The UK remains in the most attractive destination for foreign investment in Europe. During 2014/15 the UK Trade and Investment Inward Investment Report recorded a total of 1,988 foreign direct investment projects into the UK, up by 12% from the previous year, the strongest performance since records began in the early 1980s.

There are various forms of investment for foreign investors to consider, including entering the market by setting up a new presence in the UK, entering into a joint venture with a local player, or through the direct acquisition of a company or a business.

This briefing provides an overview of the legal process when acquiring a private company or business in the UK.

Structuring the transaction

There are two principal ways of acquiring an existing UK business:

• by buying the shares of the company that owns the business (a share purchase). The seller is the shareholder(s) of the target company, who sells its/their shares in the target company to the buyer.

• by buying the assets of the company which make up the business (a business or asset purchase). The seller in this instance is the company itself, and it sells some or all of its assets to the buyer.

If the buyer buys the shares, through ownership of the target company, it automatically acquires all the company's assets, liabilities and obligations. However, if the buyer buys assets it must identify which assets, liabilities and obligations it wishes to acquire.

Some key issues likely to influence the choice of structure include:

Liabilities

On a share purchase the buyer acquires the target company "as is", with all of the company's assets, liabilities and obligations. The seller's continuing liability is basically limited to the warranties and indemnities it gives to the buyer (see below), offering the seller a cleaner break.

On an asset purchase the buyer will choose (and negotiate with the seller) the assets and liabilities it wishes to purchase; everything else stays with the company. Where the buyer has concerns about particular liabilities, an asset purchase offers the ability to pick the assets it wants and only assume known and quantified liabilities.

Tax considerations

The structuring of a transaction is also largely driven by the tax implications for both parties.

• From a seller's perspective, the following can help to mitigate their tax implications on a share purchase:

o Share for share exchanges. This is where some or all of the consideration for the purchase is paid by the issue of shares or loan notes to the seller rather than cash. This may defer the seller's tax liability on any gain they make on the shares they are selling as the gain may crystallise at a more tax efficient time.

o Dividends before sale. This is where the target company pays out an amount to the seller by way of dividend before the seller sells the target company to the buyer. This reduces the price paid for the shares and may in turn reduce the chargeable gain made by the seller.

o From a buyer's perspective, as the tax liabilities of the target company will remain with it following a purchase, the buyer should seek appropriate protection in the legal documentation.

Tax is a complex area dependent on the circumstances of the parties, including available exemptions, reliefs and allowances. So specialist tax advice should be obtained at the outset. Generally, if a seller is an individual they will likely prefer a share sale to avoid a double tax charge arising from an asset sale – an initial tax charge on the company at the time of the sale of assets to the buyer, and a further charge on the company's shareholders when the company distributes the sale proceeds.

Partial sale

Where the business for sale is a division of the seller's business, it may be more practical to structure the sale as an asset sale. Otherwise, it may be necessary first to set up a new company and transfer the division to that company followed by a share sale of the company.

Contractual consents

On an asset purchase, it is likely that consents from third parties who have contracts with the business being transferred are necessary to transfer such contracts to the buyer (including business contracts, financial agreements, licences, etc.). However, even on a share purchase it is necessary to consider whether any contract of the target company includes a change of control clause enabling the contract counterparty to end the contract on the buyer's acquisition.

Government consents

On most UK acquisitions, no consent is required from the UK Government. There are some exceptions:

• competition/anti-trust consent may be needed under EU/English competition/anti-trust laws for certain acquisitions

• if the target is in a regulated industry, regulator consent may be needed

• if the target has contracts with Government bodies, consent may be needed under the contract (see above).

Employees and pensions>

On an asset purchase, it is likely that the Transfer of Undertakings Regulations (TUPE) will apply. If so, employees of the company will automatically transfer to the buyer on their current terms of employment so that the buyer becomes the employer. Both buyer and seller will have specific obligations to inform employees of their plans to acquire or sell, and may need to consult employees prior to completion. This may impact the timetable for closing the transaction.

On a share purchase there is no change of employer as the employees simply remain employed by the target company. So, it is unlikely that TUPE will apply.

There may also be significant pension implications on both an asset purchase and a share purchase, and a buyer may be required to assume significant liabilities and obligations.

This is a complex area and specialist employment and pensions advice should be obtained.

Valuing a company

There are no set ways to value a company. In practice, we see various ways to calculate the purchase price of a company on an acquisition. The most commonly used are:

• discounted cash flows

• market multiples

• net asset valuations

• dividend yields

Often the price for the shares is calculated on a "cash free, debt free basis". This means the price assumes that either there is no cash or debt in the target company, or there is only what is necessary for normal working capital purposes.

On a significant number of purchases the price is checked through a completion accounts mechanism. Such accounts are prepared after completion, and establish the value of the shares or assets at completion. There is then a post-completion price adjustment by reference to those accounts. Please see below.

In recent years there has been an increase in "locked box" transactions. Here the parties agree the price by reference to a pre-exchange balance sheet, and controls are put in place to ensure value does not "escape" from the target company. A locked box mechanism is usually less expensive and avoids a transaction "tail", but the buyer has no recourse to a post-completion price adjustment based on completion accounts, so there can be some risk.

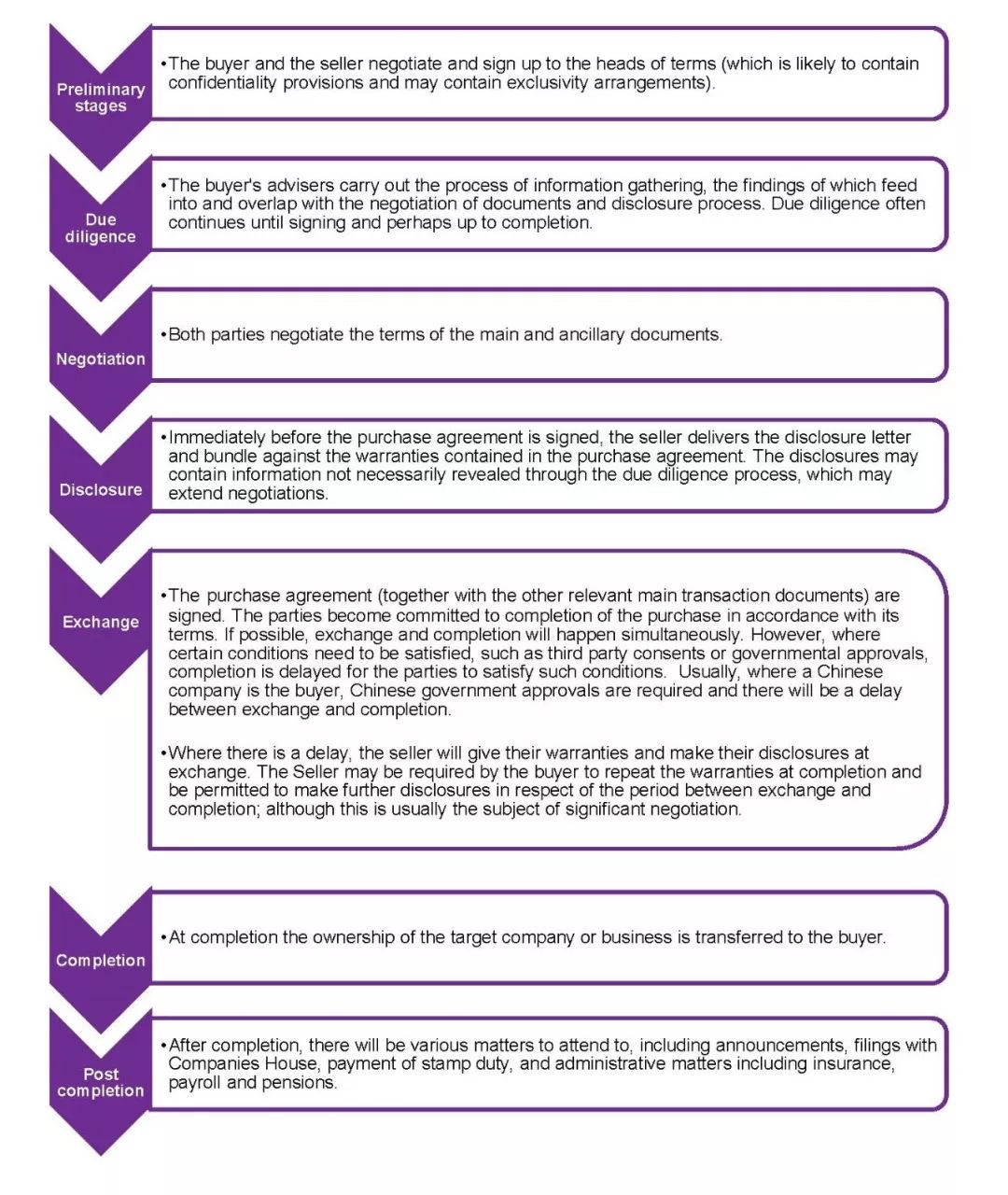

Process

Set out below is a general overview of the acquisition process, from first stages of interaction between the buyer and the seller, to post-completion administration.

[Law stated as at April 2016]

Due Diligence

Due diligence is the information-gathering process carried out by the buyer to find out as much as possible about the financial, legal and commercial condition of the target company or business. The information obtained will help the buyer to decide whether to go ahead with the transaction, and if so at what price and on what terms. The information will identify any liabilities or risk areas which may affect the structuring of the deal; areas which require contractual protection through warranties and indemnities; third party consents which may be required; and areas requiring action prior to or following the acquisition.

Legal due diligence

Traditionally the buyer's lawyers send out a request for information to the seller's lawyers, designed to obtain as much information as possible about the target company or business. All aspects of the target company or business are likely to be covered in these questions, including those regarding its constitution, contracts, property, licences, employees, litigation, financial arrangements and intellectual property rights.

The seller's team will gather the information requested and make it available to the buyer usually through the use of an electronic data room. The buyer's lawyers will review the information provided and produce a legal due diligence report for the buyer, which will contain issues raised from their analysis and suggested remedies or appropriate protective measures. The detail of the report will vary depending on the buyer's familiarity with the target company or business and the extent of factors that may be material to the buyer. Traditionally, a full report of all findings is produced. More commonly, "red-flag" reports containing only key concerns and issues are prepared.

To ensure coordination, it is necessary to set up good reporting lines and there must be regular communication between the different advisers. Whilst the due diligence process begins early on in the transaction, it can often run alongside negotiation of the transaction documents and overlap with the disclosure process, so it is important that the negotiating team is promptly informed of any significant issues which are uncovered by the due diligence.

Financial due diligence

Financial due diligence focuses on the historic trading performance of the target company or business. The buyer's accountants will analyse the financial books and back up their review by talking to the target company's own accountants and management. They will also review the target company's tax history to identify any potential disputes with the UK tax authority.

Commercial and other due diligenc

Commercial due diligence looks at broader issues such as the market in which the target company or the business operates, competitors, and its strengths and weaknesses. Typically commercial due diligence is carried out by the buyer itself or in conjunction with the financial due diligence. Sometimes, a specialist consultancy may be involved to carry out a more detailed analysis.

Other areas of due diligence may include real property and environment, and this may require coordination of specialists to provide property surveys, environmental audits, health and safety reports, etc.

Transaction documents

Preliminary documents

Heads of terms

This sets out the main terms of the commercial transaction agreed in principle between the parties. They are not legally binding (except for confidentiality or exclusivity clauses, if included, and potentially costs provisions).

Confidentiality agreement

This may be contained in the heads of terms, or be subject to a separate agreement. This imposes a duty of confidentiality on the buyer in respect of the confidential information regarding the target company or the business provided by the seller during the due diligence process as well as the fact of the potential purchase, and the confidentiality agreement itself and its terms. There is usually a reciprocal duty of confidentiality on the seller in respect of the buyer if information about the buyer is disclosed to the seller.

Exclusivity agreement

Again, this might be in the heads of teams or a separate agreement. This will prevent the seller from seeking or negotiating with other potential buyers for an agreed period of time, giving the buyer a period of exclusivity in which to negotiate and conclude the transaction.

Main transaction documents

Share purchase agreement

On a share purchase, this is the principal contractual document governing the acquisition of the shares in the target company. It is generally the buyer's lawyers who prepare the initial draft; although the seller's lawyers are likely to prepare it on an auction sale. The main areas covered are:

• Agreement to buy and sell the shares

• Consideration

• Conditions to complete (if applicable) (see below)

• Completion arrangements

• Detailed warranties about the target company and indemnities

To protect the buyer against liabilities which may exist in the target company, the seller is generally required to give a significant number of warranties covering most aspects of the company being acquired. These warranties are assurances from the seller confirming statements (usually of fact) about the target company. If any of these assurances are untrue and result in the value of the shares of the of the target company being less than the consideration paid, the seller may be liable to pay damages to the buyer under a breach of warranty claim. Warranties therefore encourage the seller to provide further information about the target company in the form of disclosures (see below) against the warranty to clarify the target company's true position, and avoid a warranty claim.

Additionally, where specific issues are revealed by due diligence which may cause loss to the target company, the buyer may choose to seek specific indemnities from the seller which allow the buyer to recover, on a £1 for £1 basis, for any particular liability covered by the indemnity which crystallises.

Warranty and indemnity clauses are always a focus of negotiations for both the buyer and the seller, and they are essentially contractual risk allocation arrangements. Warranty and indemnity insurance (W&I Insurance) can act as a means of closing the gap between the needs of the buyer and seller. W&I Insurance provides cover for losses arising from a breach of warranty or in certain cases under an indemnity. Properly implemented, it is intended to transfer the risk of financial loss associated with a claim for a breach of an insured warranty or indemnity from the seller to the insurer. In the last few years, we have seen about 5% of UK acquisitions having W&I Insurance in place.

• Seller's protections and limitations of liability

• Any restrictive covenants which are to bind the seller after completion

In order to ensure that the seller will not compete with the target company in following the purchase, the buyer will seek undertakings from the seller that will restrict their ability to carry on business which competes with the target company's business, solicit the target company's customers, suppliers or employees, disclose confidential information concerning the target company, or use any trade name previously used by the target company. To be enforceable, these undertakings must be reasonable in scope, duration and geographic extent. If not, they could be held to be unreasonable as they restrain trade and as a result would be invalid.

• Pre-completion undertakings

If there is a delay between exchange and completion, as management and control of the target company will remain with the seller in the interval, the buyer will seek to build appropriate safeguards into the share purchase agreement to ensure that the business of the target company is carried on in the ordinary course, and that no major decisions are taken without the buyer's prior approval.

Asset purchase agreement

On an asset purchase, this is the principal contractual document governing the acquisition of the assets in the target company. It is also generally the buyer's lawyers who prepare the first draft. The main areas covered are similar to those in the share purchase agreement.However the agreement needs to set out the details of the assets and liabilities to be transferred. This is usually done in the definitions section and by reference to a schedule which will list the assets. The agreement will provide that the consideration will be apportioned between the various assets.

Disclosure letter

In this document the seller makes general and specific disclosures against the warranties in the share or asset purchase agreement in order to clarify the true position of the target company or business. Both the warranties and the disclosure letter are considered together. If a warranty is untrue, the buyer may have a claim for breach of contract. However, if the warranty is adequately disclosed against in the disclosure letter, there should be no claim.

Tax covenant

This document is only relevant to share purchases. In this document the seller undertakes to pay the buyer an amount equal to any tax liability that may arise in the target company before the buyer's ownership. Essentially this document provides a means of adjusting the price of the target company, if for tax reasons it turns out to be worth less than originally assumed.

Stock transfer form

This is a simple and standard document that transfers the legal title of the shares from the seller to the buyer and is executed by the seller. Stamp duty (currently at the rate of 0.5% of the share price, rounded up to the nearest £5) is chargeable on a transfer of shares unless exemptions apply or specific stamp duty relief is sought. Usually, the buyer will pay the stamp duty by presenting the stock transfer form to HMRC for stamping. To avoid penalties or interest for late submission, the stock transfer form should be submitted to HMRC within 30 days of execution.

The target company will register a transfer of shares and update its register of members after it has received a duly executed and stamped stock transfer form. This means that a registration of the shares transferred in an acquisition rarely occurs on the day of completion. Normally it occurs weeks later.

The register of members is prima facie evidence of who the members of the company are, and what shares they hold. On the transfer of the shares, the buyer will usually ask for a power of attorney to be granted by the seller to enable the buyer to control the rights attaching to the shares.

Other agreements

On a share purchase there is likely to be other agreements; for example, the target company may wish to continue to receive services from the seller or another company in the seller's group for a limited time under a transitional services agreement.

On an asset purchase, there are likely to be further documents required to perfect the transfer of assets; for instance, property transfer forms or lease assignments for property, assignments and/or novations of contracts, and assignments of intellectual property.

Ancillary documents

Board resolutions

It is typically required that both parties (if they are corporates) will pass board resolutions to approve the entry into the transaction. Board resolutions of the target company are also required to approve the relevant transaction and the resignation and appointment of directors, company secretary and auditors of the target company, etc.

Resignation/appointment letters

If directors, company secretary and/or auditors of the target company are to resign after the sale, the relevant resignation letters will be produced.

Exchange and completion

Approvals and timing

Regulatory authorities

The buyer will need to consider at the start of the transaction whether it will need to notify or receive consent from any regulatory authorities in connection with the transaction, including:

• the competition authorities of any relevant national state or the EU (and where the buyer and/or the seller are non-UK companies, they will need to seek relevant local counsel advice)

• the regulator of any industry sector in which the target company or business operates, e.g. financial services, utilities, broadcasting and telecommunications

• tax authorities: either or both parties may wish to apply for certain tax clearances from the relevant tax authorities

• regulatory consents and/or registration from the relevant authorities in the jurisdictions where the buyer and/or the seller is incorporated or operates, e.g. foreign exchange controls in China

Third parties

As noted above, the consent of third parties such as the target company's lenders or key suppliers may be necessary if, for example, its financing or other contractual documents contain change of control clauses.

Internal approvals

• Board approval: if the transaction involves a corporate buyer or seller, the board of that corporate should properly consider and approve the transaction.

• Shareholder approval: the shareholders of a corporate buyer or seller may have to approve the transaction. For example, articles of association or a shareholders' agreement may prevent a company's directors from making significant acquisitions or disposals without shareholder approval.

The nature and extent of the necessary notifications and approvals will have an impact on the timing of the transaction. Depending on the circumstances, it may be necessary to have a split between the exchange and completion. Completion is the date on which the buyer receives the documentation effecting the transfer of ownership of shares or assets (if physical delivery of assets is not applicable) and all

Price adjustment

Completion accounts

Completion accounts relating to the target company or business are drawn up following completion in accordance with an agreed methodology specified in the share or asset purchase agreement. They are used to confirm the target company's financial position or the value of the business at completion, to ensure that it is consistent with the position in the accounts on which the buyer based its valuation of the target company or business on. The purchase price will then be adjusted (perhaps up or down) to reflect the position shown in the completion accounts.

Earn-outs

An earn-out is where, on the sale and purchase of a company's shares or assets, the purchase price is wholly or partially determined by reference to the future performance of the target company or business. For example, part of the consideration might be calculated by reference to profits over two to three financial periods after completion. This is commonly used as a management incentive where an owner-managed company or business is sold and the mangers continue to work for the company or business for an agreed period following the sale.

Completion and post-completion

On completion of the transaction, the buyer will become the new owner of the target company or business. There will be various post-completion matters to deal with, including:

• announcements and notifications

• filings at Companies House if there is any change of officers, accounting reference date or registered office

• payment of stamp duty on a share purchase (see above) and possibly an asset purchase if shares in any subsidiary company are being transferred as part of the asset purchase

• payment of stamp duty land tax on an asset purchase if the assets include real property

• preparation of completion accounts where relevant

• on an asset purchase, assignments/novations of supplier and customer contracts

• the buyer should also set up a system for monitoring potential warranty claims which may arise so that it does not miss deadlines for notifying claims set out in the share or asset purchase agreement

• administrative matters such as:

o managing insurance policies e.g. directors and officers' insurance;

o transferring employees' payroll records to the new employer reference where necessary; and

o pension scheme set up or transferred for target company employees where the target company was part of a group pension scheme.

Acquisition of Private Companies in the UK

作者:RichardBarham WeiWu来源:大成深圳办公室

The UK remains in the most attractive destination for foreign investment in Europe.