Following the issuance of the Interim Measures for Administration of the Issuance of Bonds by Overseas Institutions in the National Interbank Bond Market (《全国银行间债券市场境外机构债券发行管理暂行办法》) ("Circular No.16") by the People's Bank of China ("PBOC") and the Ministry of Finance ("MOF") on September 8, 2018, the National Association of Financial Market Institutional Investors ("NAFMII") officially issued the Guidelines on Debt Financing Instruments of Overseas Non-financial Enterprises (for Trial Implementation) (《境外非金融企业债务融资工具业务指引(试行)》) (the "NAFMII Guidelines") on January 17, 2019. The NAFMII Guidelines provide specific rules and operational requirements for overseas non-financial enterprises to issue debt financing instruments in the China Interbank Bond Market ("CIBM").

We intend to introduce the main contents of the NAFMII Guidelines in this article.

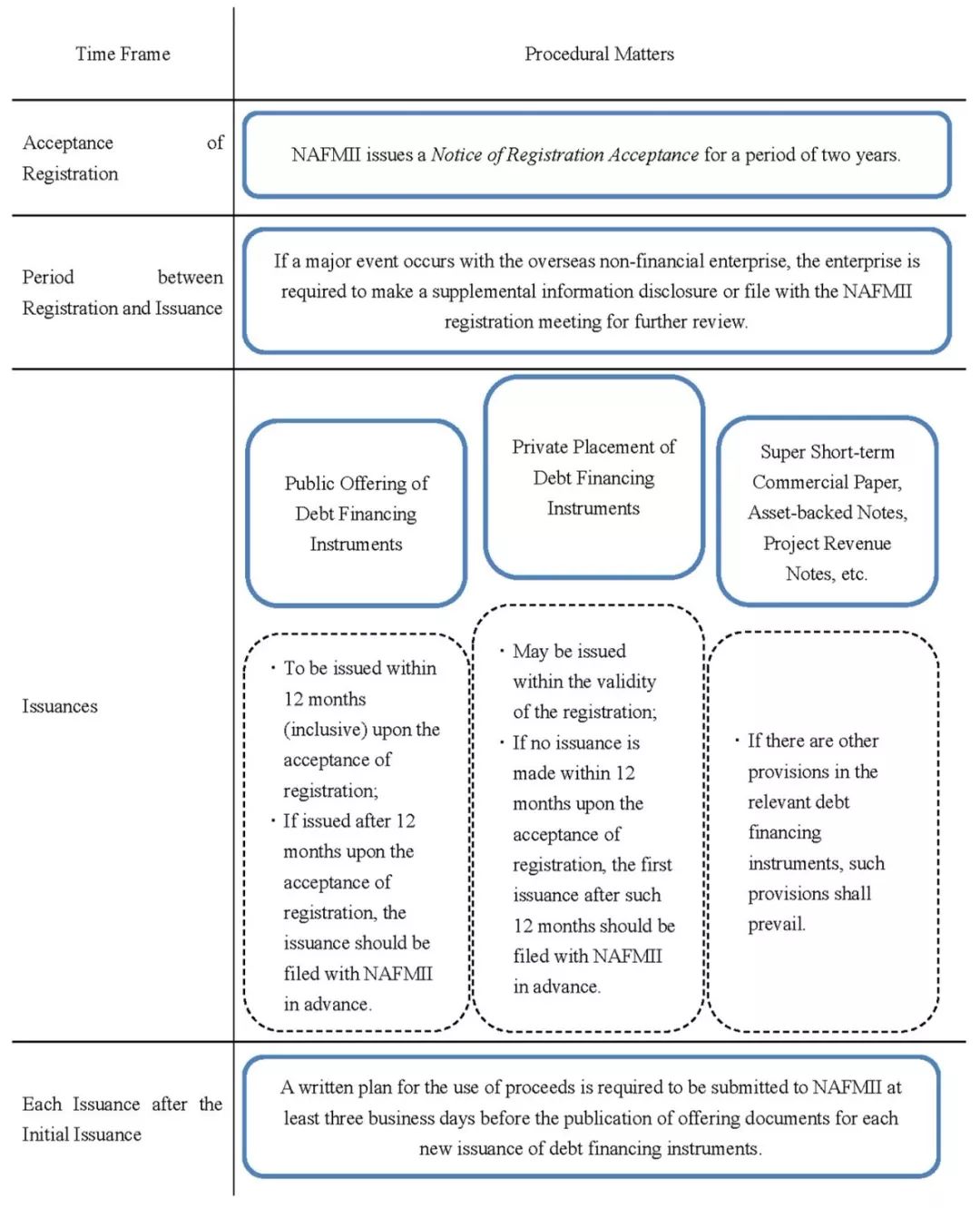

I. Further Clarifying the Requirements for the Registration and Issuance of Panda Bonds by Overseas Non-financial Enterprises

According to the NAFMII Guidelines, the registration requirements and methods of issuing debt financing instruments by overseas non-financial enterprises are generally consistent with those for domestic non-financial enterprises. For example, debt financing instruments issued by overseas non-financial enterprises are also required to be registered with NAFMII and overseas non-financial enterprises may issue debt financing instruments in the same manner with domestic non-financial enterprises as stipulated in the Rules for the Registration and Issuance of Debt Financing Instruments of Non-financial Enterprises (《非金融企业债务融资工具发行注册规则》).

Specifically, the NAFMII Guidelines further clarify the requirements for registration and issuance procedures as follows:

In addition, debt financing instruments issued by overseas non-financial enterprises should be underwritten by financial institutions qualified to act as underwriters for debt financing instruments issued by non-financial enterprises. In particular, the NAFMII Guidelines require that at least one lead underwriter has a subsidiary or branch in the country or region where the overseas non-financial enterprise is incorporated or carries out its principal business, or make other necessary arrangements to ensure that it has the ability to conduct due diligence and other work related to the underwriting of such debt financing instruments.

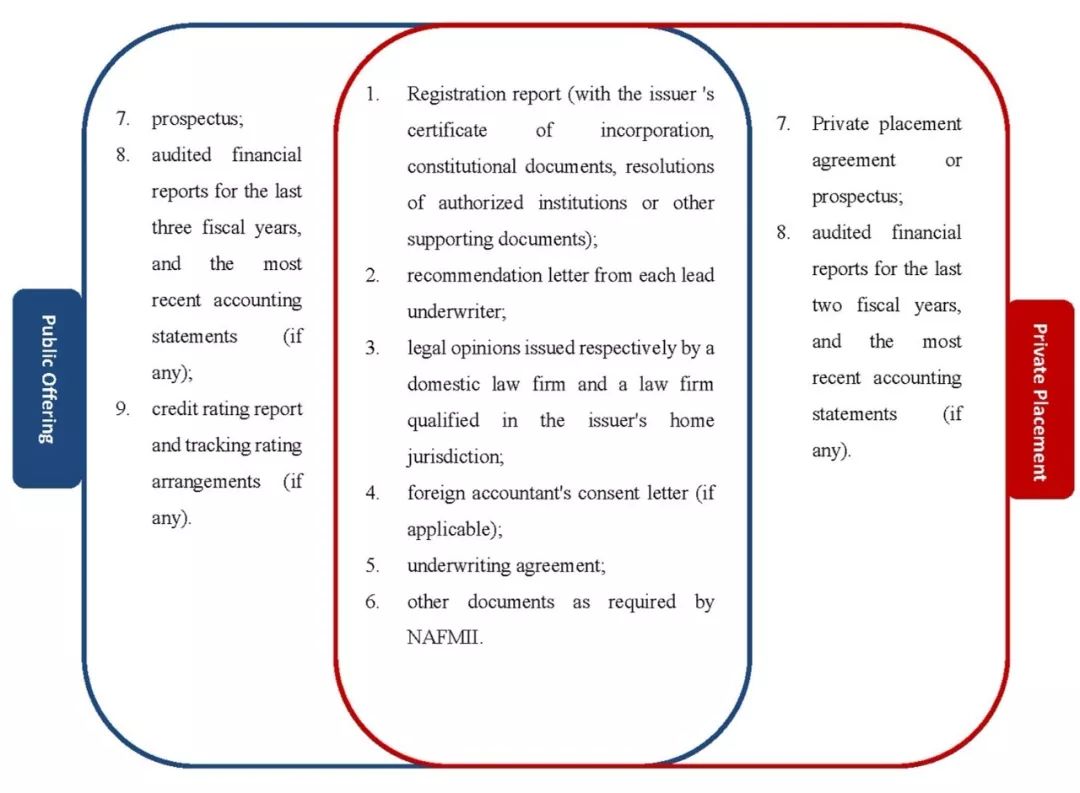

II. Specifying the Requirements for Registration Documents for Overseas Non-financial Enterprises to Issue Panda Bonds in the CIBM.

The NAFMII Guidelines also specify relevant requirements for registration documents for different issuance methods (including public offerings and private placements):

As shown in the table above, most registration documents for these two issuance methods are the same (items 1 to 6), while the requirements for financial reports and credit rating reports are different.

III. Debt Proceeds Allowed to Be Used Outside of China

The NAFMII Guidelines separately set out the requirements for the use of debt proceeds, and clarify the principles of the use of proceeds from debt financing instruments issued by overseas non-financial enterprises, which include:

1. Proceeds can be used within or outside of China according to relevant laws, regulations and regulatory requirements, which provide a clear regulatory basis for overseas non-financial enterprises to transfer proceeds out of China for use offshore;

2. Account opening, cross-border settlement, information reporting and other matters related to debt financing instruments issued by overseas non-financial enterprises shall comply with the relevant provisions of the PBOC and the State Administration of Foreign Exchange;

3. The use of proceeds shall comply with relevant laws and regulations and national policy requirements, and overseas non-financial enterprises shall strictly perform relevant information disclosure obligations in accordance with the use of proceeds disclosed in the prospectus; in case of any changes to the use of proceeds, the overseas non-financial enterprise will conduct relevant change formalities and disclose at least five business days prior to such changes.

As mentioned above, the NAFMII Guidelines expressly allow overseas non-financial enterprises to use debt proceeds offshore. However, the specific legal compliance standards for the use of proceeds and the operational procedures for changing the use of proceeds still need to be further clarified.

IV. Further Requirements for Financial Statements of Overseas Non-financial Enterprises

Based on Circular No. 16, the NAFMII Guidelines put forward further requirements for the submission and disclosure of financial statements by overseas non-financial enterprises. That is, for issuers who prepare consolidated statements, in addition to submitting or disclosing their consolidated statements, the NAFMII Guidelines also require them to:

1. submit and disclose the standalone financial statements of the parent company; or

2. disclose the content in the standalone financial statements of the parent company that may have a material impact on investors' decision-making, and make such information prominent in the issuance documents to draw investors' attention.

It is apparent that NAFMII has become more cautious about the disclosure and examination of financial statements of overseas non-financial enterprises. For overseas non-financial enterprises that prepare consolidated financial statements, investors can have a better understanding of the financial status of the issuer by reviewing the financial statements or major financial matters of the parent company.

V. Information Disclosure

Circular No. 16 provides detailed rules on information disclosures for issuing panda bonds in the CIBM, including but not limited to the principle of authentic, complete and equivalent disclosure, disclosure targets, and requirements for relevant accounting standards and audit requirements. The NAFMII Guidelines further refine the operational rules relating to disclosure matters.

1. Applicable disclosure rules. The NAFMII Guidelines require overseas non-financial enterprises to disclose financial information on a regular basis. Disclosure of information as well as major events during the term of the debt financing instruments should be included in the registration and issuance documents in accordance with the Rules for Information Disclosure on Debt Financing Instruments of Non-financial Enterprises in the China Interbank Bond Market (《银行间债券市场非金融企业债务融资工具信息披露规则》) (the "Information Disclosure Rules").

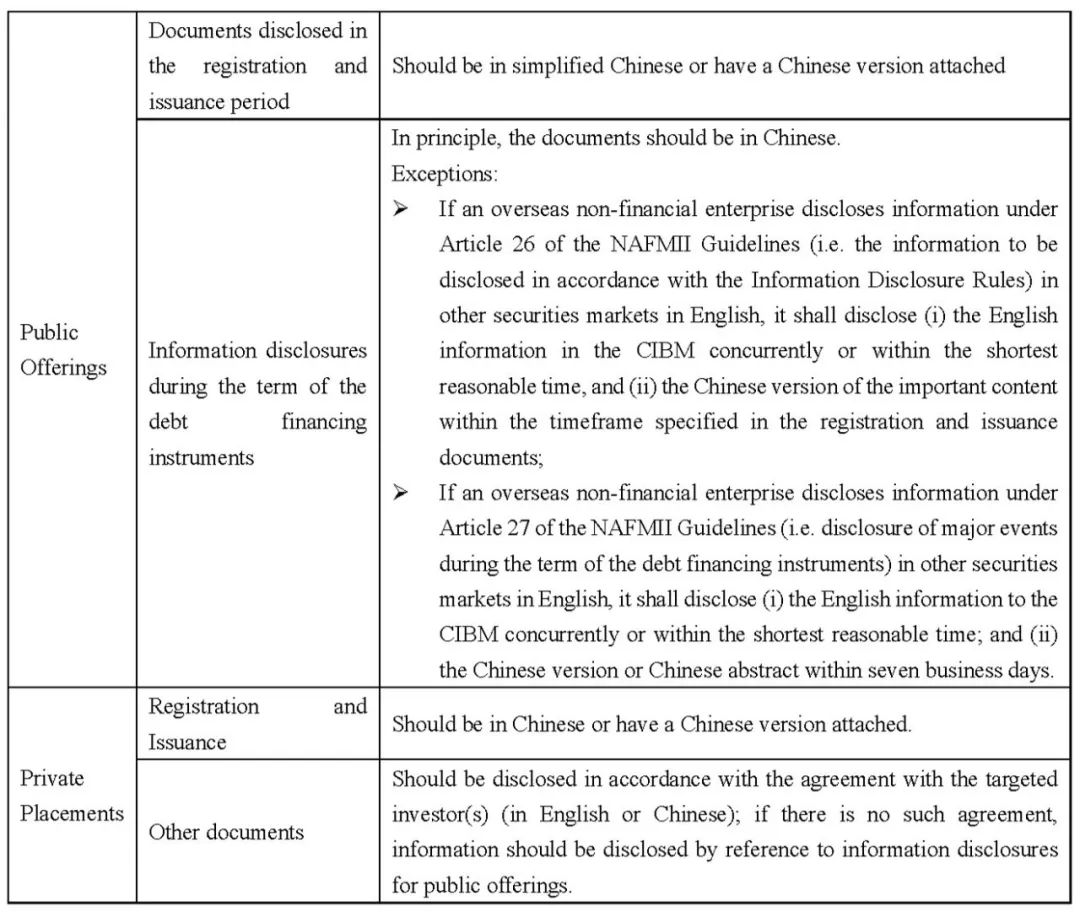

2. The language of the disclosure documents. The NAFMII Guidelines provide the following requirements:

3. Disclosure requirements for credit enhancement agencies. Where an offshore credit enhancement agency provides credit enhancement to the issuer, the relevant information disclosure of the credit enhancement agency shall be in accordance with the requirements to such issuer. However, the information to be disclosed will be separately prescribed by NAFMII where an offshore parent company provides an unconditional, irrevocable joint liability guarantee for its wholly-owned subsidiary.

VI. Applicable law

Prior to the issuance of Circular No.16, the Interim Measures for Administration of Issuing Renminbi Bonds by International Development Institutions (《国际开发机构人民币债券发行管理暂行办法》) [1] explicitly stipulated that any breach of contract or other disputes arising out of or in connection with the issuance of renminbi-denominated bonds within China by an international development institution was to be governed by PRC law. Circular No. 16 does not contain any mandatory provisions relating to the applicable law.

However, the NAFMII Guidelines clearly stipulate that the offering and transaction documents for issuances of debt financing instruments by overseas non-financial enterprises should be governed by PRC law. Based on these requirements, we understand that when overseas non-financial enterprises issue panda bonds, they should follow the requirements of the NAFMII Guidelines and ensure that the transaction documents (including prospectuses, private placement agreements, etc.) are governed by PRC law.

Based on Circular No.16, the NAFMII Guidelines further supplement and refine the special provisions for the issuance of panda bonds in the CIBM by overseas non-financial enterprises, and provides guidance for overseas non-financial enterprises to issue panda bonds (in particular, specific operational requirements for registration documents and subsequent disclosure documents are provided). Moreover, the requirements of the NAFMII Guidelines are consistent with the existing rules on the issuance of debt financing instruments by non-financial enterprises, which indicates that the issuance rules for domestic issuers and foreign issuers should be as consistent as possible. This will facilitate the effective supervision and management of debt financing instruments issued by domestic or overseas non-financial enterprises.

Please kindly note that the NAFMII Guidelines are currently only at the trial stage, which leaves room for further adjustments in the future. Due to different legal requirements for corporate governance in different jurisdictions, certain diversity in overseas non-financial enterprises, and the differences in establishment, registration and constitutional documents between domestic enterprises and offshore enterprises (particularly those incorporated in common law jurisdictions), further clarification is needed as for how to manage and restrict different types of overseas non-financial enterprises as issuers and propose appropriate requirements. We will continue to pay attention to the relevant rules newly issued by the regulatory authorities such as PBOC or NAFMII.

[1] Interim Measures for Administration of Issuing Renminbi Bonds by International Development Institutions has been officially abolished by Circular No.16.

The above is a preliminary review of certain key points of the NAFMII Guidelines. If you need further information on the above matters, please contact:

Rules for Overseas Non-financial Enterprises Issuing Panda Bonds

作者:ShuWang JunZhuTie ChengYang JunWan YinGe来源:汉坤律师事务所

Following the issuance of the Interim Measures for Administration of the Issuance of Bonds by Overse