The Stock Exchange of Hong Kong (“HKEx”) published its conclusion to its consultation on creating a new listing regime for special purpose acquisition companies (“SPAC”) in December 2021. The new addition to the Listing Rules, namely Chapter 18B which governs the listing of SPAC, shall become effective on 1 January 2022.

A SPAC is essentially akin to a shell company, utilised to raises funds through its listing for the purpose of acquiring a business, i.e. a De-SPAC Target. SPACs have emerged, over the years, as listing applicants in other stock markets, predominantly the US, as well as in Singapore. The new Chapter 18B of the Listing Rules stipulate the listing requirements for SPAC, as well as the framework for conducting the acquisition of De-SPAC Target i.e. a De-SPAC Transaction. It is observed that Hong Kong’s listing regime for SPAC is more stringent than that of other jurisdictions, where publication of listing documents is required for both the listing of SPAC and the completion of De-SPAC Transaction. Therefore, the SPAC regime in Hong Kong is a two-stage process, which include the listing of SPAC itself and the completion of the De-SPAC transaction within prescribed time. It is further noted that, for ease of identification, the stock short names of (1) SPAC shares will end with the marker “Z” and (2) SPAC warrants will end with “ZYYMM” or “ZYY” (with YY representing the expiry year and MM representing the expiry month).

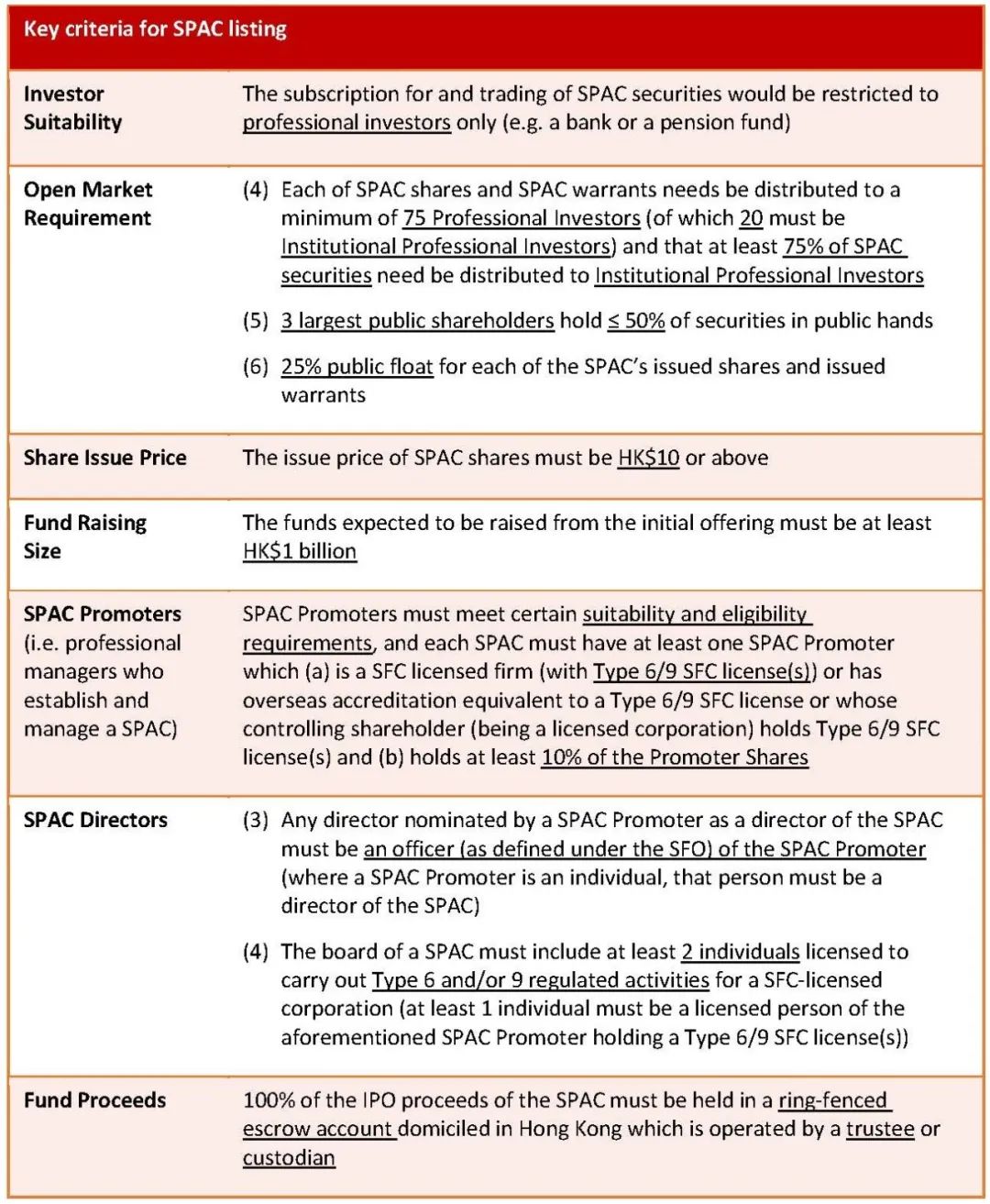

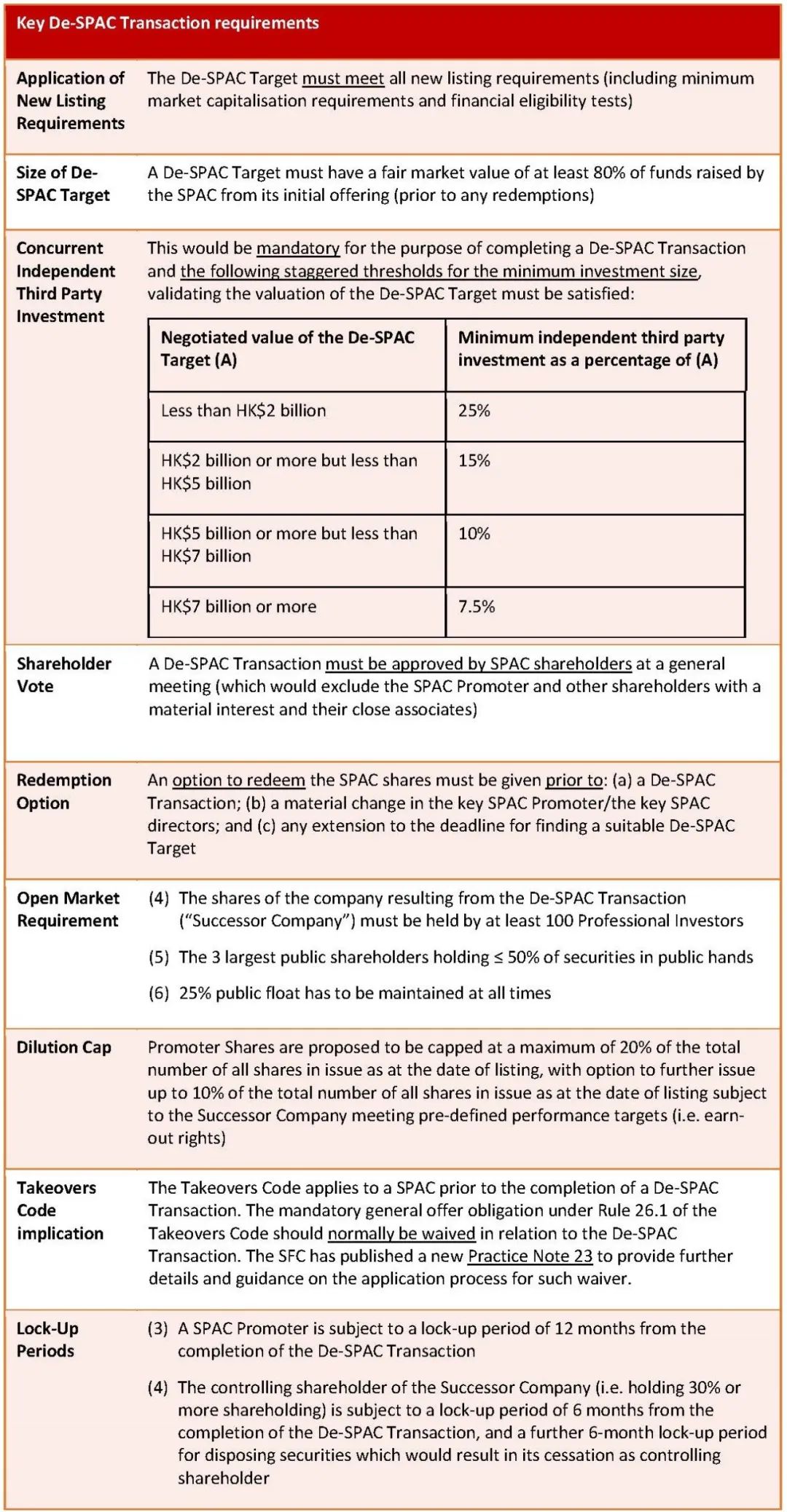

The key features of the Hong Kong SPAC regime are summarised as follows:

SPAC Listing

De-SPAC Transaction

The following summarises the key requirements of a De-SPAC Transaction, which shall be proposed within 24 months from the date of the SPAC listing and completed within 36 months from such listing, unless extension is granted by shareholders of SPAC and HKEx:

If a SPAC is unable (a) to announce a De-SPAC Transaction within 24 months of listing, (b) complete a De-SPAC within 36 months of listing, or (c) obtain the requisite shareholder approval for a material change in key SPAC Promoters/key SPAC directors within 1 month of such change, the SPAC must return 100% of the funds it raised (plus accrued interest) to its shareholders.

Hong Kong New Listing Regime for SPAC

作者:DennisFong BoscoLeung来源:通力律师事务所

The Stock Exchange of Hong Kong (“HKEx”) published its conclusion to its consultation on creating a