Against the backdrop of increasingly stringent IPO policies in China's A-share capital market in recent years, numerous enterprises have redirected their focus toward overseas capital markets, such as Hong Kong and the United States. This trend is particularly evident among Chinese enterprises with international expansion ambitions and globally oriented business strategies. The SPAC listing model has further provided these enterprises with an additional pathway to access overseas capital markets, including those in Hong Kong and the United States.

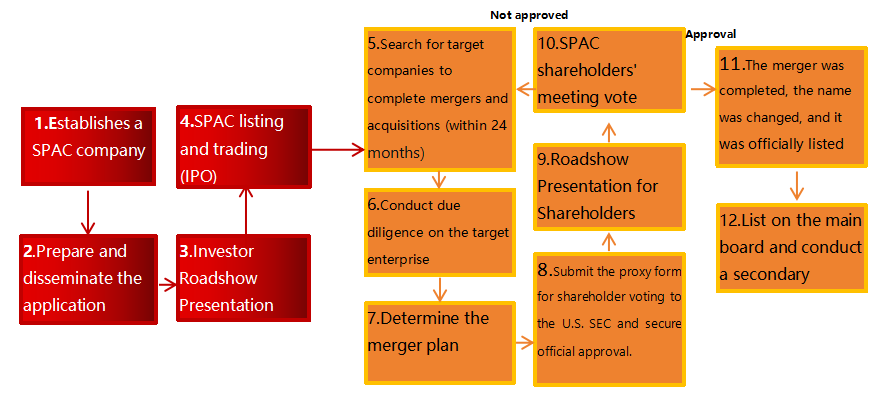

The full name of SPAC is "Special Purpose Acquisition Company", Unlike traditional initial public offerings (IPOs) and reverse mergers, the SPAC model follows a distinct process. Initially, a SPAC shell company, typically established by sponsors with expertise in private equity, investment banking, or senior industry experience, is formed as a cash-rich entity and subsequently goes public through an IPO (SPAC IPO). Following this, the SPAC identifies target companies for acquisition, conducts negotiations and due diligence, while simultaneously establishing a red-chip structure. Subsequently, the SPAC shell company merges with or acquires the target company (De-SPAC), thereby incorporating the target company into the public listing system and enabling its official entry into the capital market. Generally, SPACs have a timeframe of 18 to 24 months to identify and complete mergers with target companies. If a SPAC fails to complete the De-SPAC transaction within this period, it must seek approval from its shareholders to extend its operational timeline; otherwise, the SPAC will be liquidated.

Compared to the traditional IPO method, SPAC has gained significant favor among investors and companies planning to go public due to its advantages such as a shorter listing timeline, lower costs, simplified procedures, and higher efficiency. Originating from the U.S. capital market, SPAC listings were first accepted in 2003 and experienced rapid growth in 2020. In 2021, the securities markets of Singapore and Hong Kong introduced the SPAC listing mechanism. On January 20, 2022, VTAC, Singapore's first company listed under the SPAC model, officially debuted on the Singapore Exchange, marking it as the first mainstream Asian exchange to offer SPAC listings. On March 18, 2022, Aquila Acquisition, Hong Kong's first company listed under the SPAC model, officially commenced trading on the main board of the Hong Kong Stock Exchange.

I.Specific Steps of the SPAC Model (Taking the United States as an Example)

(Left: SPAC IPO Stage; Right: De-SPAC Stage)

(I)SPAC IPO

As outlined in the overview section, a Special Purpose Acquisition Company (SPAC) is established by professional entities such as private equity firms and investment banks. Its purpose is to raise capital through an Initial Public Offering (IPO) and subsequently acquire unspecified assets with growth potential. Acting as a "cash shell," the SPAC fulfills the investment objectives of its sponsors by merging with target companies that possess tangible operating assets and promising development prospects post-IPO.

The term "SPAC IPO" refers to the process wherein the SPAC, functioning purely as a financial vehicle, completes its public listing. Given that the acquisition of target companies following the IPO demands substantial expertise and experience in finance, overseas securities regulators and exchanges scrutinize the past investment track record and industrial background of the SPAC's sponsors and management team during the review process. Despite lacking operational business activities, SPACs typically undergo a more streamlined and expedited listing process compared to traditional IPOs. In practice, this phase generally requires a minimum of 8 weeks, often spanning 3 to 6 months, though it may extend up to 12 months in certain cases.

(II) De-SPAC (Red-chip Restructuring), ompleted listing

De-SPAC refers to a series of procedures wherein a Special Purpose Acquisition Company (SPAC), following the completion of its initial public offering, identifies a target company and executes mergers and acquisitions. Typically, this process must be finalized within 18 to 24 months post-IPO.

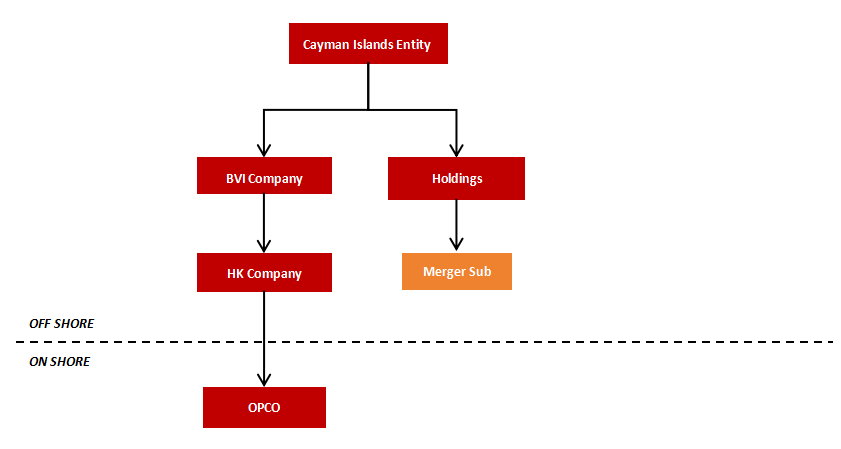

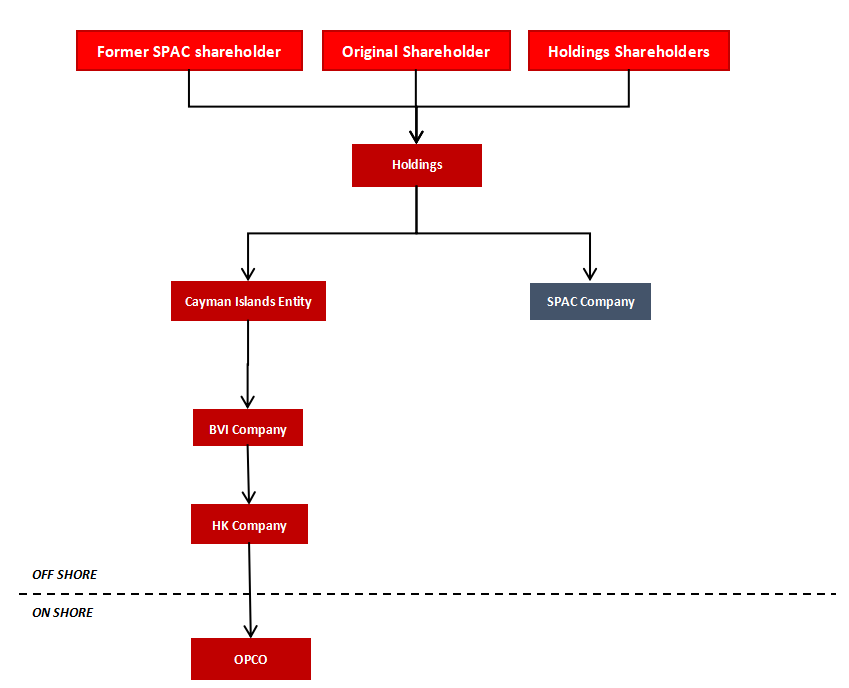

(1)Establishing a Red-Chip Restructuring Framework: Using the De-SPAC process in the U.S. stock market as an example, a target company based in China cannot directly merge with a SPAC entity to complete the De-SPAC transaction. To comply with the merger requirements, the target enterprise must undergo restructuring and establish a red-chip framework. At the outset of the project, domestic legal advisors will assist the target company in designing a red-chip restructuring plan and engage intermediaries to facilitate the establishment of the red-chip structure. Concurrently, international legal counsel will align with the merger transaction structure to assist the target enterprise in establishing an overseas group framework (such as creating merger subsidiaries, public companies, and other entities) through collaboration with external agencies. A typical De-SPAC red-chip restructuring framework involves equity exchange and reverse triangular mergers, as illustrated in the following example:

The Cayman Islands company establishes a wholly-owned subsidiary, structured as a Holdings, in the Cayman Islands. Subsequently, this Holdings forms a special-purpose vehicle (SPV) for mergers and acquisitions, named Merger Sub, in the registered location of the SPAC company (Cayman Islands).( The establishment of a British Virgin Islands (BVI) entity between a Cayman Islands company and a Hong Kong company is typically aimed at facilitating future expansion opportunities and optimizing tax planning. However, such a structure is not essential for constructing a red-chip structure.Public investors typically include industry-specific funds targeting companies with substantial valuation potential, arbitrage funds focused on the equity certificates of SPAC companies and confident in the SPAC management team's ability to complete mergers and acquisitions, funds concentrating on guaranteed-return investment categories, as well as associates of the sponsors. At the SPAC IPO stage, public investors contribute cash in exchange for investment units priced at $10 per unit. These units correspond to equity shares, warrants, voting rights, redemption rights, and interest income held in trust. For public investors participating in SPAC IPOs, the risks are relatively low due to the availability of redemption rights and fixed interest rates. Following the completion of a SPAC merger, the primary participants in the secondary market typically consist of hedge funds, mutual funds, and retail investors.)

1.The equity structure prior to the occurrence of the merger transaction

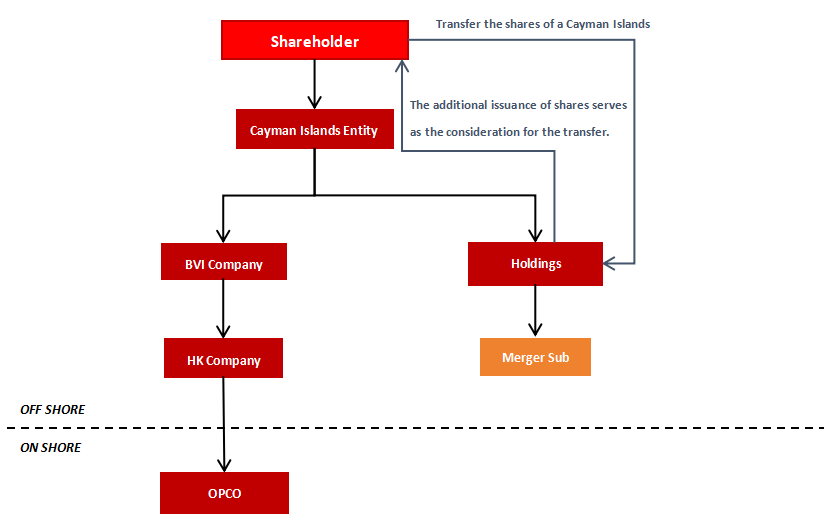

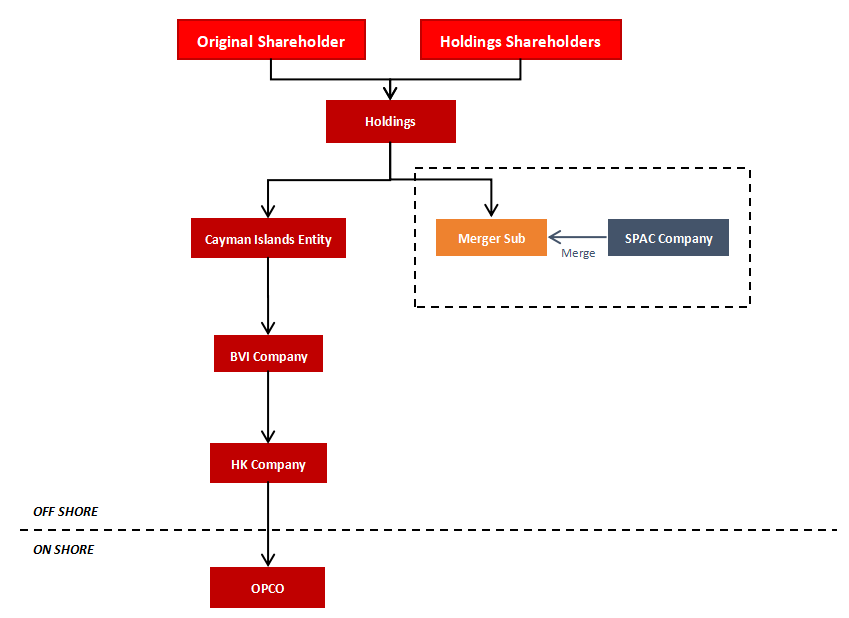

At the time of the merger transaction: 1) The shareholders of the Cayman Islands Company shall sell all their shares in the Cayman Islands Company to the Holdings in exchange for newly issued shares from the Holdings. Concurrently, the Cayman Islands Company shall return and cancel the shares it holds in the Holdings. Upon completion of this step, the Cayman Islands Company will become a wholly-owned subsidiary of the Holdings, and the shareholders of the Cayman Islands Company will become shareholders of the Holdings. 2) When a SPAC company merges with its Merger Subsidiary, the SPAC company will survive the merger as the continuing entity. Following the merger, the Holdings will hold all shares of the SPAC company. Additionally, the Holdings will issue shares and warrants to the original shareholders of the SPAC company.

2.The first step is equity transfer

3.The secondcep: Merge

4.The equity structure upon completion of the merger

(2)Preparation of Transaction Documents and Form 8-K Announcement: Following the preliminary determination of the target company, the domestic and international legal counsel, auditors, and other intermediary institutions engaged by the SPAC company will conduct comprehensive legal and financial due diligence on the target company. Concurrently, the domestic and international legal counsel of the target company will commence the preparation of the merger agreement and corresponding disclosure letter. Upon reaching consensus through multiple rounds of negotiations and consultations, the target company and the SPAC company will execute the merger agreement. Subsequently, the SPAC company will issue a Form 8-K announcement detailing the relevant aspects of the merger transaction within four business days following the execution of the agreement.

(3)Filing with the China Securities Regulatory Commission (CSRC):According to the relevant provisions of the "Trial Measures for the Administration of Overseas Securities Issuance and Listing by Domestic Enterprises" and its supporting guidelines (hereinafter referred to as the "New Regulations on Overseas Listing"), De-SPAC listing is categorized as an indirect overseas listing and must comply with the filing procedures required by the China Securities Regulatory Commission (CSRC). The filing materials should be submitted to the CSRC's online service platform within three working days following the announcement of the merger and acquisition transaction by the SPAC company (i.e., upon the release of Form 8-K). These materials are typically prepared by the Chinese legal counsel of the target company in accordance with the requirements stipulated under the New Regulations on Overseas Listing. For content involving financial data and overseas issuance details, the domestic legal counsel will collaborate with other project stakeholders (such as international legal advisors and auditors) to assist the target company in providing necessary supplements. Subsequently, the domestic legal counsel will coordinate with all parties involved in the project to prepare written responses addressing both the written and oral feedback received from the CSRC.

(4)Submission of the Prospectus Form F-4: Typically, during the preparation phase of the merger agreement or following its execution, the overseas legal counsel assumes primary responsibility for drafting the "prospectus" for the De-SPAC listing, specifically Form F-4. The domestic legal advisors of the target company are generally tasked with drafting sections concerning risk factors and regulations related to Chinese law, as well as reviewing and updating content pertaining to Chinese law within Form F-4. Analogous to traditional U.S. IPO procedures, Form F-4 may be initially submitted confidentially to the U.S. Securities and Exchange Commission (SEC) and subsequently transitioned to a public filing after multiple rounds of revisions in response to the SEC's comment letters.

(5)Closing and Overseas Listing: Upon receipt of the effectiveness notice from the U.S. Securities and Exchange Commission (SEC), the filing confirmation from the China Securities Regulatory Commission (CSRC), and the approval from the relevant stock exchange, as well as the shareholder approvals obtained through general meetings held by both the target company and the Special Purpose Acquisition Company (SPAC), the closing of the De-SPAC merger and acquisition transaction will be executed. Following the completion of the transaction, the Cayman Islands holding entity of the target enterprise will be listed and traded on an overseas securities market.

(6) Post-listing Matters: In compliance with the requirements of domestic and foreign regulatory authorities, after the listing is finalized, the listed company must file a Super 8-K or Form 20-F with the U.S. SEC (within four business days following the closing). The Form 20-F applies to Foreign Private Issuers. Additionally, the company must submit reports regarding its overseas issuance and listing to the China Securities Regulatory Commission (CSRC), though no specific time limit is mandated for this submission.

II.Submission to the China Securities Regulatory Commission

According to Article 15 of the "Trial Measures for the Administration of Overseas Listing" issued on February 17, 2023, if a domestic enterprise's revenue, total profit, total assets, or net assets in the most recent fiscal year exceed 50% of the corresponding figures in the issuer's audited consolidated financial statements for the same period, and its primary business activities or main operating premises are located within China, or if the majority of senior management personnel responsible for operations and management are Chinese citizens or reside habitually within China, such issuance shall be deemed as an indirect overseas listing by a domestic enterprise. Furthermore, Article 17 of the "Trial Measures for Administration" explicitly stipulates that if domestic enterprises achieve direct or indirect overseas listings of their assets through acquisitions, share swaps, transfers, or other transaction arrangements, they must complete filings in accordance with the relevant provisions outlined in Article 16 of the "Trial Measures for Administration," which governs the filing deadlines for initial public offerings or listings overseas. In cases where application documents have not been submitted overseas, filings must be completed within three working days following the first public announcement by the listed company regarding specific transaction arrangements.

Therefore, domestic enterprises that comply with the requirements of Article 15 of the "Administrative Trial Measures" and achieve overseas listing through mergers and acquisitions with SPAC companies via the De-SPAC transaction method must complete the filing process with the China Securities Regulatory Commission (CSRC) .

In accordance with the newly issued regulations on overseas listings. Following the introduction of these new regulations, for domestic enterprises engaging in De-SPAC transactions and subsequent listings, the completion of the CSRC filing and acquisition of the overseas issuance and listing filing notice are generally considered prerequisites for the closing of the merger transaction. Consequently, failure to obtain the filing notice may result in the target company being unable to satisfy the closing conditions, thereby leading to the postponement or suspension of the De-SPAC transaction and/or listing. Furthermore, without obtaining the filing notice, as stipulated in Article 27 of the "Trial Measures for Administration," the lead securities institution may be subject to warnings, fines, or other penalties.

III.Comparative Analysis of SPAC Listing Regulatory Requirements in the United States, Hong Kong, and Singapore

As detailed below:

Nasdaq/NYSE | HKEX | SGX | |

The scale of capital raised by SPAC | The market capitalization must be at least 50 million US dollars, with NGM being no less than 75 million US dollars. Additionally, for the New York Stock Exchange, the market capitalization requirement is a minimum of 100 million US dollars. | No less than one billion Hong Kong dollars, and the fair market value of the acquisition target must be at least 80% of the funds raised by the SPAC in its initial public offering. | The market value should be at least 150 million Singapore dollars, and the market value of the acquisition target must constitute no less than 80% of the escrow funds. |

Qualification of the Sponsor | / | It must adhere to the suitability and qualification requirements, and at least one initiator must hold either Financial Services License No. 6 or Asset Management License No. 9, or both, issued by the Securities and Futures Commission of Hong Kong. | The initiator's track record, coupled with the professional expertise of the management team. |

Investor stakeholder | / | For accredited investors only | / |

Minimum number of public shareholders | 300 | The successor company must have a minimum of 100 shareholders. | At least 25% of the issued shares are held by at least 300 public shareholders. |

The minimum investment share of the initiator | / | At least one sponsor holds a minimum of 10% of the SPAC company's shares. | 2.5%-3.5% of the market capitalization of SPAC. |

PIPE(Independent third party)) | / | The lesser of the following: (a) The percentage of the current stipulated investment amount relative to the agreed valuation of the De-SPAC target, as follows: (i) For a valuation below HKD 2 billion, 25%; (ii) For a valuation of HKD 2 billion or more but less than HKD 5 billion, 15%; (iii) For a valuation of HKD 5 billion or more but less than HKD 7 billion, 10%; or (iv) For a valuation of HKD 7 billion or more, 7.5% (provided that if the valuation exceeds HKD 10 billion, the Hong Kong Stock Exchange may accept a percentage lower than 7.5%); or (b) HKD 500 million. | There are no mandatory requirements for independent PIPE investments. However, if the SPAC merger and acquisition transaction does not include PIPE investment, it is necessary to engage an independent valuation agency. |

Deadline for completing the merger | SPAC companies are required to complete the merger transaction within 24 months following their initial public offering. Should the specified regulatory requirements and conditions be satisfied, this timeframe may be extended by an additional period of up to 12 months. | SPAC companies are required to announce the merger transaction within 24 months following their initial public offering and complete the merger within 36 months. Under certain conditions, this timeline may be extended by an additional six months at most. | SPAC companies are required to complete their merger transactions within 24 months following their initial public offering. Should the relevant regulations and conditions be satisfied, this timeframe may be extended by an additional period of up to 12 months. |

Criteria for Approving SPAC Merger and Acquisition Transactions | The successor company is required to adhere to the regulations of the relevant exchanges concerning initial public offerings (IPOs). | ||

Approval requirements for the shareholders' meeting of SPAC mergers and acquisitions | More than half of the SPAC shareholders are in favor, yet their actions remain subject to the constraints outlined in the articles of association. | More than half of the SPAC shareholders, excluding the sponsors and other stakeholders with significant interests, are in favor of the proposal. | More than half of the SPAC shareholders are in favor, yet their actions remain subject to the constraints outlined in the articles of association. |

Dual equity after De-SPAC | In the IPO stage: Some SPAC companies will issue different types of shares to the promoters and public investors, with varying rights in terms of redemption rights, liquidation rights, etc. De-SPAC stage: Allowed. | / | IPO stage: Not allowed; De-SPAC stage: Allowed. |

Summary

Currently, the Nasdaq continues to serve as the primary exchange for SPAC listings, with a predominant focus on technology and healthcare sectors. Nevertheless, the potential of the Hong Kong Stock Exchange (HKEX) and the Singapore Exchange (SGX) should not be overlooked. In light of the global expansion trends among enterprises, those meeting relevant criteria may comprehensively evaluate their options by considering factors such as strategic development, capital-raising requirements, and transactional efficiency. Regardless of the chosen exchange, strict adherence to regulatory compliance must remain a fundamental principle.