In the process of constructing and developing a multi-level capital market, market participants have always been looking forward to more stable and transparent tax rules. Along with improvements to the capital market-related tax regime, we are also looking forward to more systematic and well-reasoned income tax incentives which may be the icing on the cake of an increasingly liberal investment environment.

Near the end of this year, the Ministry of Finance (“MOF”) and State Administration of Taxation (“SAT”) released a series of tax incentive policies which extend nationally the four tax incentives that have been implemented in the National Innovation Demonstration Zone (“NIDZ”).

Four NIDZ Pilot Tax Incentives to be Rolled Out Nationwide

On October 23, 2015, MOF and SAT jointly released the Circular on Promoting the Pilot Tax Policies in NIDZ Nationwide (Cai Shui [2015] No.116, “Circular 116”), rolling out the four income tax incentives nationwide.

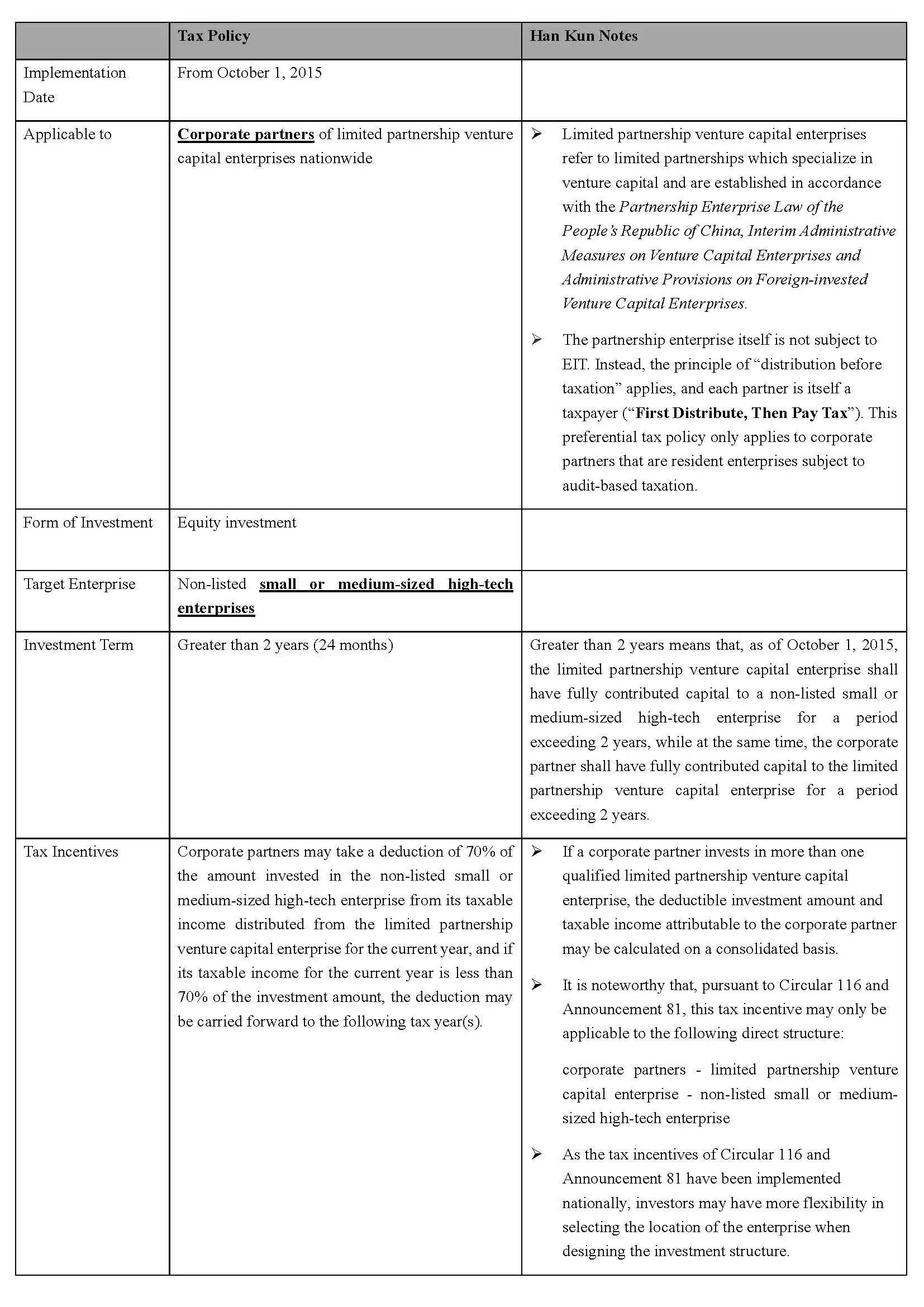

Enterprise income tax (“EIT”) policy for corporate partners of limited partnership venture capital enterprises

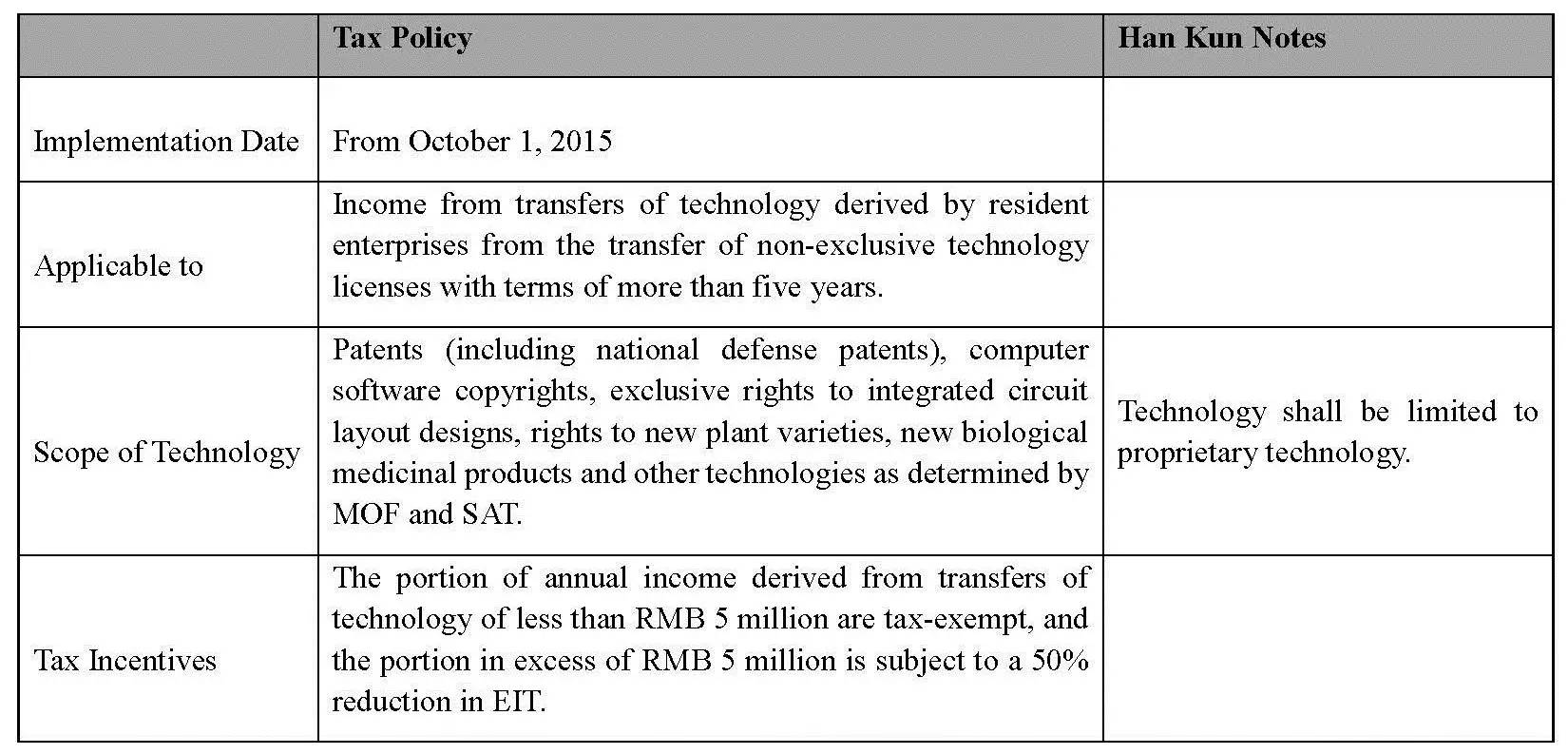

EIT policy for income from transfers of technology

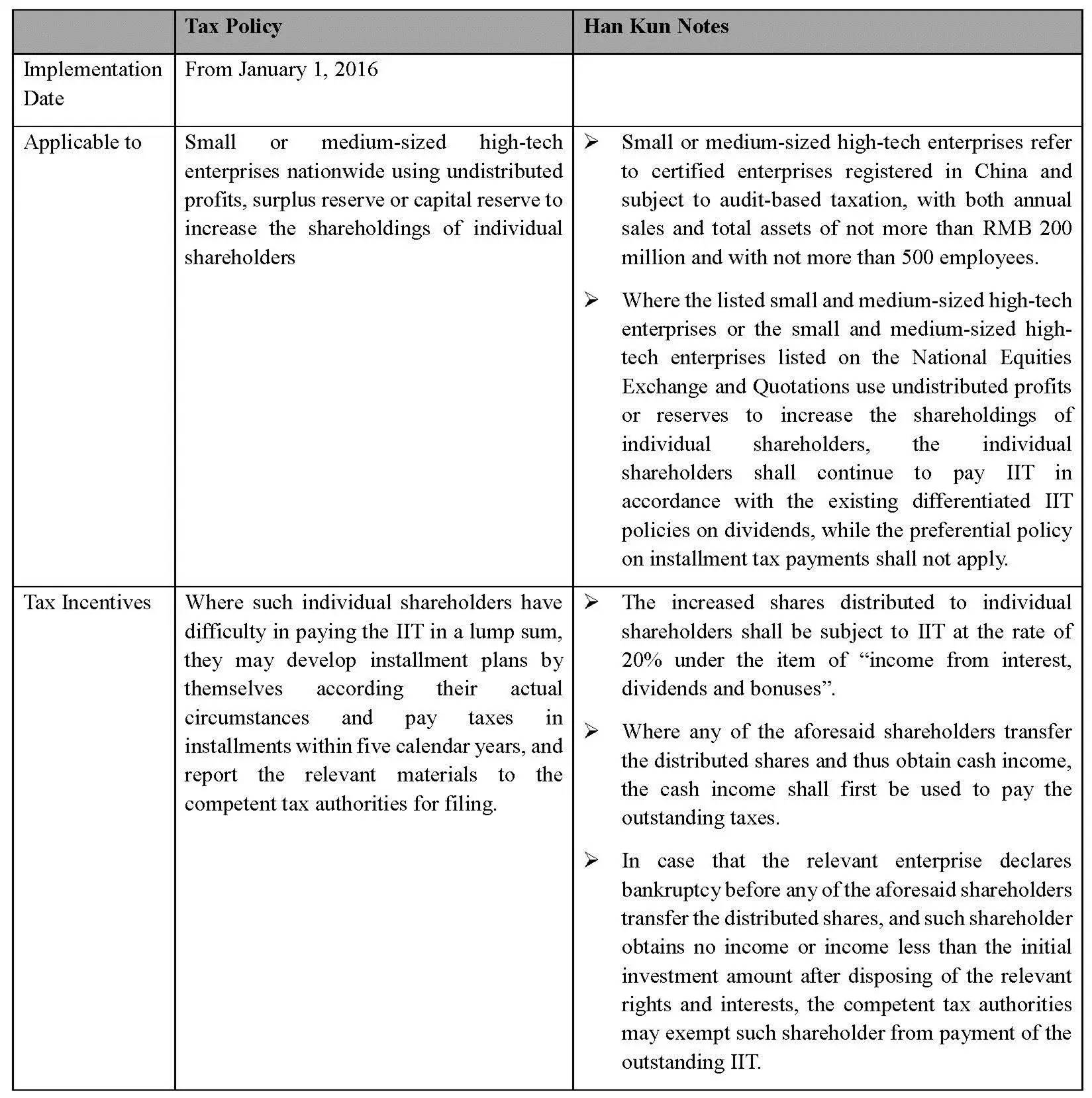

Individual income tax (“IIT”) policy for reserve-converted shares

IIT policy for equity incentives

We summarize below our insights on the four tax rules for your reference.

1、EIT Policy for Corporate Partners of Limited Partnership Venture Capital Enterprises

Despite the lengthy title, this preferential policy is worthy of applause by corporate partners. SAT released the Announcement on Issues Concerning EIT on Corporate Partners of Limited Partnership Venture Capital Enterprises, dated November 16, 2015 (SAT Announcement 2015 No.81, “Announcement 81”), which further clarified the implementation of the preferential EIT policy for corporate partners.

Salient Issues to be Resolved

Limited liability partnerships have been widely used since the new Partnership Enterprise Law came into force in 2007. The Circular on Issues Concerning EIT on Partners of Partnership Enterprises (Cai Shui [2008] No.159), issued by MOF and SAT in 2008, specifies the principle of “First Distribute, Then Tax.” Unfortunately, although the new Partnership Enterprise Law has been amended for nearly ten years, partnership-related income tax collection continues to follow rules which have been in place for more than fifteen years, and which may not be current with the development of the market. For instance, principle matters such as whether the equity investment gains of a corporate partner from investment in a target enterprise through a limited partnership can be considered exempt income remains to be further defined.

2、EIT Policy for Income Derived from Transfers of Technology

SAT released the Announcement on Issues concerning EIT on Income from Transfers of Technology (SAT Announcement 2015 No.82, “Announcement 82”), which specifies the EIT tax incentives for income from transfers of technology. We briefly summarize the provisions of Circular 116 and Announcement 82 as follows:

3、IIT Policy for Reserve-converted Shares

(1) Salient Issues Concerning Tax Policies for Reserve-converted Shares

The IIT related to using undistributed profits and surplus reserves to increase share capital in the current tax collection regime is relatively clear. However, there is more controversy moving from theory to practice for the taxation of capital reserves which are used to increase share capital. Actually, this controversy derives from the following two SAT tax collection documents:

Article One of the Circular on the Exemption of IIT on Increase of Share Capital and Bonus Share Distribution of Joint-Stock Enterprises (Guo Shui Fa [1997] No.198, “Circular 198”) stipulates that when a joint-stock enterprise converts its capital reserves into share capital, it shall not be defined as distribution of dividends or other distribution of similar nature, and the amount of the share capital acquired by the individual shall not be treated as taxable income.

Article Two of Reply on Taxable IIT on Income from Individual Shares Added Value in Process of Former Urban Credit Cooperatives Transforming into Urban Cooperative Banks (Guo Shui Han [1998] No.289, “Reply 289”) points out that the “Capital Reserve” in Circular 198 shall mean the capital reserve derived from income of a joint-stock enterprise when issuing shares at a premium (“Additional Paid-in Capital”). Individual income from Additional Paid-in Capital shall not be subject to IIT, while individual income from capital reserves other than Additional Paid-in Capital shall be subject to IIT.

Reply 289 specifies that only the income from Additional Paid-in Capital of a joint-stock enterprise is not be subject to IIT when converting capital reserves into share capital. In the practice of investment and financing,discrepancies arise as to whether individuals recognize income when converting capital reserves derived from Additional Paid-in Capital of a limited liability company into share capital and when converting capital reserves which are derived from the conversion of a limited liability company into a joint-stock enterprise into share capital.

(2) Further Clarification of Tax Incentives for Reserve-converted Shares

Although the aforementioned controversy on the taxability of converting capital reserves into share capital has not been fundamentally resolved, Announcement on Issues Concerning the Collection and Administration of IIT on Incentive Shares and Increased Shares from Distributions, released by SAT and dated November 16, 2015 (SAT Announcement 2015 No.80, “Announcement 80”), has provided a positive signal to the market regarding preferential IIT policies for reserve amounts which are converted into shares distributable to shareholders.

4、IIT Policy for Equity Incentives

According to Circular 116 and Announcement 80, individuals acquiring equity incentives from high-tech enterprises subject to audit-based taxation may enjoy relevant IIT preferential policies.

Han Kun Viewpoint

Extending the four NIDZ tax incentives nationally will play a positive role in stimulating entrepreneurship and innovation in the market and in creating a fair tax environment. We recommend that market participants pay attention to the applicable scope and filing requirements specified in the relevant policies, so as to control the risk of tax compliance in investment and financing transactions.

A Large Wave of Income Tax Incentives is Coming

作者:薛冰 谢逸姿来源:汉坤律师事务所

In the process of constructing and developing a multi-level capital market, market participants have