Recently, the Stock Exchange of Hong Kong Limited (“SEHK”) has published the New Board Concept Paper for the purpose of seeking market feedback on SEHK’s proposed establishment of a New Board. This newsletter is a brief introduction to the New Board Concept Paper.

Background: Ensuring Continued Success of Hong Kong’s IPO Market

Under the current listing framework, the Hong Kong security market has high industry concentrations and is underweight in high growth sectors, meaning that the competitiveness of HKEX as an IPO venue is facing challenge.

Companies from New Economy industries (such as Biotechnology, Health Care Technology, Internet & Direct Marketing Retail, Internet Software & Services, IT Services, Software, Technology Hardware, Storage & Peripherals) that have listed on Hong Kong market in the past ten years make up only 3% of Hong Kong’s total market capitalisation, as compared with 60%, 47% and 14% for NASDAQ, NYSE and LSE, respectively. Moreover, Hong Kong security market has minimal weightings in some of the fastest growing industries globally: Pharmaceuticals, Biotechnology & Life Sciences (1%),Healthcare Equipment & Services (1%) and Software & Services (9%, or 1% if Tencent is excluded).

Meantime, the Mainland listing venues and regulator have pursued a series of measures to improve the attractiveness of Mainland venues for emerging and innovative companies to raise equity capital in recent years. Among these were the launch of ChiNext and NEEQ in 2009 and 2012. The Mainland listing venues and regulator have also released an announcement regarding a path to step-up from NEEQ to a listing on ChiNext and plan for registration-based reform to improve the listing process.

One major attraction of the US market for many such companies is that Weighted Voting Rights (“WVR”) structures are permitted there, whereas the Hong Kong market does not allow them. Moreover, 18 out of 33 (55%) US-listed Mainland Chinese companies with WVR structures, accounting for 84% of market capitalisation, are from precisely the information technology industry that the Hong Kong market is underweight in.

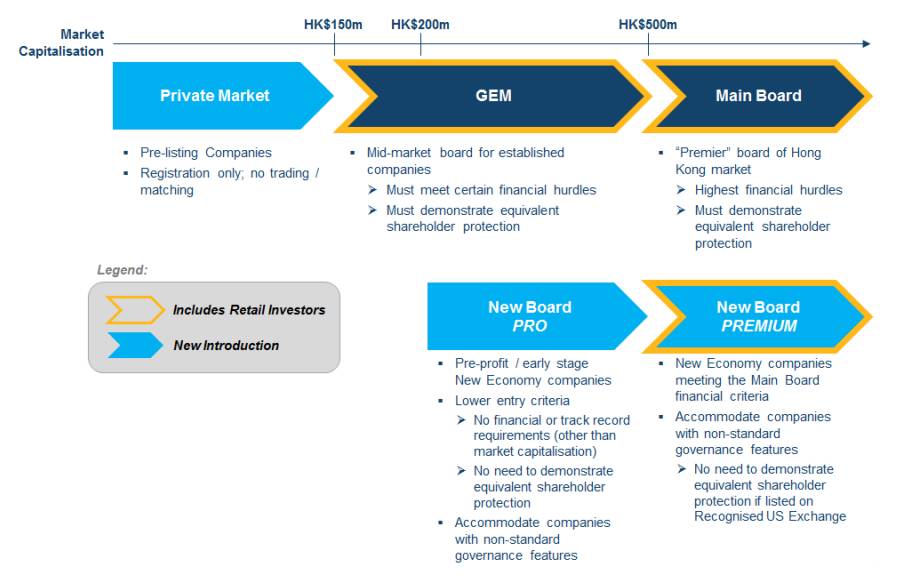

To complement and supplement the existing listing framework, open up to a more diverse range of issuers, broaden the capital market access in Hong Kong and ensure that only pre-profit companies with high growth potential or New Economy companies can apply to list in Hong Kong, SEHK proposes to establish a New Board, separate from the Main Board and the GEM.

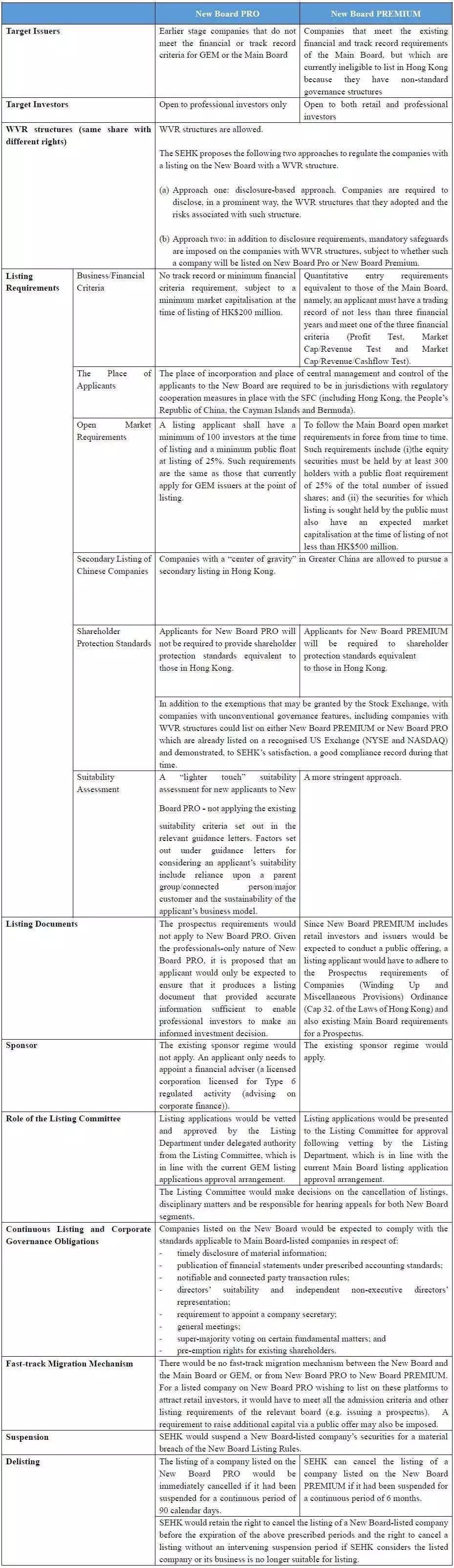

New Board PRO or New Board PREMIUM?

Vision for Hong Kong’s Future Listing Framework

(1) The Main Board would be positioned as a “premier board” with an increased minimum market capitalisation requirement of HK$500 million (raised from HK$200 million), along with existing financial and track record criteria.

(2) GEM would serve the needs of small and mid-sized issuers that meet its financial and track record criteria and desire to attract retail as well as professional investors.

(3) The New Board would fill the gaps in Hong Kong’s current listing framework, so that the needs of New Economy and early-stage companies could be accommodated while maintaining appropriate regulatory and shareholder protection standards.

Proposed Corresponding Reform of and Changes to the GEM and Main Board

(1) The SEHK proposes removing the “stepping stone” concept (GEM as a stepping stone to the Main Board) and the streamlined process for transfers from GEM to the Main Board. This means that GEM Transfer applicants will be required to appoint a sponsor and issue a “prospectus-standard” listing document.

(2) All GEM Transfer applicants shall have published and distributed at least two full financial years of financial statements after their GEM listings before they can be considered for a GEM Transfer.

(3) The initial listing requirements in GEM Board will be raised (including increasing minimum market capitalisation requirement from HK$100 million to HK$150 million, increasing minimum cash flow requirement from HK$20 million to HK$30 million and extending the lock-up on controlling shareholders upon listing from one year to two years).

(4) The initial listing requirements in Main Board will be raised (including increasing minimum market capitalisation requirement from HK$200 million to HK$500 million, increasing the minimum public float value from HK$50 million to HK$125 million and extending the lock-up on controlling shareholders upon listing from one year to two years).

For further details, please see the Consultation Paper on Review of the Growth Enterprise Market (GEM) and Changes to the GEM and Main Board Listing Rules which is available at the following link:

http://www.hkex.com.hk/eng/newsconsul/mktconsul/Documents/cp2017062.pdf

or, you may click the link at the bottom to read the full text of the two documents.

Hong Kong New Board – To Embrace the New Economy

作者:YurongYe FelixMiao FredricHuang来源:汉坤律师事务所

Recently, the Stock Exchange of Hong Kong Limited (“SEHK”) has published the New Board Concept Paper