On December 26, 2017, China's National Development and Reform Commission (“NDRC”) issued the “Management Rules for Overseas Investment by Enterprises”, Order No. 11 of 2017 (“Order 11”). On February 11, 2018, the NDRC issued the “Catalog on Overseas Investment in Sensitive Industries (2018 Edition)” (the “Sensitive Industries List”) and the “Set of Forms Related to the Management Rules for Overseas Investment by Enterprises” (the “Standard Forms”).

The NDRC will closely scrutinize overseas investment by Chinese enterprises in industries specified in the Sensitive Industries List. The Standard Forms set forth detailed documentation and information requirements that Chinese enterprises will need to submit to the NDRC when making overseas investments, whether such investments require NDRC approval or only a record-filing with the NDRC. Order 11, the Sensitive Industries List and the Standard Forms will all come into effect on March 1, 2018.

It is important to note that, in addition to the approval or record-filing requirements under Order 11, Chinese investors may also need to comply with other pre-existing PRC regulatory requirements when making overseas investments, such as approval or record-filing with the Ministry of Commerce and approval for the remittance of funds out of China.

Order 11 is novel because it effectively creates long-arm jurisdiction over the overseas investment activities of Chinese investors by imposing new regulations and requirements on overseas arms controlled by such Chinese investors. Accordingly, even if these overseas arms are legally independent of a Chinese parent, or have raised funds or generated revenue outside of China, they are still subject to the requirements of Order 11. Accordingly, when these overseas arms intend to conduct other investments outside of China, they will have to comply with Order 11.

Part I – Sensitive Industries List

Any investment by a Chinese investment in a sensitive industry requires approval under Order 11. This is true even if the investment is made by an overseas arm controlled by a Chinese parent.

The Sensitive Industries List defines the following as sensitive industries:

Research, development, production or repair of weapons and related equipment

Development or use of cross-border water resources

News media

Real estate

Hotels

Cinemas

Entertainment

Sports clubs

Establishment of equity investment funds or investment platforms without a specific industrial project

The Sensitive Industries List includes items that are, to date, not well-defined. For example, “entertainment” is not defined, meaning variants of entertainment such as gaming may fall within the scope of the Sensitive Industries List. For well-defined items such as real estate, the implication for potential sellers and non-Chinese investors is starting to take shape. Starting on March 1, 2018, any overseas investment by a Chinese buyer in a sensitive industry, including a buyer incorporated outside of China that is controlled by Chinese investors, is required to obtain NDRC approval pursuant to Order 11.

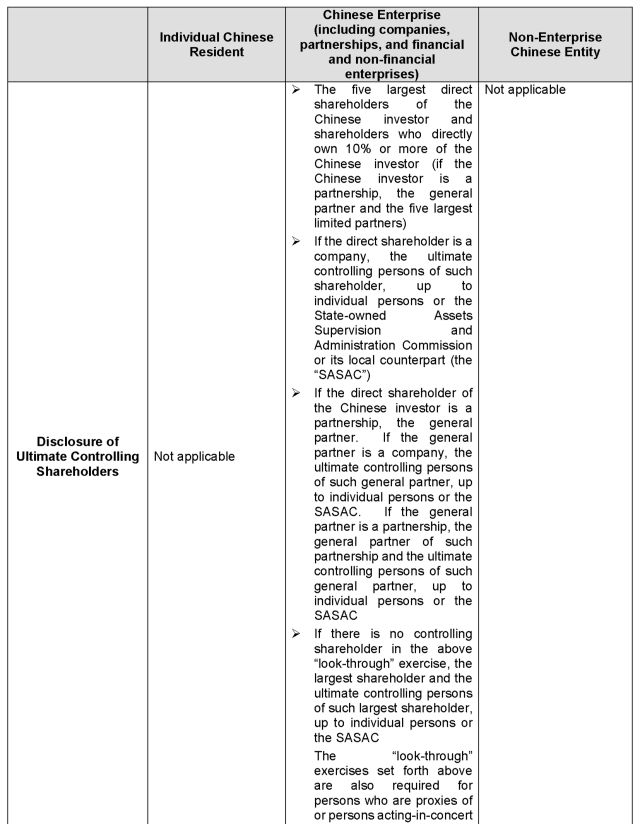

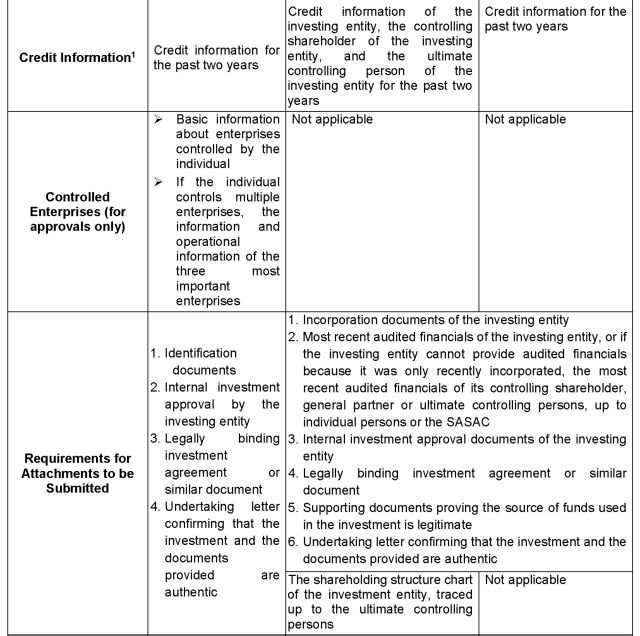

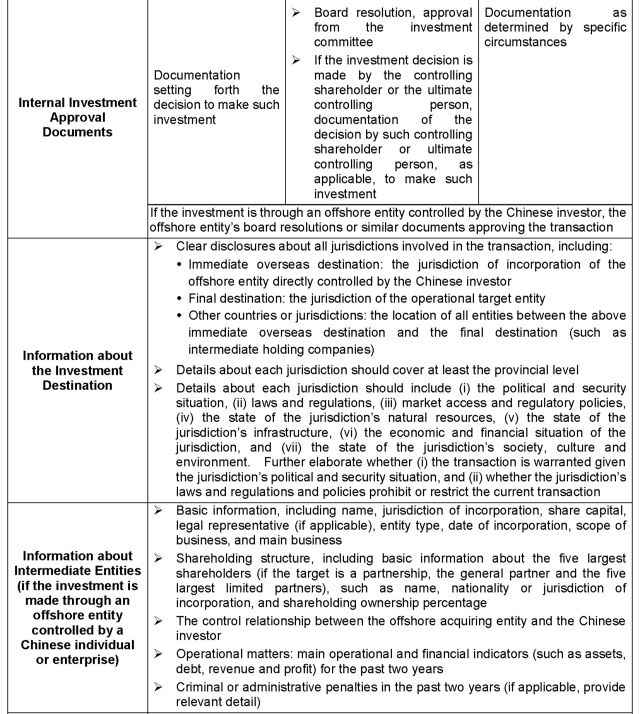

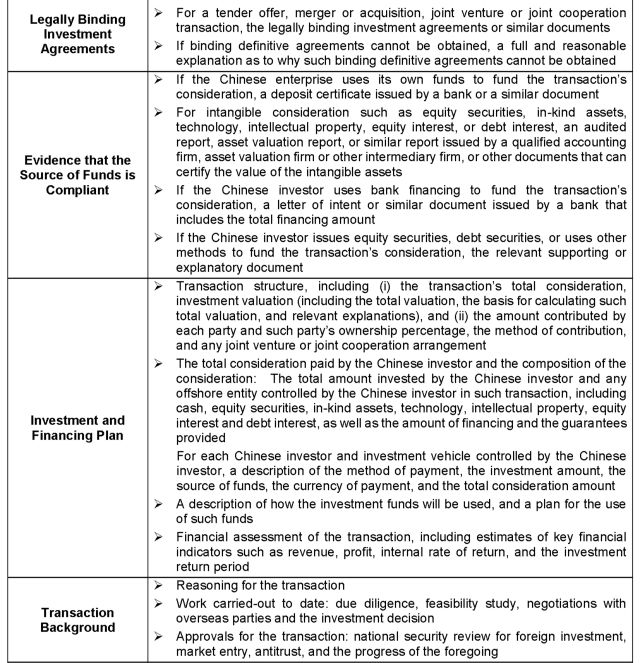

Part II – Comprehensive Disclosure Requirements

The Standard Forms expand and more specifically set forth the application and disclosure requirements under Order 11. What is worth noting is that the application materials for transactions requiring NDRC approval and transactions only requiring a record-filing with the NDRC are both expansive as compared to existing requirements.

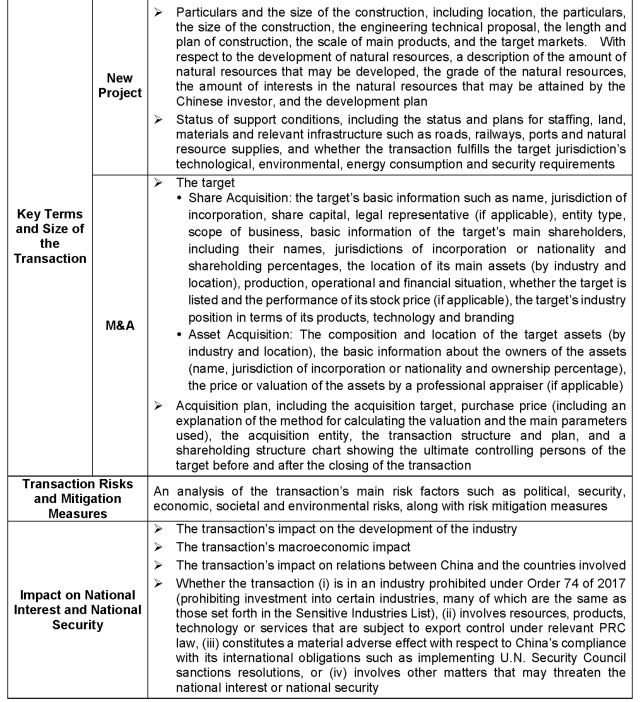

Below is a detailed list of requirements divided into different categories of Chinese resident persons.

Part III – Practical Observations

The Standard Forms' requirement that applicants submit legally binding agreements means the parties may no longer rely on non-binding term sheets, letters of intent or memorandums of understanding when submitting application materials.

The Standard Forms also require the disclosure of indirect control arrangements, such as contractual control (including management contracts) and trusts, along with the entire investment holding structuring, including all intermediate special purpose vehicles. Accordingly, the Standard Forms increase transparency requirements with respect to ultimate beneficial ownership, which may impact Chinese investors who, for one reason or another, do not wish to disclose such arrangements.

Part IV – The Standard Forms’ Requirements are more Comprehensive as Compared to Existing Requirements

Compared with the NDRC’s current application documentation requirements for overseas investment, the Standard Forms' requirements are more comprehensive, resulting in increased disclosure obligations for Chinese investors.

One of the consequences of the new requirement to disclose ultimate beneficial owners is that the NDRC will now be able to access the credit records of the applicants. Accordingly, applicants will no longer be able to avoid this evaluation through the establishment of intermediate holding companies or different investment vehicles.

In addition, the Standard Forms codify a recent practice requiring applicants to demonstrate that they have evaluated the risks of the overseas investment and have taken appropriate countermeasures. This requirement may be in response to recent overseas investment activities by large, heavily indebted Chinese conglomerates in industries now labeled as sensitive.

As the Standard Forms impose more comprehensive application documentation requirements, we predict that Chinese enterprises will need more time to prepare these application materials. The new application requirements, such as the need to submit definitive and binding documentation, may result in increased deal costs and uncertainty. Accordingly, non-Chinese sellers should consult qualified PRC counsel with on-the-ground knowledge of law and, more importantly, its practical implementation, when discussing transactions with potential Chinese buyers.

New Requirements for China Outbound Investments

作者:AaronZhou BingXue CharlesWu来源:汉坤律师事务所

On December 26, 2017, China's National Development and Reform Commission (“NDRC”) issued the “Manage