, a fine ranging from CNY 500,000 to CNY 5,000,000 shall be imposed. For entities engaging in insider trading, the person-in-charge and other personnel who are directly responsible shall be issued a warning and be subject to a fine ranging from CNY 200,000 to CNY 2,000,000.

8. Investor protection

The newly added Chapter VI of the Securities Law 2019 significantly enhances the protection of investors, especially for small- and medium-sized investors:

(1) Clarification of investor suitability management. For the first time at the legislative level, investors are clearly distinguished into ordinary investors and professional investors. This revision provides that, in the case of any dispute between an ordinary investor and a securities company, the burden of proof shifts from the ordinary investor to the securities company. Where an ordinary investor submits a request for settlement, the securities company may not refuse such request.

(2) Establishment of a new system for solicitation and exercise in proxy of shareholder's rights of a listed company. Qualified solicitors include the board of directors of the listed company, independent directors, and shareholders holding more than 1% of the voting shares or the investor protection institution established by the State. The rights of shareholders solicited to exercise include proposal rights, voting rights, etc. Meanwhile, paid solicitations or any other paid solicitations in disguised form are prohibited.

(3) Setting up a new mechanism for advance compensation. Where an issuer causes losses to investors due to fraudulent issuances, fraudulent representations or any other significant illegal acts, the controlling shareholder, actual controller of the issuer, or the relevant securities companies may entrust an investor protection institution to enter into an agreement on compensation issues with investors who suffer losses and make compensation in advance. Upon making compensation in advance, recourse may be sought by the securities company against the issuer and other parties jointly held liable pursuant to law.

(4) Improvement on the representative litigation mechanism of securities litigation:

(a) In case an investor protection institution (which refers to the investor protection institutions established in accordance with the laws, administrative regulations or the provisions of the securities regulators) holds the shares of the listed company, under two special circumstances, i.e., (i) any director, supervisor or senior management personnel of the issuer violates the laws, administrative regulations or the articles of association of the company during his/her performance of duties in the company and causes losses to the company, or (ii) any controlling shareholder or actual controller of the issuer infringes the legitimate rights and interests of the company and losses to the company are caused, an action may be brought to the people's court in his/her own name for the benefit of the company. The shareholding ratio and shareholding period of the investor protection institution is not subject to the restriction of "holding one percent or more of the company's shares individually or jointly for 180 or more days consecutively" in general shareholder actions.

(b) When an investor brings a securities-related civil compensation action such as fraudulent representation, if the subject matter of the action is of the same type and there are multiple litigants of one party, a representative action may be adopted. The investor protection institution may be appointed by more than 50 investors to participate in the action as a representative.

9. Legal liability

The Securities Law 2019 greatly enhances punishment for relevant securities violations. Where an issuer or any of its controlling shareholders, actual controllers or other related subjects obtains illegal income, such illegal income will be confiscated and the amount of administrative punishment imposed will be raised. Where the amount of the fine is calculated based on the amount of the illegal income, the amount of such fine is raised from one to five times to one to ten times. Where an explicit range of fine is prescribed, the amount of fine is raised from CNY 300,000 to CNY 600,000, as generally prescribed in the Securities Law 2014, to respectively: CNY 2,000,000 to CNY 20,000,000 (such as fraudulent issuance), CNY 1,000,000 to CNY 10,000,000 (such as fraudulent representation, market manipulation, and public issuance without authorization), CNY 500,000 to CNY 5,000,000 (such as insider trading and alteration of the purpose of the funds raised through public issuance of securities without authorization), etc.

In addition, the Securities Law 2019 also enhances the legal liabilities of securities service intermediaries. For example, a sponsor who issues a sponsor's letter which contains fraudulent information, misleading representations or major omissions or who fails to perform other statutory duties shall be ordered to make corrections and be issued a warning; the business income shall be confiscated and the sponsor will be imposed with a fine ranging from one to ten times of the business income; where there is no business income or the amount of business income is below CNY 1,000,000, a fine ranging from CNY 1,000,000 to CNY 10,000,000 shall be imposed; where the case is serious, the business license for engaging in sponsoring shall be suspended or revoked. The person-in-charge and other personnel who are directly responsible shall be issued a warning and be subject to a fine ranging from CNY 500,000 to CNY 5,000,000.

10. Other important revisions

Other important and noteworthy revisions in the Securities Law 2019 also include:

(1) Expansion on the applicable scope of the Securities Law. In order to adapt to the previous reform of the new rules on depository receipts, depository receipts are clearly defined as statutory securities. Asset-backed securities and asset management products are explicitly written into the Securities Law 2019. And the State Council is authorized to formulate the administrative measures for their issuance and trading under the principles of the Securities Law 2019. At the same time, in view of the realistic needs of cross-border regulations in the securities industry, the Securities Law 2019 specifies that securities issuance and trading activities outside China which disrupt the market order in China and damage the legitimate rights and interests of domestic investors will be subject to legal liability in accordance with the Securities Law.

(2) Establishment of a multi-level capital markets system. The Securities Law 2019 divides securities trading platforms into three different levels, including stock exchanges, other nationwide securities exchanges approved by the State Council, and regional equity markets established according to the provisions of the State Council. The Securities Law 2019 defines the self-discipline management power of stock exchanges and other nationwide securities exchanges approved by the State Council, as well as specifies that the regional equity markets established according to the provisions of the State Council may only handle the issuance or transfer of securities in a non-public manner.

III. Supporting rules for the Securities Law 2019

The revisions made to the Securities Law cover the issuance and trading of securities, acquisition of the listed company, information disclosures, securities registration and settlement, etc. Accordingly, we expect to see revisions to be made in conformity with the Securities Law 2019 in administrative measures for initial public offering and listing, stock listing rules, stock trading rules, administrative measures for the acquisition of the listed company, information disclosure rules, administrative measures for the issuance and trading of corporate bonds, the corresponding rules of the NEEQ and other supporting rules. We will also pay further attention to the revisions of the supporting regulations of the Securities Law 2019 and share our views with readers in a timely manner.

[1] "Closed-loopprinciple": The ESOP shall not allow any transfer of any stocks at thetime of IPO of the enterprise, with a lock-up period of at least 36 months fromthe date of listing promised. If an employee, during the lock-up period beforeand after listing of an issuer, intends to transfer and withdraw the relevantrights and interests he/she holds, he/she may only transfer such rights andinterests to the employees in the ESOP or other eligible employees. If anemployee, after the lock-up period, intends to transfer and withdraw therelevant rights and interests he/she holds, such rights and interests shall bedealt with in the way stipulated in the articles of association of the ESOP orthe relevant agreement.

If an ESOP does notfollow the "closed-loop principle", it shall be composed of employeesof the enterprise, be established according to the law and be operated in astandardized manner, and shall have been filed for record with AMAC accordingto laws and regulations.

Highlights of the New PRC Securities Law

作者:汉坤律师事务所来源:汉坤律师事务所

On 28 December 2019, the 15th Meeting of the Standing Committee of the 13th National People's Congre