Summary

Recently, PRC Ministry of Justice released the Notice of the Ministry of Justice on Seeking Public Comments for the Regulations on Foreigners’ Permanent Residence in the People’s Republic of China (Exposure Draft), stipulating the foreigner's permanent residence application requirements, approval procedures and other matters. For foreigners who intend to apply through the way of working in China or reuniting with their families, a good tax record and the actual number of days of residence in China meet the requirements are essential application conditions. From the surface, it seems that for foreigners who wish to apply for permanent residence status through the working in China category and the family reunion category, the longer the period of substantial presence in China, the better. However, foreigners must be aware of another thing, that is the fact that the actual number of days of one’s substantial presence in China will directly affect whether one needs to pay individual income tax on income derived outside the territory of China. Therefore, how to balance the control of IIT costs and long-term residence in China is a problem that we can help foreigners who have with no residence domicile in China (hereinafter referred to as "foreigners") to solve.

Background

Since the implementation of the Measures for the Administration of Examination and Approval of Foreigners' Permanent Residence in China in 2004 (hereinafter referred to as the Administrative Measures), the Chinese Green Card has always been known for its difficulty to apply. But on February 27, 2020, the Ministry of Justice promulgated the Notice of the Ministry of Justice on Seeking Public Comments for the Regulations on Foreigners’ Permanent Residence in the People’s Republic of China (Exposure Draft) (hereinafter referred to as the Exposure Draft). The Exposure Draft stipulates the foreigner's permanent residence application requirements, approval procedures and other matters. Compared with the previous permanent residence policy, it has made some great developments, and has become the new weathervane of the Chinese Green Card.

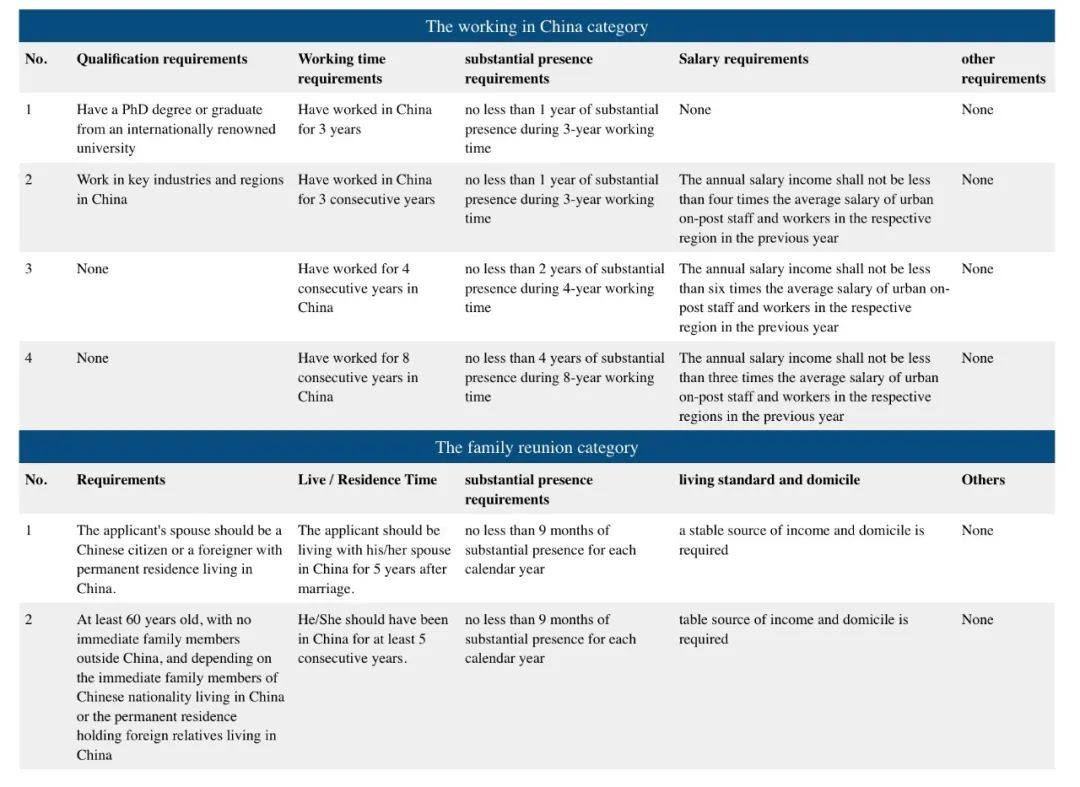

The foreigners listed in the Exposure Draft who can apply for permanent residence can be summarized into the following categories: outstanding contribution category, outstanding achievement category, urgently needed talent category, working in China category, foreign investment category, family reunion category, among which, both the working in China category and the family reunion category have substantial presence requirements in China, and the working in China category also needs proof of good tax records and credit history.

So, for foreigners who wish to apply for permanent residence through the working in China category and the family reunion category, it seems that the longer the substantial presence in China, the better. However, foreigners must be aware of the fact that the actual number of days of one’s substantial presence in China will directly affect whether one needs to pay individual income tax ( hereinafter referred to as the "IIT") on income derived outside the territory of China.

Therefore, how to balance the control of IIT costs and long-term residence in China is a problem that foreigners with no domicile in China (hereinafter referred to as "foreigners") must consider.

I Under what circumstances are the foreigners not required to pay IIT on income derived outside the territory of China

A. Under the premise of compliance filing, the foreigners can enjoy tax-free benefits on income derived outside the territory of China and paid by overseas units or individuals before 2024 (inclusive).

Subject to record-filing with the competent tax authority, IIT exemption should be given to the income derived outside the territory of China and paid by any overseas entity or individual shall the applicant’s substantial presence in China is less than 183 days each year and for 6 consecutive years.

Here is the Q & A about this issue:

1. Q: What qualifies as “substantial presence in China for more than 183 days a year”?

A: The total number of days of residence of a foreigner in China within a tax year shall be calculated according to his/her total number of days of staying inside china territory. If the day of staying equals to or exceeds 24 hours, then the day is considered a valid substantial presence day, and shall be included in the total number of days, otherwise, the day will be considered invalid, and not be included.

2. Q: What qualifies as “ six consecutive years”?

A: If a foreigner has resided in China for 183 days in a tax year, he / she shall have resided for six consecutive years from the previous year to the previous six years in each tax year for 183 days in total. The starting year of the previous six years starts from 2019 (inclusive).

3. Q: If the accumulated residence for each year is 183 days, is there any way to interrupt the recalculation after 6 consecutive years?

A: If the foreigners have left China for more than 30 days on a single trip in any of the previous six years, their income derived outside China and paid by an overseas employer or individual shall be exempted from individual income tax. As a result, this year should be the starting point of a new 6-consecutive years with each year’s substantial presence should be no less than 183 days.

4.Q: What qualifies as a day in “183 days” requirement?

A: If the day of staying equals to or exceeds 24 hours, then the day is considered a valid substantial presence day, and shall be included in the total number of days, otherwise, the day will be considered invalid, and not be included.

B. For Instance

Ms. Chen is a Macao resident employed by a Macao entity but always needs to travel to work in Zhuhai. She goes to work in Zhuhai from Macao on Monday, and will travel back to Macao on Friday of the same week.

As stated above, the individual stays in China for 24 hours in a day, the said day shall be included in the number of days of residence in China; if less than 24 hours, the said day shall not be included. So, Ms. Chen is considered to have resided in the PRC for 3 days in a week since Monday and Friday, on which Ms. Chen only spends part of each day in the PRC, will not be counted as two days for PRC IIT purposes.

If Ms. Chen continues this working mode during the entire year, she will only be regarded as resident in the PRC for 156 days (3 days x 52) during a tax year and thus will not be treated as a PRC tax resident for PRC IIT purposes. If Mrs. Chen's salary is paid and borne by her Macao employer, she will not be subject to RPC IIT.

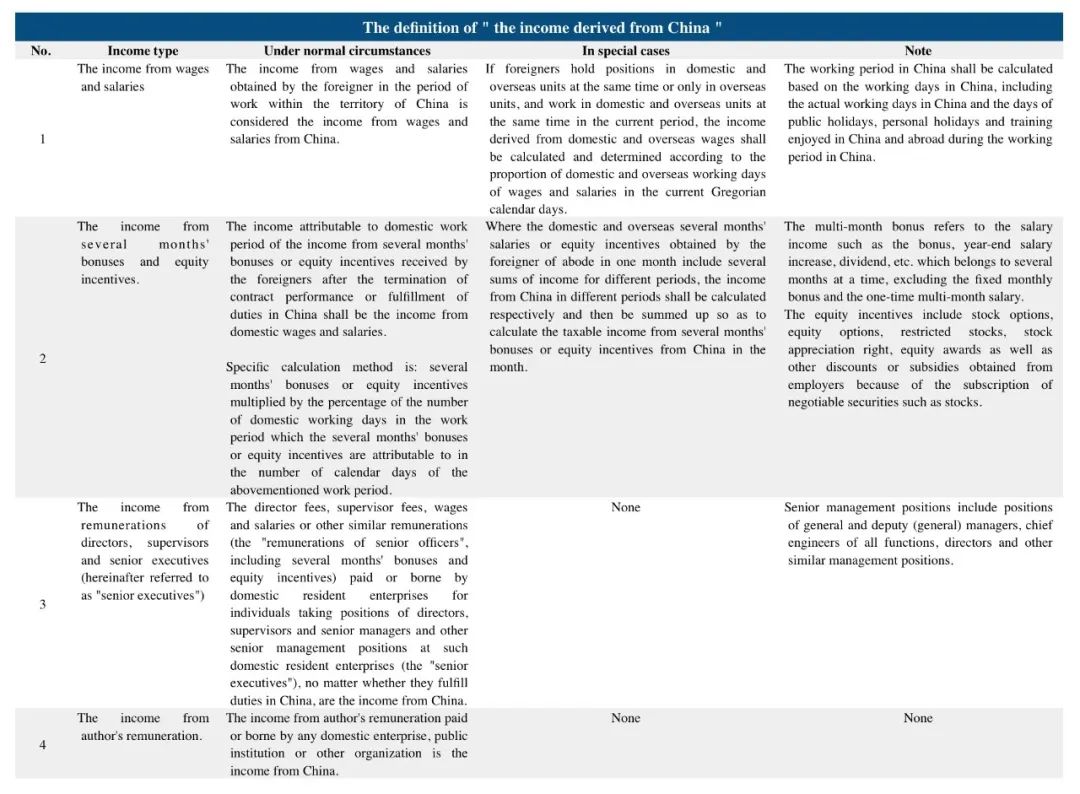

II How to define your income is derived outside the territory of China

As mentioned above, if a foreigner plans his/her work schedule successfully then only the income derived from China shall be subject to IIT. We can use the chart below to determine what income is defined as “the income derived from China”:

Ⅲ How should the foreigners calculate IIT paid in China

Since the calculation of the IIT payable is based on the amount of income, therefore, we divide the calculation of the IIT payable of the foreigners into the following two steps:

A. Calculation of IIT on wages and salaries

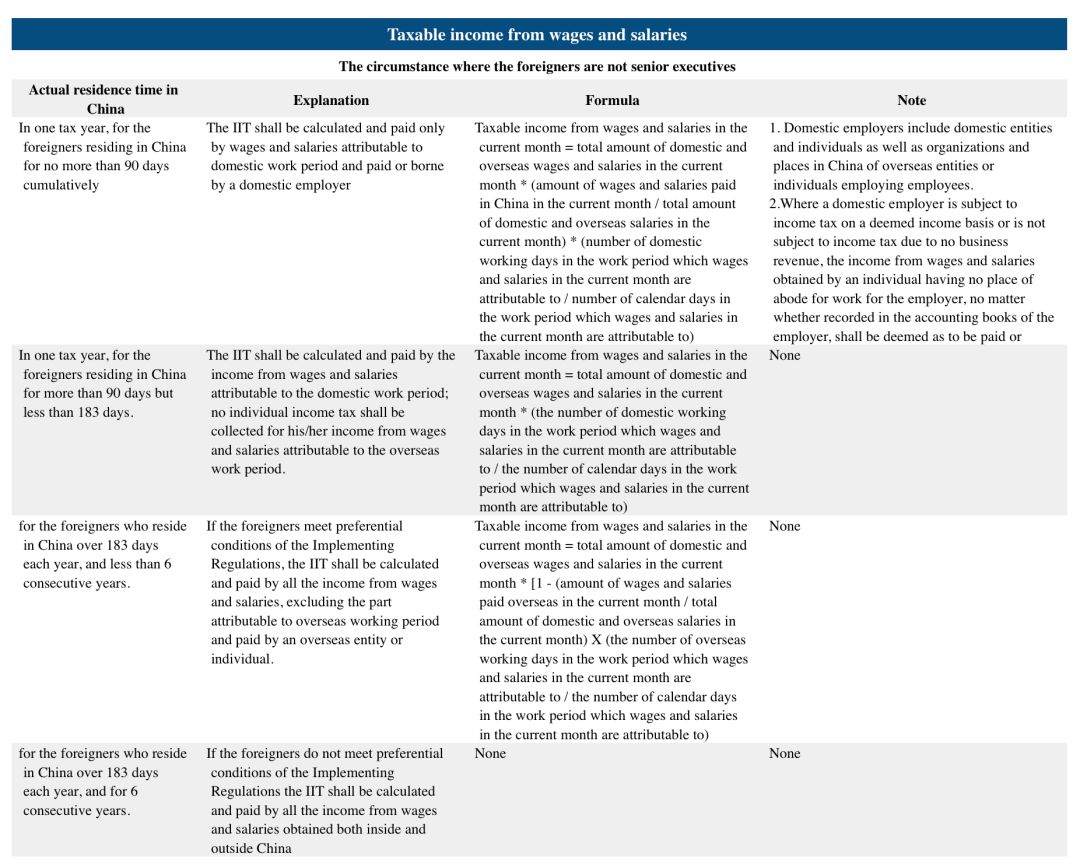

1. Calculation of the Taxable Income from Wages and Salaries

For foreigners, the most important part of their income comes from wages and salaries. When calculating the income of wages and salaries, we should strictly distinguish them according to the actual residence time of foreigners in China:

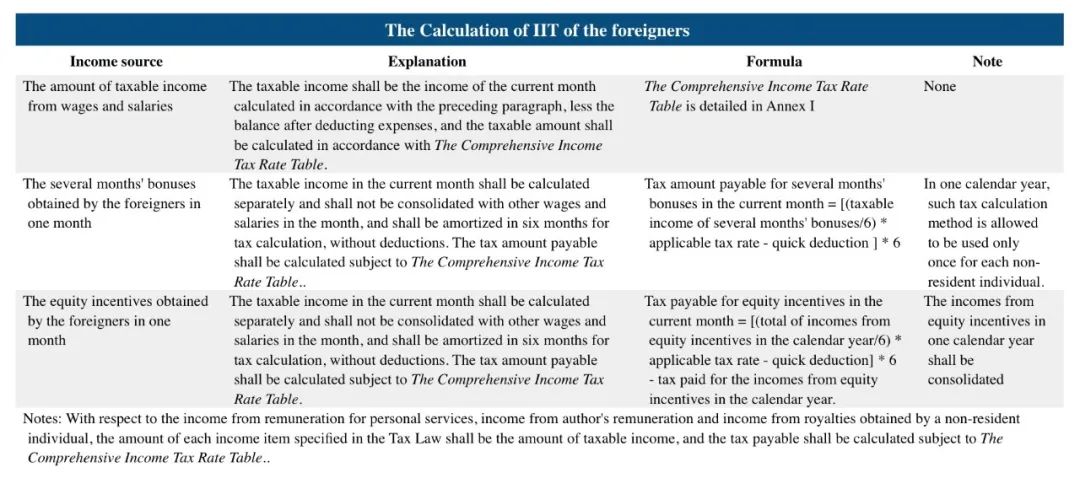

2. The Calculation of IIT of the foreigners

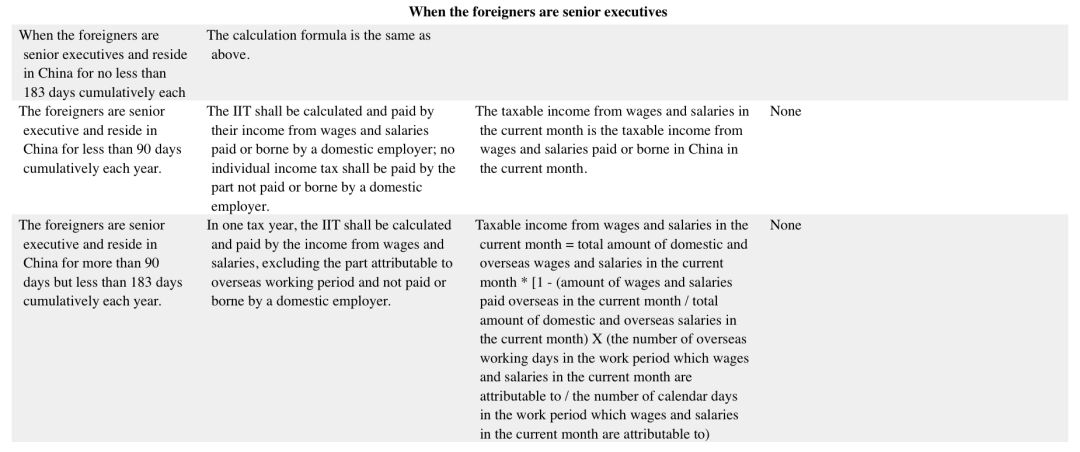

(1) When the foreigners reside in China for no less than 183 days cumulatively each year.

Tax payable for annual consolidated income = (annual taxable income from wages and salaries + annual taxable income from remuneration for personal services + annual taxable income from author's remuneration + annual taxable income from royalties - deductions - special deductions - special additional deductions - other deductions determined according to the law) * applicable tax rate - quick deduction

(2) When the foreigners reside in China for less than 183 days cumulatively each year.

Ⅳ The recommendations of the compliance and cost control of IIT for foreigners working in China

As mentioned above, foreigners working in China should reasonably arrange their work schedules or residence plans with a full understanding of Chinese IIT rules. On the premise of fully complying with the rules, foreigners can consider the following aspects of planning arrangements to lower tax costs:

1. Avoiding tax resident status by arranging a reasonable tax holiday;

2. Avoiding overpayment of taxes through reasonable arrangements of paying distribution

3. Trying to create conditions in line with the preferential IIT policies in China (For example, tax preferential policies for individuals from Hong Kong and Macao in Greater Bay Area)

4. Fully understand and make use of the Double Taxation Avoidance agreements signed between the host country where foreigners are tax residents and China, and the Double Taxation Avoidance arrangements signed between the mainland and Hong Kong and Macao, so as to avoid double taxation and overpayment of taxes.

If foreigners working in China and their employers have any questions about the above content, please feel free to contact us for more details.

Annex

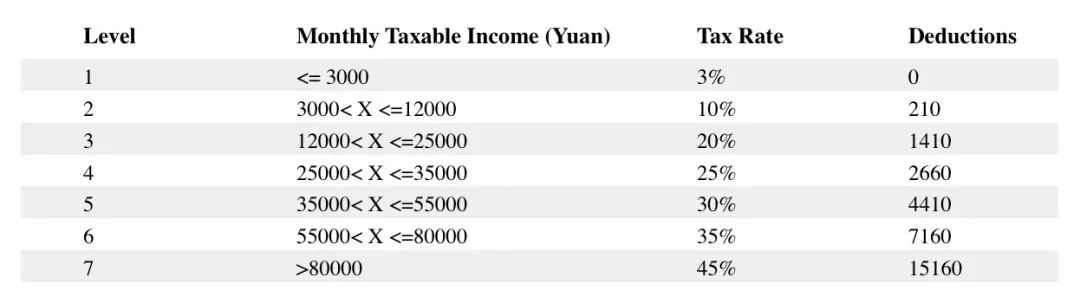

The Comprehensive Income Tax Rate Table (converted by month)

Recently, PRC Ministry of Justice released the Notice of the Ministry of Justice on Seeking Public Comments for the Regulations on Foreigners’ Permanent Residence in the People’s Republic of China (Exposure Draft), stipulating the foreigner's permanent residence application requirements, approval procedures and other matters. For foreigners who intend to apply through the way of working in China or reuniting with their families, a good tax record and the actual number of days of residence in China meet the requirements are essential application conditions. From the surface, it seems that for foreigners who wish to apply for permanent residence status through the working in China category and the family reunion category, the longer the period of substantial presence in China, the better. However, foreigners must be aware of another thing, that is the fact that the actual number of days of one’s substantial presence in China will directly affect whether one needs to pay individual income tax on income derived outside the territory of China. Therefore, how to balance the control of IIT costs and long-term residence in China is a problem that we can help foreigners who have with no residence domicile in China (hereinafter referred to as "foreigners") to solve.

Background

Since the implementation of the Measures for the Administration of Examination and Approval of Foreigners' Permanent Residence in China in 2004 (hereinafter referred to as the Administrative Measures), the Chinese Green Card has always been known for its difficulty to apply. But on February 27, 2020, the Ministry of Justice promulgated the Notice of the Ministry of Justice on Seeking Public Comments for the Regulations on Foreigners’ Permanent Residence in the People’s Republic of China (Exposure Draft) (hereinafter referred to as the Exposure Draft). The Exposure Draft stipulates the foreigner's permanent residence application requirements, approval procedures and other matters. Compared with the previous permanent residence policy, it has made some great developments, and has become the new weathervane of the Chinese Green Card.

The foreigners listed in the Exposure Draft who can apply for permanent residence can be summarized into the following categories: outstanding contribution category, outstanding achievement category, urgently needed talent category, working in China category, foreign investment category, family reunion category, among which, both the working in China category and the family reunion category have substantial presence requirements in China, and the working in China category also needs proof of good tax records and credit history.

So, for foreigners who wish to apply for permanent residence through the working in China category and the family reunion category, it seems that the longer the substantial presence in China, the better. However, foreigners must be aware of the fact that the actual number of days of one’s substantial presence in China will directly affect whether one needs to pay individual income tax ( hereinafter referred to as the "IIT") on income derived outside the territory of China.

Therefore, how to balance the control of IIT costs and long-term residence in China is a problem that foreigners with no domicile in China (hereinafter referred to as "foreigners") must consider.

I Under what circumstances are the foreigners not required to pay IIT on income derived outside the territory of China

A. Under the premise of compliance filing, the foreigners can enjoy tax-free benefits on income derived outside the territory of China and paid by overseas units or individuals before 2024 (inclusive).

Subject to record-filing with the competent tax authority, IIT exemption should be given to the income derived outside the territory of China and paid by any overseas entity or individual shall the applicant’s substantial presence in China is less than 183 days each year and for 6 consecutive years.

Here is the Q & A about this issue:

1. Q: What qualifies as “substantial presence in China for more than 183 days a year”?

A: The total number of days of residence of a foreigner in China within a tax year shall be calculated according to his/her total number of days of staying inside china territory. If the day of staying equals to or exceeds 24 hours, then the day is considered a valid substantial presence day, and shall be included in the total number of days, otherwise, the day will be considered invalid, and not be included.

2. Q: What qualifies as “ six consecutive years”?

A: If a foreigner has resided in China for 183 days in a tax year, he / she shall have resided for six consecutive years from the previous year to the previous six years in each tax year for 183 days in total. The starting year of the previous six years starts from 2019 (inclusive).

3. Q: If the accumulated residence for each year is 183 days, is there any way to interrupt the recalculation after 6 consecutive years?

A: If the foreigners have left China for more than 30 days on a single trip in any of the previous six years, their income derived outside China and paid by an overseas employer or individual shall be exempted from individual income tax. As a result, this year should be the starting point of a new 6-consecutive years with each year’s substantial presence should be no less than 183 days.

4.Q: What qualifies as a day in “183 days” requirement?

A: If the day of staying equals to or exceeds 24 hours, then the day is considered a valid substantial presence day, and shall be included in the total number of days, otherwise, the day will be considered invalid, and not be included.

B. For Instance

Ms. Chen is a Macao resident employed by a Macao entity but always needs to travel to work in Zhuhai. She goes to work in Zhuhai from Macao on Monday, and will travel back to Macao on Friday of the same week.

As stated above, the individual stays in China for 24 hours in a day, the said day shall be included in the number of days of residence in China; if less than 24 hours, the said day shall not be included. So, Ms. Chen is considered to have resided in the PRC for 3 days in a week since Monday and Friday, on which Ms. Chen only spends part of each day in the PRC, will not be counted as two days for PRC IIT purposes.

If Ms. Chen continues this working mode during the entire year, she will only be regarded as resident in the PRC for 156 days (3 days x 52) during a tax year and thus will not be treated as a PRC tax resident for PRC IIT purposes. If Mrs. Chen's salary is paid and borne by her Macao employer, she will not be subject to RPC IIT.

II How to define your income is derived outside the territory of China

As mentioned above, if a foreigner plans his/her work schedule successfully then only the income derived from China shall be subject to IIT. We can use the chart below to determine what income is defined as “the income derived from China”:

Ⅲ How should the foreigners calculate IIT paid in China

Since the calculation of the IIT payable is based on the amount of income, therefore, we divide the calculation of the IIT payable of the foreigners into the following two steps:

A. Calculation of IIT on wages and salaries

1. Calculation of the Taxable Income from Wages and Salaries

For foreigners, the most important part of their income comes from wages and salaries. When calculating the income of wages and salaries, we should strictly distinguish them according to the actual residence time of foreigners in China:

2. The Calculation of IIT of the foreigners

(1) When the foreigners reside in China for no less than 183 days cumulatively each year.

Tax payable for annual consolidated income = (annual taxable income from wages and salaries + annual taxable income from remuneration for personal services + annual taxable income from author's remuneration + annual taxable income from royalties - deductions - special deductions - special additional deductions - other deductions determined according to the law) * applicable tax rate - quick deduction

(2) When the foreigners reside in China for less than 183 days cumulatively each year.

Ⅳ The recommendations of the compliance and cost control of IIT for foreigners working in China

As mentioned above, foreigners working in China should reasonably arrange their work schedules or residence plans with a full understanding of Chinese IIT rules. On the premise of fully complying with the rules, foreigners can consider the following aspects of planning arrangements to lower tax costs:

1. Avoiding tax resident status by arranging a reasonable tax holiday;

2. Avoiding overpayment of taxes through reasonable arrangements of paying distribution

3. Trying to create conditions in line with the preferential IIT policies in China (For example, tax preferential policies for individuals from Hong Kong and Macao in Greater Bay Area)

4. Fully understand and make use of the Double Taxation Avoidance agreements signed between the host country where foreigners are tax residents and China, and the Double Taxation Avoidance arrangements signed between the mainland and Hong Kong and Macao, so as to avoid double taxation and overpayment of taxes.

If foreigners working in China and their employers have any questions about the above content, please feel free to contact us for more details.

Annex

The Comprehensive Income Tax Rate Table (converted by month)