On March 15, 2019, the Foreign Investment Law of the People's Republic of China[1] was adopted at the Second Session of the Thirteenth National People's Congress, which will become effective on January 1, 2020. The law was adopted quickly following its first submission to the NPC Standing Committee for deliberation on December 23, 2018, reflecting the legislative body's strong determination to create a basic legal system to replace the "three foreign-invested enterprise laws"[2] and serve as the foundation for foreign investment in China.

The Foreign Investment Law provides clear provisions on issues of common concern for foreign-invested enterprises and their investors, such as the pre-access national treatment plus negative list system, the equal application of all national policies to foreign-invested enterprises, no expropriation of foreign investments under unexceptional circumstances, liberalization of inbound and outbound remittances, concentration of undertakings reviews and foreign investment security review systems. For more analysis, please see our related article, Interpreting the Foreign Investment Law: In a Nutshell.

However, the Foreign Investment Law has also left more than a few open questions, many of which remain topics of interest. This article will analyze these open questions.

I. Temporarily shelving VIE structure issues

The variable interest entity ("VIE") structure, also known as "agreement control" or "contractual arrangement", refers to the use of a series of agreements, rather than equity ownership, to achieve actual control of domestic operating entities and consolidation into the financial statements.

Since Sina completed its NASDAQ listing by adopting a VIE structure in 2000, VIE structures have been widely used by Chinese companies involved in foreign investment-restricted or -prohibited industries (such as TMT, private education, etc.) to raise foreign capital by creating red chip structures or completing overseas IPOs. However, currently effective Chinese laws and regulations have yet to clearly determine the nature of VIE structures.

Article 15 of the 2015 consultation draft of the Foreign Investment Law (the "Comment Draft") for the first time clearly defined VIE structures as a form of foreign investment. However, the first draft for deliberation in 2018 of the Foreign Investment Law ("First Review Draft") removed all provisions referring to "agreement control" or "actual controller". In their place, a catch-all clause was added which stipulated that "foreign investment" includes "investments made by foreign investors in China through other means as provided by laws, administrative regulations or by the State Council." This catch-all clause has been retained in the final Foreign Investment Law[3].

We tend to believe that the current focus of the Foreign Investment Law is to expand opening-up, clarify the pre-access national treatment plus negative list system, and ensure an equally competitive environment for domestic and foreign investors under the background of the coming 40th anniversary of reform and opening-up and continuation of Sino-U.S. trade frictions and consultations. The Foreign Investment Law temporarily shelves many controversial issues that are less urgent, leaving them for later legislative authorization, such as the legality of VIE structures and identifying foreign investment based on actual control rather than place of registration (i.e., the actual control concept proposed in the Comment Draft). Therefore, Article 2, para. 2 of the Foreign Investment Law leaves open the possibility that VIE structures may still be included in the regulatory scope of "foreign investment" through special laws, or administrative regulations or even normative documents formulated by the State Council.

For more analysis of VIE structures, please refer to our related article, Interpreting Draft Foreign Investment Law from VIE Perspectives.

II. The Foreign Investment Law applies to Hong Kong, Macao and Taiwan investors on a "reference or comparison" basis, with supporting regulations possibly to come

Hong Kong SAR, Macao SAR and Taiwan are a part of China, and are also classified as independent customs zones. Thus, investments from Hong Kong, Macao and Taiwan are regarded neither as entirely foreign nor entirely domestic. In practice, the Chinese government has long administered Hong Kong, Macao and Taiwan-sourced investments by reference to foreign investment laws.

In fact, Articles 162 and 163 of the Comment Draft stipulated that the law would apply by reference to investments in mainland China made by Hong Kong, Macao and Taiwan investors and overseas Chinese investors, except as otherwise provided by laws and administrative regulations. However, the First Review Draft removed these provisions, which were also missing from the final Foreign Investment Law.

In this regard, at a press conference on the Second Session of the Thirteenth National People's Congress held on March 4, 2019, Mr. Zhang Yesui, spokesperson for the Second Session, stated that: "In practice, the government administers Hong Kong, Macao and Taiwan investments by reference to foreign investment. The Foreign Investment Law will not change this arrangement for the application of law. And the relevant systems will be continuously revised and improved in accordance with practical needs, and further provide a more open and convenient business and development environment for Hong Kong, Macao and Taiwan investments[4]."

On the morning of March 15, Premier Li Keqiang held a press conference at the conclusion of the Second Session. While taking questions from journalists, Premier Li stated: "Hong Kong, Macau and Taiwan investment can refer to or comparatively apply the just-adopted Foreign Investment Law, and some of the institutional arrangements and actual practices that have worked well for a long time will continue to be followed, not only will this not disturb [investment], it will help attract investment from Hong Kong, Macau and Taiwan[5]." We expect that, in the future, the National People's Congress and its Standing Committee or the State Council may further introduce supporting regulations to clarify the laws that apply to Hong Kong, Macao and Taiwan investors and the enterprises which they establish in mainland China in order to attract Hong Kong, Macao and Taiwan investment.

III. Three types of foreign-invested enterprises need to adjust corporate governance structures during the transition period

In order to establish unified rules for domestic and foreign-invested enterprises, Article 31 of the Foreign Investment Law clearly stipulates: “The organizational form and organizational structure of foreign-invested enterprises shall be governed by the Company Law of the People’s Republic of China and the Law of the People’s Republic of China on Partnership Enterprises.” Article 42 of the Foreign Investment Law further provides that the three foreign-invested enterprise laws will be repealed as of January 1, 2020, and that foreign-invested enterprises established under these laws before the Foreign Investment Law becomes effective may retain their original organizational form for a period of five years.

Thus, a majority of foreign-invested enterprises face the problem of completing necessary internal adjustments during this five-year transition period to comply with the Company Law, which will come to uniformly apply to both domestic and foreign-invested enterprises. These adjustments are not expected to be easy.

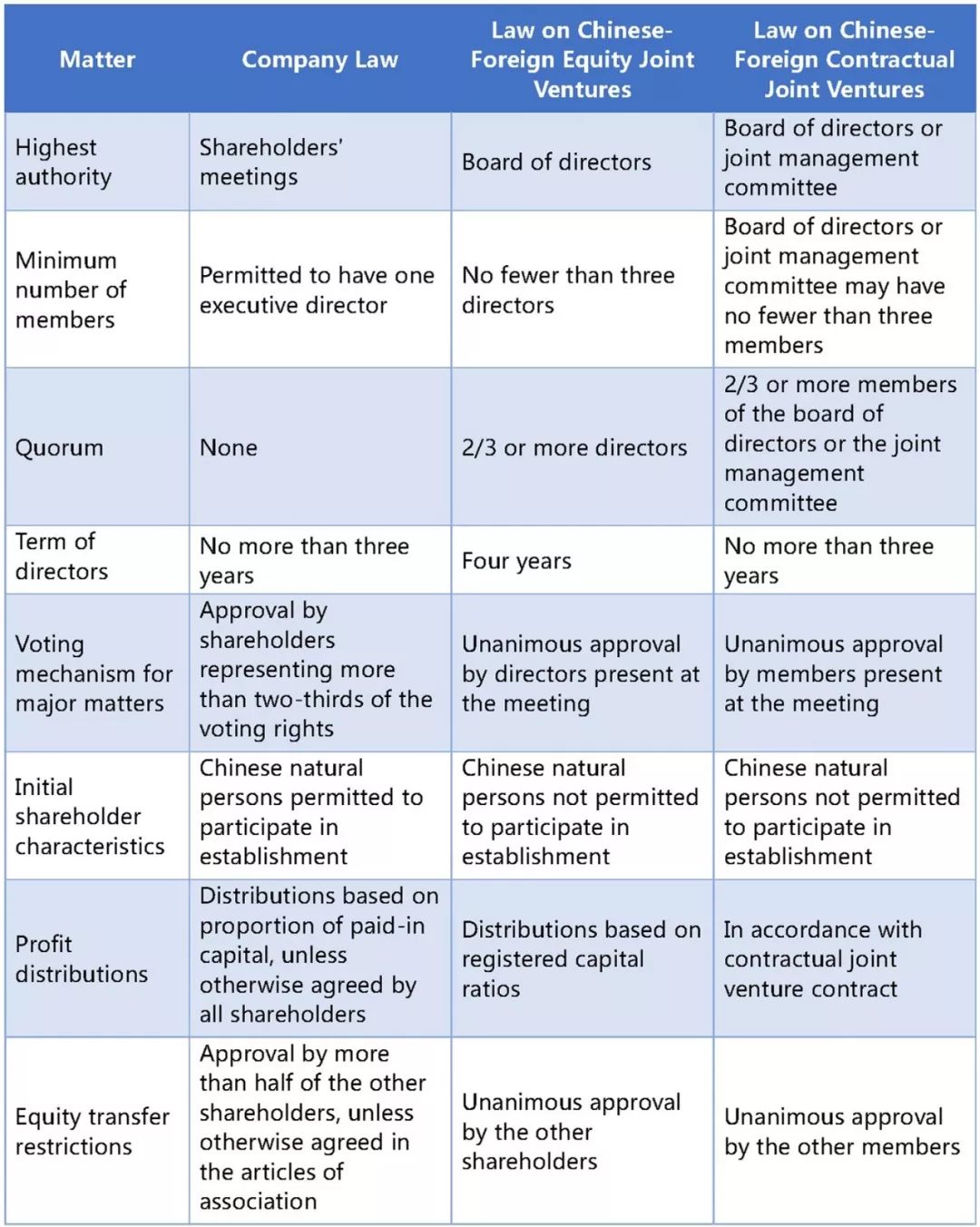

The Company Law sees significant differences compared to the currently effective Law on Chinese-Foreign Equity Joint Ventures and Law on Chinese-Foreign Contractual Joint Ventures, including but not limited to the following:

In practice, there is some controversy as to whether a joint venture can conform to the Company Law, whose provisions differ significantly from the Law on Chinese-Foreign Equity Joint Ventures. For example, can a joint venture stipulate in its contract and articles of association that a two-thirds affirmative vote of voting directors is required to approve a major event? And can a joint venture stipulate in its contract that equity transfers only require the consent of more than half of the other shareholders, or even stipulate that certain or all shareholders have the right to freely transfer their shares? Although there are no definite answers to these questions, and we believe the answers will vary depending on specific circumstances, the existence of such questions is sufficient evidence to prove that it has become difficult for the three foreign-invested enterprise laws to meet the needs of reform and opening-up.

With respect to the highest authoritative body, joint ventures will need to establish new shareholders' meeting systems to inherit rights from their boards of directors as described in the Company Law, and will need to establish new voting mechanisms. These adjustments will possibly result in conflicts between joint venture parties.

By contrast, a more pressing issue is whether existing foreign-invested enterprises during the transition period should comply with the new Foreign Investment Law by reference (and if so, how), or whether they should continue to comply with the then-repealed three foreign-invested enterprise laws (that is, will the laws remain effective for those existing foreign-invested enterprises?). We believe that these issues need to be clarified before the new Foreign Investment Law comes into effect on January 1, 2020.

IV. Foreign investment promotion policy to be carefully opened to local government, which is worth looking forward to

Both the First Review Draft and the Second Review Draft stipulated in Article 18 that "local governments at various levels may formulate foreign investment promotion policies within their statutory authority." Some local governments had long issued certain preferential policies in terms of taxation, income and finance in order to attract foreign investment which were all subsequently suspended by the Circular of the State Council on Stocktaking and Regulation of Preferential Policies for Taxation and Related Issues (Guo Fa [2014] No. 62). Article 18 therefore raises similar concerns about local governments abusing their authority and uncertainty about the future suspension of similar local preferential policies.

Article 18 was revised in the Third Review Draft to further clarify that governments at or above the county level can only formulate policies and measures to promote and facilitate foreign investment within their statutory authority in accordance with the provisions of laws, administrative regulations and local regulations. This new provision was also adopted in the new Foreign Investment Law.

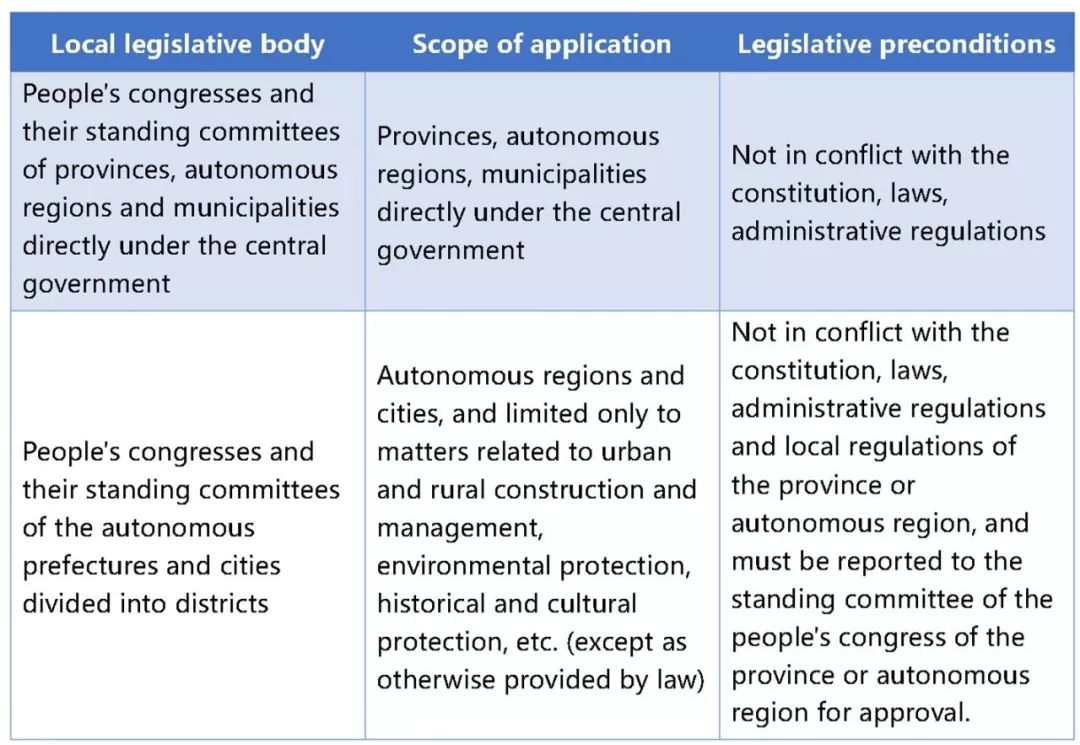

According to the Legislation Law, the legislative body, scope of application and legislative preconditions of local regulations are shown in the following table.

The highlight of the above amendment is to add "local regulations" to the legal basis for developing local preferential policies. In practice, except for some regions of strategic significance such as the Guangdong-Hong Kong-Macao Greater Bay Area, local governments will find it difficult to count on a national law basis for their local foreign investment promotion policies. "Local regulations" may address this concern by not causing the requirements under Article 18 to be too high so as to become impractical, but also not too low so as to invite abuses of authority.

It will be worthwhile to see how the local governments use the convenience provided by "local regulations" to formulate local foreign investment promotion and facilitation policies and measures.

[1] http://www.npc.gov.cn/npc/xinwen/2019-03/15/content_2083532.htm

[2] Refers to the currently effective Law of the People's Republic of China on Foreign-Capital Enterprises, Law of the People's Republic of China on Chinese-Foreign Contractual Joint Ventures and Law of the People's Republic of China on Chinese-Foreign Equity Joint Ventures.

[3] The clause reads as "investment made by foreign investors through other means as provided by law."

[4] http://www.npc.gov.cn/npc/zhibo/zzzb44/node_381.htm

[5] http://www.xinhuanet.com/politics/2019lh/2019-03/15/c_1124239569.htm

Interpreting the Foreign Investment Law: Uncharted Waters

作者:AdrianLv HuanhaoHe来源:汉坤律师事务所

On March 15, 2019, the Foreign Investment Law of the People's Republic of China[1] was adopted at th