Barely a week ago on December 29, 2023, China’s legislative body passed and President Xi Jinping signed into law the newly revised Company Law, effective from July 1, 2024 (the “New Law”). It makes a big splash to the business community for both the law’s as-pillar significance, and the striking degree of revisions (over a quarter of provisions are involved with major changes). The New Law will bring about a broad spectrum of changes comprising shareholder capital contribution, shareholders’ rights protection, company capital system, corporate governance, company registration, company financing, etc., which may make even just a spreadsheet of bulletin points run dozens of pages long.

At Han Kun, we prioritize our clients' interests and aim to provide more than just prompt advice. Consequently, we wish to delve deeper into the New Law, decipher the legal changes most pertinent to you, and underscore the implications that demand your attention.

The U-turn in Shareholders’ Capital Contribution Obligation

1. Shortened Contribution Deadline

The 2013 and 2014 revisions of the Company Law transitioned from the registered capital payment registration system to a subscribed capital registration system, eliminating statutory requirements for contribution deadlines, minimum registered capital, and initial contribution ratios. However, the New Law introduces provisions specifying deadlines for limited liability company shareholders to fully pay subscribed capital within five years from the company's establishment date. Founding shareholders of a joint-stock company must fully pay the capital upon its establishment. For existing companies predating the New Law’s effective date, adjustments to deadlines are required, and the registration authority can demand timely adjustments if abnormal contribution deadlines or amounts are identified. Implementation rules for such existing companies will be formulated by the State Council.

2. Revocation of Shareholder Status

The New Law establishes a shareholder disqualification system for limited liability companies. If a shareholder fails to pay the contribution in full and on time, the company issues a written payment demand with a grace period of no less than sixty days. If, by the end of this period, the shareholder fails to fulfill the contribution obligation, the company, through a board resolution, can issue a disqualification notice. From the notice date, the shareholder loses rights to the unpaid contributions.

3. Added Obligation of Accelerated Capital Contribution

The New Law introduces a provision on the accelerated maturity of a limited liability company’s shareholder contribution obligations. The triggering event, "the company cannot repay the due debts," is much less restrictive than the current legal conditions for such obligation acceleration. In the future, a shareholder could face demands from the company or any creditor with unpaid debts, even if the payment schedule is not yet due.

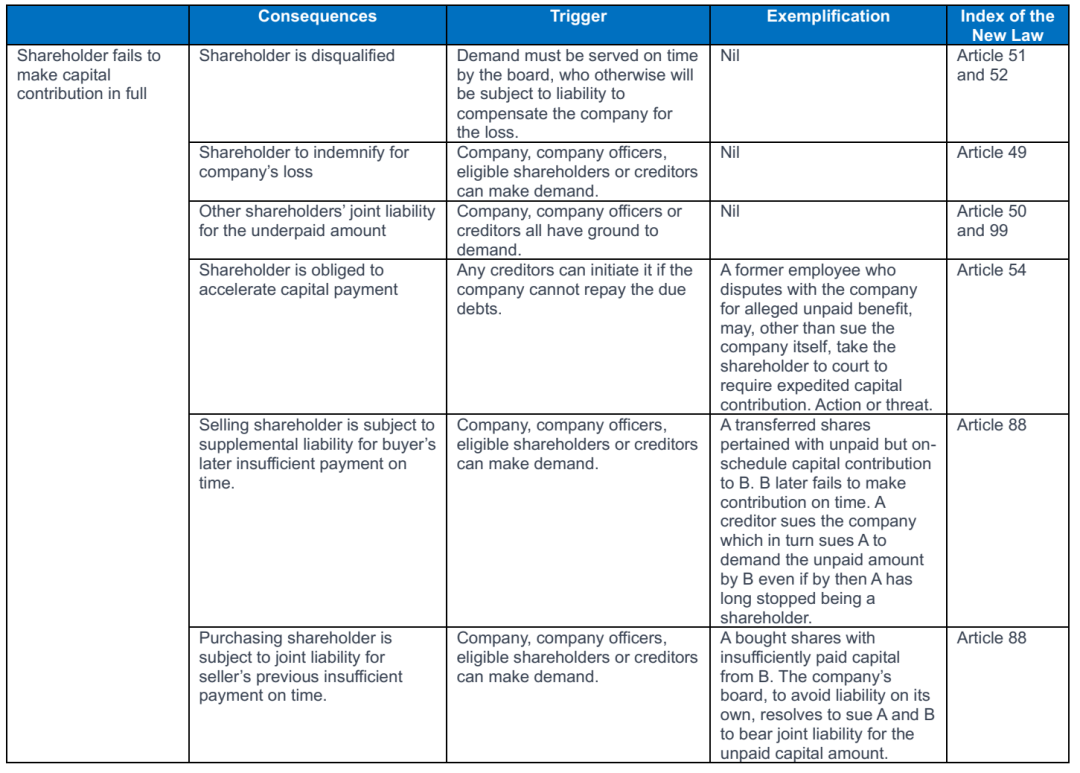

4. Expanded Legal Responsibilities

The New Law stipulates that when a limited liability company is established, if a shareholder fails to make full payment, other shareholders at the time will be jointly liable within the scope of the insufficient contribution. Additionally, supplementary liability is imposed on the former shareholder who has transferred shares to a buyer that later fails to make a full capital contribution to those shares. Joint liabilities are also applicable to the purchasing shareholder who bought shares from a former shareholder that failed to make a sufficient capital contribution on time.

The following diagram may illustrate the possible consequences of a shareholder’s underpayment of capital contribution to a limited liability company:

Despite the clarity provided by this diagram, uncertainties persist, particularly regarding how existing companies should transition for full compliance with the New Law. At this stage, we recommend existing foreign-invested enterprises with unpaid registered capital to assess the remaining contribution amount and adjust the timing accordingly. It is crucial to monitor subsequent legislative developments from regulatory authorities and formulate appropriate response plans. For newly established enterprises post the New Law's enactment, investors should carefully consider contribution deadline requirements aligned with initial business development plans, establishing a reasonable initial registered capital to mitigate risks of inability to fulfill contribution obligations. Ultimately, resolutions can be sought through subsequent capital increases.

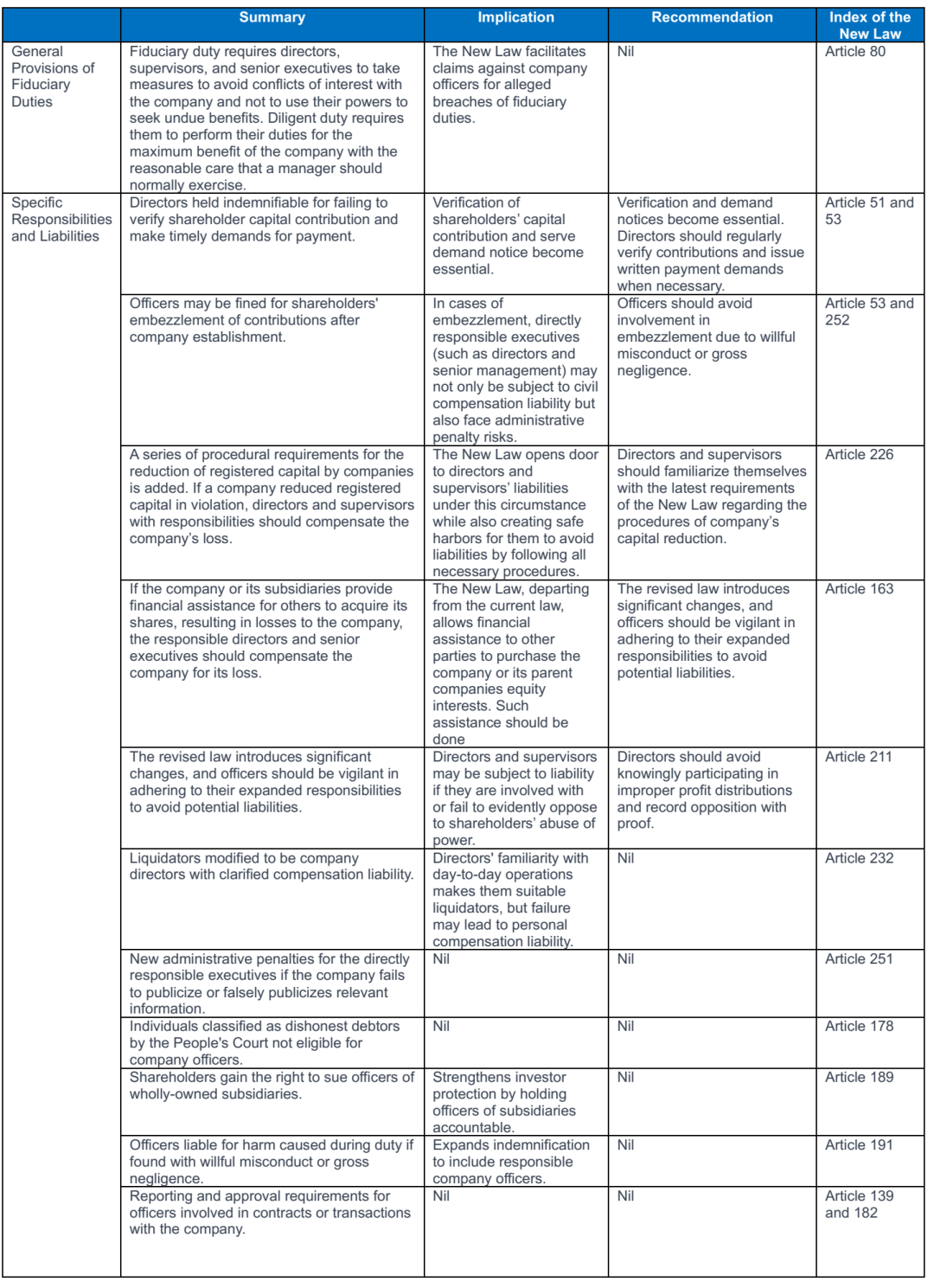

More Responsibilities Falling on Company Officers

Under China’s Company Law, the company officers consist of, mainly, director, senior executives and supervisors. Their personal liability have long been a focal point for foreign investors. Generally, the personal liability of such officers includes: (i) civil liability arising from breaches of fiduciary duties and unauthorized representation; (ii) administrative penalties and even criminal liability for directors and executives who hold relevant positions in the company or serve as key responsible persons in areas where the company violates significant compliance obligations (such as safety production, environmental protection); and (iii) directors participating in or driving decisions related to the company's criminal or irregular activities may be deemed to play a certain role in the "decision, approval, or instigation" of the company's actions and may be required to assume personal responsibility.

The New Law in this instance places a strong emphasis on the fiduciary and diligent duties of directors, supervisors, and senior management, adding administrative penalties beyond civil compensation. We summarize the main provisions, the implications and our recommendations as follows:

Significant Changes in Corporate Governance

1. Greater Flexibility in Allocation of Corporate Powers

*The statutory powers of the shareholders' meeting have been reduced, and certain matters previously reserved for the shareholders' meeting can now be decided by the board of directors or management based on the actual situation of the company (Article 59);

*Beyond the enumerated powers of the board of directors, the shareholders' meeting can explicitly grant additional powers to the board of directors, including authorizing the board of directors to make decisions on "issuing corporate bonds" (Article 59);

*The exemplary list of the manager's powers has been removed, and thus the manager's authority is entirely subject to the company's articles of association and the agreements of the board of directors (Article 74).

After this revision, decisions on "company's operational policies and investment plans" and "review and approval of the company's annual financial budget and final accounts" are no longer mandatory for the shareholders' meeting. The New Law provides companies with more operational space, enabling them to allocate powers among the shareholders' meeting, board of directors, and managers based on their specific needs. This adjustment is particularly beneficial for foreign-invested enterprises, aligning with international corporate governance practices that focus on the board's role in significant operational and investment decisions.

2. Enhanced Democratic Management Measures for Employees

The New Law mandates companies to establish a democratic management system, primarily through the employee congress. Unlike the current Company Law, which defines appointment requirements based on the background of the investing state-owned assets, the New Law specifies that for a limited liability company with more than three hundred employees, except it has set up a supervisory board with at least one sitting employee supervisor, it must involve at least one employee director to its board.

Therefore, even for non-state-owned foreign wholly-owned enterprises or limited liability companies formed as joint ventures, if they meet the aforementioned employee threshold, they may need to appoint employee directors. At the same time, companies need to be aware that such requirements may have potential impacts on the structure of board seats, and reasonable arrangements should be made in advance.

3. Permitted Absence of Supervisory Board or Supervisors

The New Law clearly states that smaller-scale limited liability companies and joint-stock companies can choose not to have a supervisory board, appoint one supervisor, or not have supervisors at all. Under the New Law, a limited liability company can establish an audit committee composed of directors to exercise the powers of the supervisory board (Article 69), without having a supervisory board or supervisors. Smaller-scale or fewer-shareholder limited liability companies may not need to have a supervisory board and can appoint one supervisor to exercise the powers of the supervisory board; with unanimous agreement of all shareholders, they can also choose not to have supervisors (Article 83).

The New Law introduces flexibility in the presence of supervisory boards and supervisors, allowing companies to tailor their governance structures to their specific needs. This aligns with contemporary practices and provides companies with greater adaptability.

In summary, the latest amendment to China’s corporate legislation introduces significant changes, shaping the legal framework for businesses. While providing opportunities for improved governance and transparency, these changes also warrant careful consideration and adaptation. As we navigate this evolving legal landscape, our legal team remains dedicated to guiding you through these modifications and addressing any concerns or questions you may have. We appreciate your ongoing partnership and are here to ensure your business is well-prepared for the implications of these revisions.

First Insights into China's New Corporate Landscape

作者:RayShi ClaireXu来源:汉坤律师事务所

Barely a week ago on December 29, 2023, China’s legislative body passed and President Xi Jinping sig