Overview of fund investment advisory business

Securities and fund investment advisory business is a basic capital markets intermediary service. Securities and fund investment advisory business currently comprises securities investment advisory business, fund investment advisory business, and securities research report issuing business. Fund investment advisory business refers to services where (a) clients entrust an advisor to provide them with investment advice as agreed in the contracts regarding mutual funds and other investment products recognized by the China Securities Regulatory Commission ("CSRC"), and (b) an advisor assists clients to make investment decisions or makes transactions on behalf of clients. Fund investment advisory business may be divided into non-discretionary fund investment advisory business and discretionary fund investment advisory business, based on the relevant scopes of authority granted by clients to the advisor. Non-discretionary fund investment advisory business refers to where clients entrust an advisor to provide advice on mutual fund portfolio strategies without making any investment decisions on their behalf. Discretionary fund investment advisory business refers to where an advisor agrees with clients to make decisions on their behalf for specific mutual fund investment types, quantities, and trading opportunities according to portfolio strategies, and to process transaction requests such as subscription, redemption, and conversion of funds. The relevant laws and regulations on fund investment advisory business include the Notice on Facilitating the Trial Running of Mutual Fund Investment Advisory Business (《关于做好公开募集证券投资基金投资顾问业务试点工作的通知》), the Measures for the Administration of Securities and Fund Investment Advisory Business (Draft for Comments) (《证券基金投资咨询业务管理办法(征求意见稿)》), the Guidelines on the Content and Format of the Mutual Fund Investment Advisory Service Agreement (Draft for Comments) (《公开募集证券投资基金投资顾问服务协议内容与格式指引(征求意见稿)》), the Guidelines on the Content and Format of Risk Disclosure Statement for Mutual Fund Investment Advisory Business (Draft for Comments) (《公开募集证券投资基金投资顾问服务风险揭示书内容与格式指引(征求意见稿)》), and the Guidelines on Display of the Performance and Clients’ Assets of Mutual Fund Investment Advisory Business (Draft for Comments) (《公开募集证券投资基金投资顾问服务业绩及客户资产展示指引(征求意见稿)》) (hereinafter collectively referred to as the "Fund Investment Advisory Regulations"). It is foreseeable that the supervisions on fund investment advisory institutions will strictly follow the relevant regulatory rules of fund management companies and the compliance management, internal control and risk management of fund investment advisory institutions will face higher standards in the future. More explicit regulations and requirements will be applied to the business definitions, service models, liabilities, prohibited actions, information disclosure, risk disclosure, promotion etc. of fund investment advisory services. As of December 31, 2021, 58 institutions have obtained the fund investment advisory qualifications, among whom 22 are fund management companies, 29 are securities companies, 3 are fund distribution institutions, and 4 are other financial institutions[1].

The core elements of the fund investment advisory business include products, strategies, investment advice and clients. From global perspective, fund investment advisory business includes four different forms: "intelligent investment advisory", "intelligent + artificial investment advisory ", "investment advisory" and " financial management". Under the current regulatory framework, there is no need for a service provider to file or register with CSRC if the fund investment advisory service is ancillary to its fund distribution service, and no separate contract is signed and no separate service fee is charged for the ancillary service. However, the basic legal relationships for fund distribution business shall be followed within the current regulatory framework and distributors are prohibited from engaging in any discretionary fund investment advisory service.

This article mainly analyzes key compliance issues and industry concerns in course of the fund investment advisory business under the Fund Investment Advisory Regulations, including internal decision-making and process control for fund investment advisory strategies, additional requirements for discretionary fund investment advisory services, management of investor suitability and promotion activities, management of conflicts of interest and establishment of effective segregation mechanism, and declaration and information disclosure, etc. for your reference.

Key aspects of compliance and internal control for fund investment advisory business

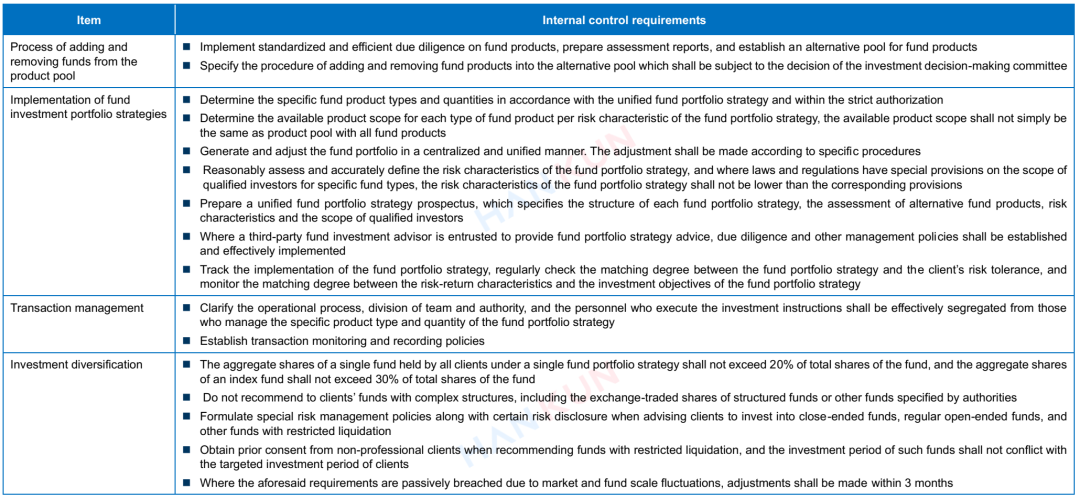

1. Internal decision making and process control of fund investment advisory business

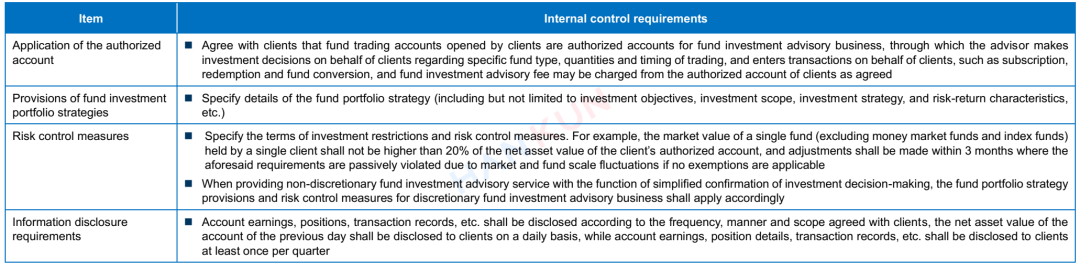

2. Additional requirements for discretionary investment advisory business

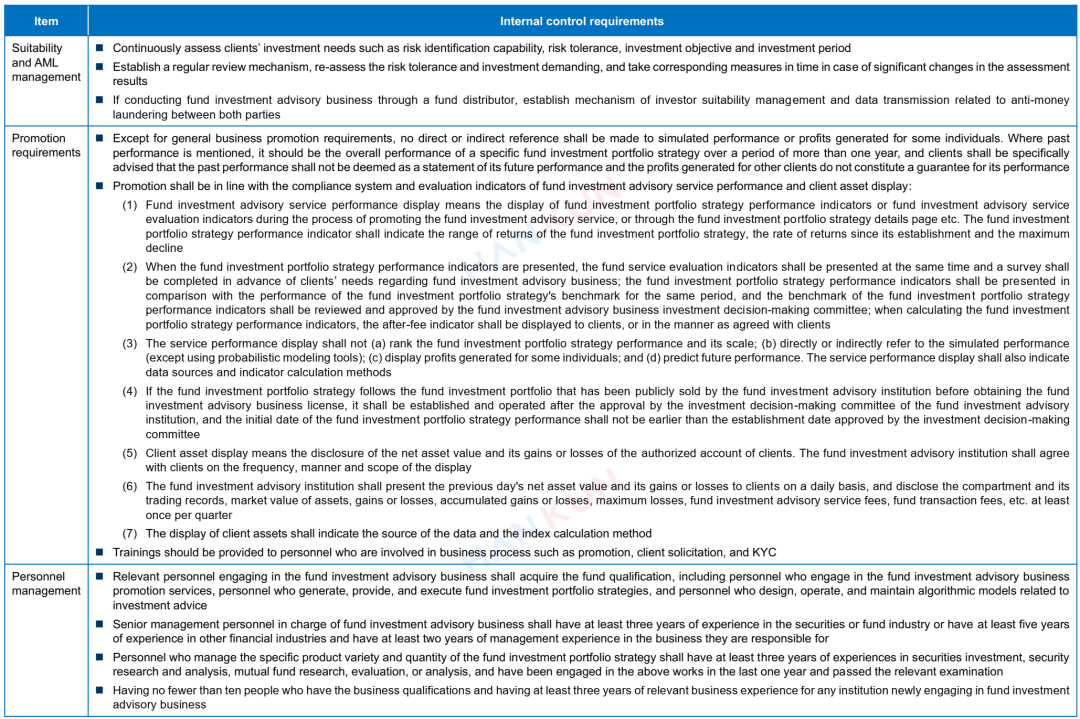

3. Management of investor suitability and promotional activities

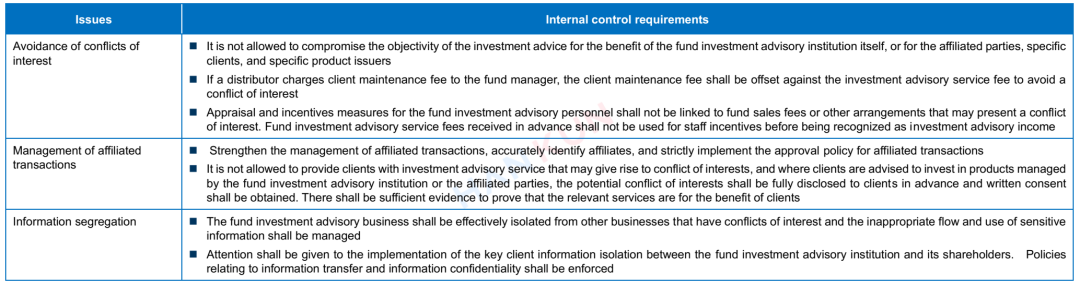

4. Management of conflicts of interest and establishment of effective segregation

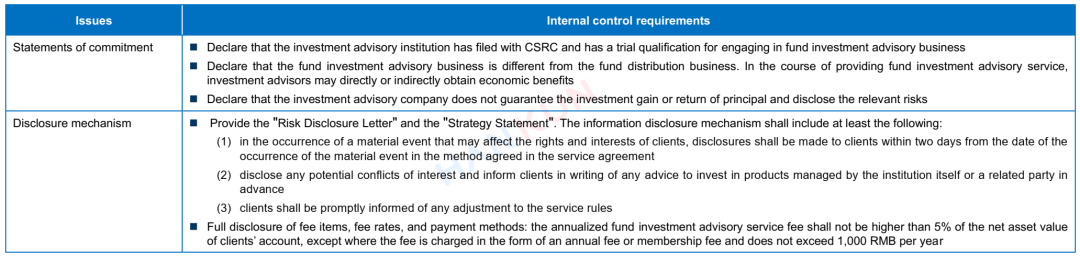

5. Declaration and information disclosure

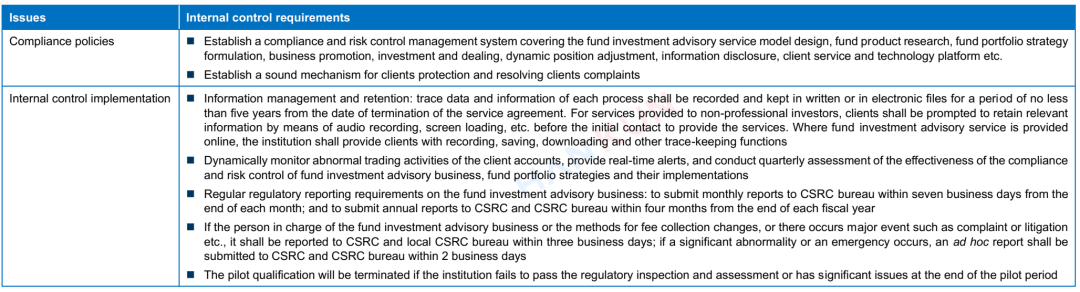

6. Other compliance and internal control requirements

Note: The implementation of certain key points of above compliance and internal control shall depend on the finalization of relevant draft rules.

The regulatory system for fund investment advisory business continues to improve

In response to the "grey area" in the development of fund investment advisory business, the recently issued Fund Investment Advisory Regulations clarify these issues and would comprehensively regulate the qualification conditions, internal management, service models, risk disclosure, promotion, asset display and service evaluation. The Fund Investment Advisory Regulations aim to establish a multi-dimensional legal and compliance system for the future development of fund investment advisory business, fully reflecting the principles of orderly entry/exit, mutual balance, structural optimization, and risk matching.

We are also paying attention to discussions of certain business models in the market:

Model 1: fund managers list a series of fund portfolios on the fund distributors’ business outlets/websites without charging separate fee or signing separate fund investment advisory agreement, whereas the fund manager will be displayed as the manager of the fund portfolio;

Model 2: fund distributors sell mutual fund products on a commission basis and provide one-click ordering services without a separate fee. Each fund subscription ratio has been configured by default, but the investors may modify the subscription ratio of each fund at their discretion;

Model 3: a key opinion leader in the fund business acts as the portfolio manager and relevant funds remain in the investor's own account; after the investor has subscribed a fund portfolio, the system will automatically allocate the funds to relevant portfolio per the ratio adopted by such portfolio manager.

We believe the legal application and compliance of above-mentioned business models will be further clarified. According to the Fund Investment Advisory Regulations, institutions with non-compliant business models would not be allowed to conduct new non-compliant activities in providing fund investment portfolio strategy recommendations. This includes not presenting or launching new fund investment portfolio strategies, not adding new clients to existing fund investment portfolio strategies, and not providing additional portfolio strategy investments for existing clients. In addition, clients would be prominently alerted that the institution is in the process of rectifying its fund investment advisory activities and that there is a risk that services cannot be provided uninterrupted in the future.

We will continue to closely monitor the development and implementation of the Fund Investment Advisory Regulations, and how they can be effectively applied to various business scenarios and embedded into the institutions’ internal control frameworks, and work with market participants in connection with legal, compliance, and risk management issues in the development of fund investment advisory business.

[1] http://www.csisc.cn/zbscbzw/jjtzgw/202109/f1e411bef5f64a0595ed9aa09a4f030f.shtml.

Securities and fund investment advisory business is a basic capital markets intermediary service. Securities and fund investment advisory business currently comprises securities investment advisory business, fund investment advisory business, and securities research report issuing business. Fund investment advisory business refers to services where (a) clients entrust an advisor to provide them with investment advice as agreed in the contracts regarding mutual funds and other investment products recognized by the China Securities Regulatory Commission ("CSRC"), and (b) an advisor assists clients to make investment decisions or makes transactions on behalf of clients. Fund investment advisory business may be divided into non-discretionary fund investment advisory business and discretionary fund investment advisory business, based on the relevant scopes of authority granted by clients to the advisor. Non-discretionary fund investment advisory business refers to where clients entrust an advisor to provide advice on mutual fund portfolio strategies without making any investment decisions on their behalf. Discretionary fund investment advisory business refers to where an advisor agrees with clients to make decisions on their behalf for specific mutual fund investment types, quantities, and trading opportunities according to portfolio strategies, and to process transaction requests such as subscription, redemption, and conversion of funds. The relevant laws and regulations on fund investment advisory business include the Notice on Facilitating the Trial Running of Mutual Fund Investment Advisory Business (《关于做好公开募集证券投资基金投资顾问业务试点工作的通知》), the Measures for the Administration of Securities and Fund Investment Advisory Business (Draft for Comments) (《证券基金投资咨询业务管理办法(征求意见稿)》), the Guidelines on the Content and Format of the Mutual Fund Investment Advisory Service Agreement (Draft for Comments) (《公开募集证券投资基金投资顾问服务协议内容与格式指引(征求意见稿)》), the Guidelines on the Content and Format of Risk Disclosure Statement for Mutual Fund Investment Advisory Business (Draft for Comments) (《公开募集证券投资基金投资顾问服务风险揭示书内容与格式指引(征求意见稿)》), and the Guidelines on Display of the Performance and Clients’ Assets of Mutual Fund Investment Advisory Business (Draft for Comments) (《公开募集证券投资基金投资顾问服务业绩及客户资产展示指引(征求意见稿)》) (hereinafter collectively referred to as the "Fund Investment Advisory Regulations"). It is foreseeable that the supervisions on fund investment advisory institutions will strictly follow the relevant regulatory rules of fund management companies and the compliance management, internal control and risk management of fund investment advisory institutions will face higher standards in the future. More explicit regulations and requirements will be applied to the business definitions, service models, liabilities, prohibited actions, information disclosure, risk disclosure, promotion etc. of fund investment advisory services. As of December 31, 2021, 58 institutions have obtained the fund investment advisory qualifications, among whom 22 are fund management companies, 29 are securities companies, 3 are fund distribution institutions, and 4 are other financial institutions[1].

The core elements of the fund investment advisory business include products, strategies, investment advice and clients. From global perspective, fund investment advisory business includes four different forms: "intelligent investment advisory", "intelligent + artificial investment advisory ", "investment advisory" and " financial management". Under the current regulatory framework, there is no need for a service provider to file or register with CSRC if the fund investment advisory service is ancillary to its fund distribution service, and no separate contract is signed and no separate service fee is charged for the ancillary service. However, the basic legal relationships for fund distribution business shall be followed within the current regulatory framework and distributors are prohibited from engaging in any discretionary fund investment advisory service.

This article mainly analyzes key compliance issues and industry concerns in course of the fund investment advisory business under the Fund Investment Advisory Regulations, including internal decision-making and process control for fund investment advisory strategies, additional requirements for discretionary fund investment advisory services, management of investor suitability and promotion activities, management of conflicts of interest and establishment of effective segregation mechanism, and declaration and information disclosure, etc. for your reference.

Key aspects of compliance and internal control for fund investment advisory business

1. Internal decision making and process control of fund investment advisory business

2. Additional requirements for discretionary investment advisory business

3. Management of investor suitability and promotional activities

4. Management of conflicts of interest and establishment of effective segregation

5. Declaration and information disclosure

6. Other compliance and internal control requirements

Note: The implementation of certain key points of above compliance and internal control shall depend on the finalization of relevant draft rules.

The regulatory system for fund investment advisory business continues to improve

In response to the "grey area" in the development of fund investment advisory business, the recently issued Fund Investment Advisory Regulations clarify these issues and would comprehensively regulate the qualification conditions, internal management, service models, risk disclosure, promotion, asset display and service evaluation. The Fund Investment Advisory Regulations aim to establish a multi-dimensional legal and compliance system for the future development of fund investment advisory business, fully reflecting the principles of orderly entry/exit, mutual balance, structural optimization, and risk matching.

We are also paying attention to discussions of certain business models in the market:

Model 1: fund managers list a series of fund portfolios on the fund distributors’ business outlets/websites without charging separate fee or signing separate fund investment advisory agreement, whereas the fund manager will be displayed as the manager of the fund portfolio;

Model 2: fund distributors sell mutual fund products on a commission basis and provide one-click ordering services without a separate fee. Each fund subscription ratio has been configured by default, but the investors may modify the subscription ratio of each fund at their discretion;

Model 3: a key opinion leader in the fund business acts as the portfolio manager and relevant funds remain in the investor's own account; after the investor has subscribed a fund portfolio, the system will automatically allocate the funds to relevant portfolio per the ratio adopted by such portfolio manager.

We believe the legal application and compliance of above-mentioned business models will be further clarified. According to the Fund Investment Advisory Regulations, institutions with non-compliant business models would not be allowed to conduct new non-compliant activities in providing fund investment portfolio strategy recommendations. This includes not presenting or launching new fund investment portfolio strategies, not adding new clients to existing fund investment portfolio strategies, and not providing additional portfolio strategy investments for existing clients. In addition, clients would be prominently alerted that the institution is in the process of rectifying its fund investment advisory activities and that there is a risk that services cannot be provided uninterrupted in the future.

We will continue to closely monitor the development and implementation of the Fund Investment Advisory Regulations, and how they can be effectively applied to various business scenarios and embedded into the institutions’ internal control frameworks, and work with market participants in connection with legal, compliance, and risk management issues in the development of fund investment advisory business.

[1] http://www.csisc.cn/zbscbzw/jjtzgw/202109/f1e411bef5f64a0595ed9aa09a4f030f.shtml.