Cuddle up to Panda Bonds——Brief Analysis of the Application and Issuance of Panda Bonds from a PRC Law Perspective

熊猫债券方兴未艾——从中国法律角度简析熊猫债券的申请和发行

On September 8, 2018, the People’s Bank of China (the “PBOC”) and the Ministry of Finance jointly promulgated the Interim Measures of the Administration of Offshore Institutions’ Bond Offering in National Interbank Bond Market (the “Interbank Panda Bond1 Measures”). The Interbank Panda Bond Measures and the Notice on Launching the Pilot Program of the Belt and Road Bonds (the “Notice on Stock Exchange Panda Bonds”) promulgated by the Shanghai Stock Exchange and Shenzhen Stock Exchange (collectively, the “Stock Exchanges”) in March 2018 constitute the main legal sources for offshore institutions’ Panda Bond offerings on the interbank bond market and stock exchange bond market respectively. These two regulations together with the interbank bond market rules promulgated by the PBOC, the National Association of Financial Market Institutional Investors (“NAFMII”) and other stock exchange bond market rules promulgated by the China Securities Regulatory Commission (the “CSRC”) and stock exchanges form the preliminary legal framework for Panda Bonds. We understand that NAFMII is drafting the guidelines for the registration and issuance of bonds by foreign governmental agencies, international development agencies and non-financial corporations on the national interbank bond market. With the release of such guidelines, the legal supervision system of Panda Bonds will be more complete.

2018年9月8日,中国人民银行和财政部联合颁布了《全国银行间债券市场境外机构债券发行管理暂行办法》(以下简称“《银行间熊猫债券办法》”),该办法与上海证券交易所和深圳证券交易所(以下合称“交易所”)于2018年3月分别颁布的《关于开展“一带一路”债券业务试点的通知》(以下简称“《交易所熊猫债券通知》”),分别构成了境外机构在银行间债券市场和交易所债券市场申请发行熊猫债券的统领性法律文件;连同中国人民银行和中国银行间市场交易商协会(以下简称“交易商协会”)已发布的银行间债券市场规则,以及中国证券监督管理委员会(以下简称“中国证监会”)和交易所已发布的交易所债券市场规则,初步形成了熊猫债券的法律监管体系。我们理解,交易商协会正在制定外国政府类机构、国际开发机构、非金融企业法人等在全国银行间债券市场注册发行债券的业务指引,该等指引出台后,熊猫债券的监管体系将更加完善。

Based on the latest legislation, and our previous experience on relevant projects, we have summarized the key procedures and issues when applying for Panda Bonds issuance in this article.

本文依据熊猫债券发行的最新法规动态,并结合本所以往项目经验,从中国法律角度简要梳理了不同主体申请发行熊猫债券的基本流程以及需要关注的主要问题,以抛砖引玉,供相关熊猫债券市场参与者参考和讨论。

I.General Procedures for Issuing Panda Bonds on the Interbank Bond Market

银行间债券市场熊猫债券基本流程

Please find below the governing authority, registration/approval procedures and qualifications for different types of issuers to issue Panda Bonds on interbank bond market.

依据发行主体的不同,我们梳理了如下银行间债券市场熊猫债发行项目的主管及审批程序。

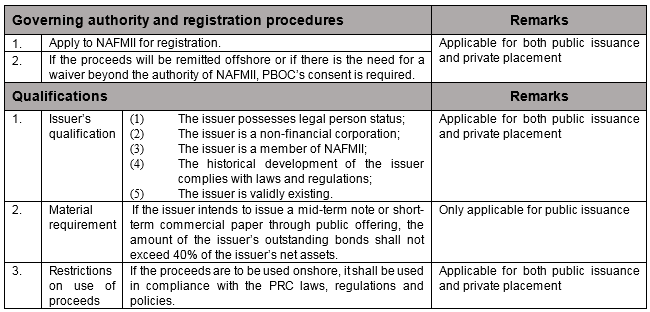

1. Non-financial corporate issuers

发行人为非金融企业

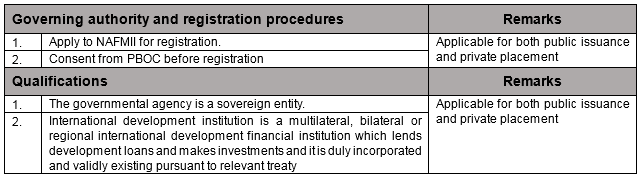

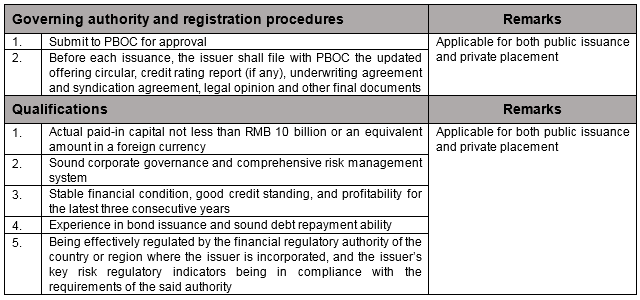

2. Foreign governmental agency and international development institution issuers

发行人为外国政府类机构、国际开发机构

3. Financial Institution issuers

发行人为金融机构

II.General Procedures for Panda Bonds Issuance in the Stock Exchange Bond Market

交易所债券市场熊猫债券基本流程

Pursuant to the Notice on Stock Exchange Panda Bonds, national or regional governmental agencies, non-financial corporations and financial institutions within the “Belt and Road” region can apply to the Stock Exchange for the issuance of “Belt and Road” Panda Bonds. Currently, all Panda Bonds issuers in the stock exchange bond market are non-financial corporations; to date, no financial institution, governmental agency or international development institution has issued Panda Bonds on the stock exchange bond market. We understand that the following list applies to both non-financial corporations and to financial institutions.

根据《交易所熊猫债券通知》,“一带一路”沿线国家(地区)政府机构、一般企业和金融机构均可向交易所申请发行“一带一路”熊猫债券。目前,交易所市场仅有非金融企业发行的先例,无金融机构和外国主权类机构、国际开发机构发行的先例。与银行间债券市场不同,交易所债券市场熊猫债券并未依据发行主体的不同区分主管部门及审批程序,仅因发行方式的不同有所区别:

III.Key Issues for Panda Bond Issuance Applications

申请发行熊猫债券需要关注的主要问题

1. Accounting principles and auditing

会计准则和审计问题

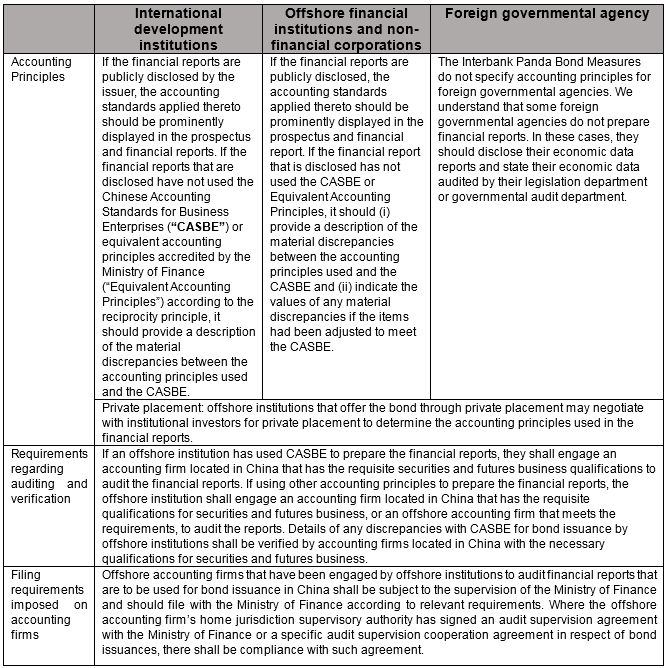

The requirements regarding the accounting principles and auditing applicable to international development institutions, foreign governmental agencies, offshore financial institutions and non-financial corporates, and the filing requirements for offshore accounting firms as specified in the Interbank Panda Bond Measures are as follows:

《银行间熊猫债券办法》对国际开发机构、境外金融机构法人和非金融企业法人适用的会计准则、审计及会计师事务所报备要求如下:

Differences in the accounting principles adopted by Panda Bond issuers and CASBE have been a long-running obstacle deterring many potential Panda Bond issuers. Prior to the promulgation of Interbank Panda Bond Measures, the only accounting principles that had been accredited by the Ministry of Finance as being equivalent to CASBE were the International Financial Reporting Standards adopted by EU listed companies for their consolidated financial reports, and the Hong Kong Accounting Standards for Business Enterprises. Since there are only a limited number of Panda Bond issuers using these equivalent account principles, many potential Panda Bond issuers put their issuance plans on hold. The Interbank Panda Bond Measures allow issuers using non-equivalent accounting principles to apply for public issuance if they provide relevant supplementary information; issuers who find it difficult to provide such supplementary information may choose private placement as an alternative.

一直以来,熊猫债券发行人适用的会计准则与中国企业会计准则的差异处理是诸多熊猫债券发行中的难题。《银行间熊猫债券办法》出台前,经财政部认定已与中国企业会计准则实行等效的会计准则仅包括欧盟成员国上市公司在合并财务报表层面所采用的国际财务报告准则以及香港企业会计准则,而适用上述等效会计准则的熊猫债券发行人数量有限,导致许多有意向发行熊猫债券的发行人的发行计划因此搁置。《银行间熊猫债券办法》出台后,明确了使用非等效会计准则的发行人在公开发行时补充相关信息后可申请发行,同时如发行人认为补充信息有困难的,也可以选择定向发行的方式。

2. Panda Bond Tax Issues

发行和投资熊猫债券的税务问题

(1) Income tax

所得税

Only when the issuer and the investor are both non-PRC resident enterprises can bond interest be exempted from PRC enterprise income tax. For any income earned through the transfer of bonds, if the investor is a PRC resident enterprise, such investor is required to pay Chinese enterprise income tax. It should be noted that if the offshore investor is registered outside of China but has de facto management bodies in China, such investor will still be treated as a PRC resident enterprise and will thus be subject to Chinese enterprise income tax.

对于债息所得,只有发行人和投资者均为中国非居民企业的情况下,才免于中国企业所得税纳税义务;对于转让价差所得,在投资者为中国居民企业的情况下将产生中国企业所得税纳税义务。值得注意的是,境外投资者虽然注册在境外,但如果其实际管理机构位于境内,其仍然构成中国企业所得税法下的中国居民企业,从而产生中国企业所得税纳税义务。

(2) Value-added tax

增值税

Under PRC value-added tax law, an offshore investor’s transfer of Panda Bonds constitutes a financial product transfer service. If the transferee is located outside of China, the offshore investor’s income earned from such transfer is not subject to PRC value-added tax. If the transferee is located within China, the offshore investor’s income earned from such transfer is subject to PRC value-added tax. Certain offshore investors accredited by the PBOC may be exempt from such value-added tax.

境外投资者转让熊猫债券属于提供中国增值税法规规定的金融商品转让服务,如果熊猫债券的受让方在中国境外,境外投资者的转让收入依法不需要缴纳中国增值税;如果熊猫债券的受让方在中国境内,境外投资者的转让收入依法应当缴纳中国增值税,但是境外投资者属于经中国人民银行认可的境外机构,可以免于缴纳增值税。

For further details on Panda Bond-related tax matters, please refer to a previous JunHe Bulletin: Tax Analysis of Offshore Investors’ Investment in Panda Bonds.

关于熊猫债券涉税问题的详细分析,可参考本所此前的研究简讯《境外投资者投资“熊猫债”涉税问题简析》。

When issuing bonds, Panda Bond issuers should also consider the tax laws and regulations of their home country or jurisdiction.

另外,熊猫债券发行人应同时考虑所在国家或地区对债券发行及债券投资的税务征收法律法规。

3. Governing Law and Dispute Resolution

适用法律和争议解决相关问题

The Interbank Panda Bond Measures do not explicitly detail the applicable laws or dispute resolution mechanisms for Panda Bonds. Panda Bond issuers unfamiliar with PRC laws but with extensive experience offering bonds on international capital markets may assume that they can apply non-PRC regulations as the applicable laws and arbitration option should a dispute arise in the course of Panda Bond issuance.

《银行间熊猫债券办法》未明确规定熊猫债券发行及交易文件的适用法律及争议解决机制。部分熊猫债券发行人由于对中国法律不甚了解,且在境外资本市场有丰富的债券发行经验,希望熊猫债券发行及交易文件适用其惯用选择的外国法并在国外进行仲裁。

However, based on the current practice, even though the Interbank Panda Bond Measures do not explicitly detail the applicable laws or dispute resolution mechanisms, the competent authorities still require the transaction documents of Panda Bond issuance to be governed by PRC law and for the resolution of any dispute, including the litigation and arbitration, to be resolved in China.

但是,从目前实践来看,虽《银行间熊猫债券办法》对适用法律和争议解决未作出明确规定,主管机关仍要求熊猫债券发行及交易文件适用中国法律并选择在中国进行争议解决(包括诉讼和仲裁)。

4. Guarantee Structure

担保结构发行相关问题

In order to differentiate the group’s business activities from their financing activities, for the purposes of financing, some corporate groups may establish a special-purpose vehicle (“SPV”) on international markets. The SPV acts as the issuer, the parent company provides a joint liability guarantee for its bond issuance and the proceeds are for the group’s business operations. These issuers may wish to adopt the same guarantee structure when issue Panda Bonds in China.

在国际资本市场,部分集团公司会选择设立特殊目的子公司用于集中融资,将业务活动和融资活动相分离。在此结构下,特殊目的子公司作为发行人发行债券,由集团母公司提供连带责任担保,募集资金用于集团公司业务经营。该等集团公司在中国境内发行熊猫债券,通常也希望采取同样的担保结构发行。

While the Interbank Panda Bond Measures do not specify the option for the above-mentioned guarantee structure, we understand that under certain circumstances, such guarantee structure could possibly be adopted for a bond issue. Since in this structure, the issuer is solely reliant upon the guarantor’s credit to issue bonds, any requirements showing the issuer’s qualifications, their application documents and information disclosure will be equally applicable to the guarantor.

虽然《银行间熊猫债券办法》未明确规定担保结构,但我们理解在一定条件下可以采用上述担保结构发行,由于在此等结构下发行人主要依赖担保人的信用发债,对发行人的资格条件、申请文件和信息披露等要求,担保人应同样适用。

In addition, the proceeds raised by non-financial institutions should not be used as loans to other entities. Under the guarantee structure, proceeds are not normally used by the issuer itself or by its consolidated subsidiaries. Instead, the proceeds are used by the guarantor (generally the parent of the issuer) or the guarantor’s consolidated subsidiaries (i.e. the sister companies of the issuer). There is a need for further clarification from the governing authorities as to what will be the requirements for proceeds loaned to the parent or sister companies.

另外,非金融企业发行债券的募集资金不能用于借贷,在上述担保结构下,募集资金一般并非用于发行人自身或其合并报表范围内子公司,而是用于担保人(一般为发行人的母公司)或其子公司,满足何种标准才能允许该等募集资金使用路径,仍有待与主管机关沟通并进一步澄清。

5. Issuers of Panda Bonds on the Stock Exchanges

交易所熊猫债券的发行主体问题

Pursuant to the Notice on Stock Exchange Panda Bonds, foreign governmental agencies, non-financial corporations and financial institutions may apply to the Stock Exchanges to issue Panda Bonds. Currently, all issuers of Panda Bonds on the Stock Exchanges are offshore non-financial corporations. To date, no offshore financial institution has offered Panda Bonds on the Stock Exchanges, and there are no prevailing laws and regulations to prevent them from doing so. However, in practice, since financial institutions mainly issue bonds on the interbank bond market and the use of proceeds requires pre-approval from the PBOC, if an offshore financial institution plans to issue Panda Bonds on the Stock Exchanges, it should discuss in advance the feasibility of an issuance with the PBOC, the CSRC and the Stock Exchanges.

按照《交易所熊猫债券通知》,政府机构、一般企业和金融机构均可向交易所申请发行熊猫债券,但目前交易所市场发行熊猫债券的主体均为境外非金融机构,尚未有境外金融机构于交易所市场发行熊猫债券的先例。现行法律法规并未禁止境外金融机构于交易所市场发行熊猫债券,但实践中因金融机构主要于银行间债券市场发行债券,且募集资金使用将涉及中国人民银行事先同意等原因,境外金融机构如计划于交易所市场发行熊猫债券,应当提前与中国人民银行、中国证监会及交易所事先沟通发行方案的可行性。

6. Division of Legal Work on Panda Bond Projects

熊猫债券项目律师分工问题

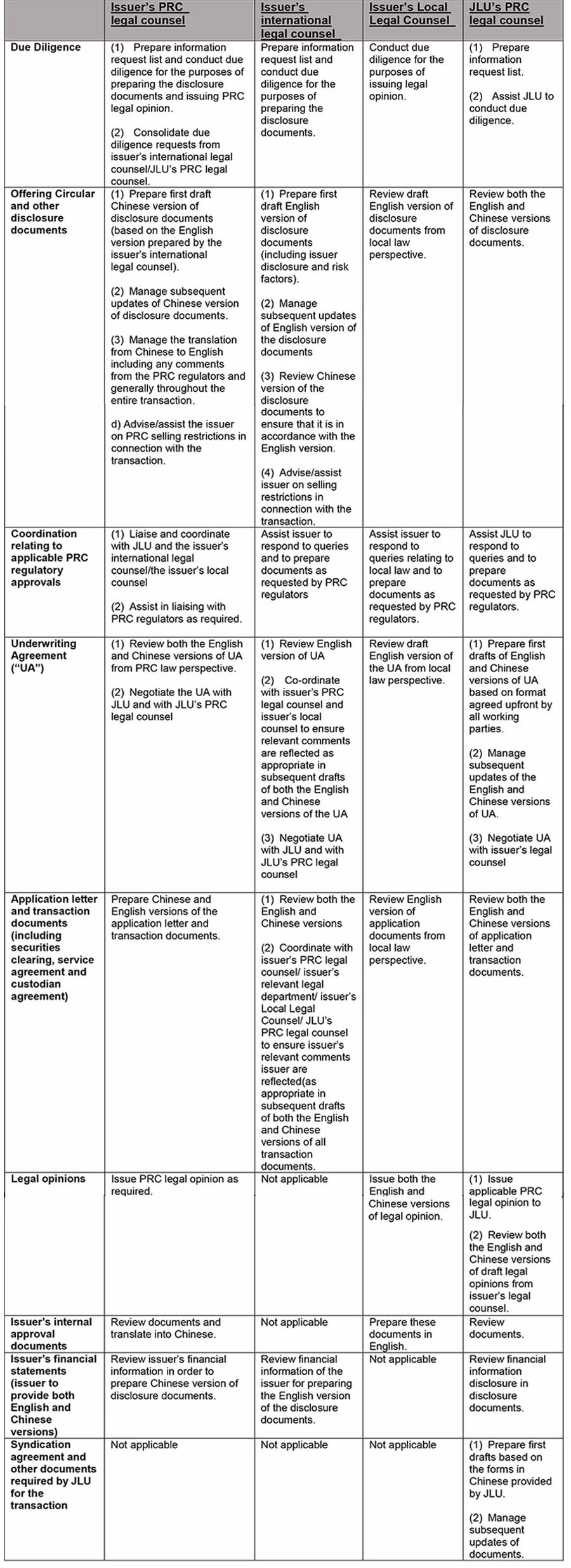

Given that all issuers of Panda Bonds are registered offshore, there will likely be multiple law firms providing legal advice to the issuer. In those cases where the issuer’s place of registration and the place of listing are in different jurisdictions, there could be up to five or more law firms involved, including the issuer’s PRC legal counsel, their international legal counsel, the legal counsel from the issuer’s jurisdiction of incorporation (or internal legal counsel) (the “Local Legal Counsel”), the legal counsel in their place of listing and the underwriter’s PRC legal counsel. In order to manage the legal activities on Panda Bond issues, there would generally be two law firms involved, i.e., the issuer’s PRC legal counsel and their Local legal counsel. Please refer to Appendix I of this article for more details on the responsibilities and division of work among the relevant law firms.

熊猫债券项目因发行人注册在境外,往往会涉及多家律师事务所共同为发行人提供法律服务的情况。在发行人注册地与上市地在不同法域的情况下,可能多达五家律师所,比如发行人境内律师、发行人国际律师、发行人注册地律师(或内部法律顾问)、发行人上市地律师和承销商境内律师,但一般是二家律师所参与,即发行人境内律师和发行人当地律师。各律师所的职责和分工请见本文的附件一。

Appendix I

List of Division of Work amongst Legal Counsels for Panda Bond Issuances

附件一:熊猫债券发行项目中各方律师分工

Under the assumption that the issuer would need both English and Chinese versions of the transaction documents, we have summarized the list of tasks and responsibilities, divided amongst the issuer’s PRC legal counsel, the issuer’s international legal counsel, the issuer’s Local Legal Counsel and Joint Lead Underwriter’s (JLU’s) PRC legal counsel based on the market practice.

在发行人需要所有交易文件均为中英文版的情况下,根据目前市场惯例,我们总结熊猫债券项目中发行人中国律师、发行人注册地律师和发行人国际律师以及承销商中国律师的简要分工。

Points to note:

另外,提示注意以下:

1.In the scenario that the issuer is a foreign governmental agency or an international development institution, the issuer’s Local Legal Counsel work could be undertaken by the issuer’s internal legal counsel.

在发行人为政府类机构或国际开发机构的情况下,发行人注册地律师的工作可由发行人的内部法律顾问承担;

2.In practice, the issuer’s international legal counsel and their Local Legal Counsel may actually be branches of the same law firm, but with offices in different jurisdictions; where the international legal counsel is not engaged by the issuer, any work that is the responsibility of the issuer’s international legal counsel could be undertaken by the issuer’s PRC legal counsel.

发行人国际律师与发行人注册地律师可以为同一家;在没有发行人国际律师的情况下,发行人国际律师的工作将由发行人中国律师和发行人注册地律师或发行人内部法律顾问承担;

3.Publicly-listed issuers will need to engage legal counsel from the jurisdictions of both its incorporation and listing place.

对于已上市的发行人且上市地与注册地不一致的,发行人还需要聘用上市地律师;

4.In practice, the JLU may not engage PRC legal counsel as their internal control department and the legal department of some JLUs may not require the JLU to engage PRC legal counsel.

实践中,如果承销商内审及法律部门没有特别要求,承销商可以不聘用律师。

Division of Work

1. A Panda bond is a Chinese RMB-denominated bond from a non-Chinese issuer

熊猫债券方兴未艾——从中国法律角度简析熊猫债券的申请和发行

On September 8, 2018, the People’s Bank of China (the “PBOC”) and the Ministry of Finance jointly promulgated the Interim Measures of the Administration of Offshore Institutions’ Bond Offering in National Interbank Bond Market (the “Interbank Panda Bond1 Measures”). The Interbank Panda Bond Measures and the Notice on Launching the Pilot Program of the Belt and Road Bonds (the “Notice on Stock Exchange Panda Bonds”) promulgated by the Shanghai Stock Exchange and Shenzhen Stock Exchange (collectively, the “Stock Exchanges”) in March 2018 constitute the main legal sources for offshore institutions’ Panda Bond offerings on the interbank bond market and stock exchange bond market respectively. These two regulations together with the interbank bond market rules promulgated by the PBOC, the National Association of Financial Market Institutional Investors (“NAFMII”) and other stock exchange bond market rules promulgated by the China Securities Regulatory Commission (the “CSRC”) and stock exchanges form the preliminary legal framework for Panda Bonds. We understand that NAFMII is drafting the guidelines for the registration and issuance of bonds by foreign governmental agencies, international development agencies and non-financial corporations on the national interbank bond market. With the release of such guidelines, the legal supervision system of Panda Bonds will be more complete.

2018年9月8日,中国人民银行和财政部联合颁布了《全国银行间债券市场境外机构债券发行管理暂行办法》(以下简称“《银行间熊猫债券办法》”),该办法与上海证券交易所和深圳证券交易所(以下合称“交易所”)于2018年3月分别颁布的《关于开展“一带一路”债券业务试点的通知》(以下简称“《交易所熊猫债券通知》”),分别构成了境外机构在银行间债券市场和交易所债券市场申请发行熊猫债券的统领性法律文件;连同中国人民银行和中国银行间市场交易商协会(以下简称“交易商协会”)已发布的银行间债券市场规则,以及中国证券监督管理委员会(以下简称“中国证监会”)和交易所已发布的交易所债券市场规则,初步形成了熊猫债券的法律监管体系。我们理解,交易商协会正在制定外国政府类机构、国际开发机构、非金融企业法人等在全国银行间债券市场注册发行债券的业务指引,该等指引出台后,熊猫债券的监管体系将更加完善。

Based on the latest legislation, and our previous experience on relevant projects, we have summarized the key procedures and issues when applying for Panda Bonds issuance in this article.

本文依据熊猫债券发行的最新法规动态,并结合本所以往项目经验,从中国法律角度简要梳理了不同主体申请发行熊猫债券的基本流程以及需要关注的主要问题,以抛砖引玉,供相关熊猫债券市场参与者参考和讨论。

I.General Procedures for Issuing Panda Bonds on the Interbank Bond Market

银行间债券市场熊猫债券基本流程

Please find below the governing authority, registration/approval procedures and qualifications for different types of issuers to issue Panda Bonds on interbank bond market.

依据发行主体的不同,我们梳理了如下银行间债券市场熊猫债发行项目的主管及审批程序。

1. Non-financial corporate issuers

发行人为非金融企业

2. Foreign governmental agency and international development institution issuers

发行人为外国政府类机构、国际开发机构

3. Financial Institution issuers

发行人为金融机构

II.General Procedures for Panda Bonds Issuance in the Stock Exchange Bond Market

交易所债券市场熊猫债券基本流程

Pursuant to the Notice on Stock Exchange Panda Bonds, national or regional governmental agencies, non-financial corporations and financial institutions within the “Belt and Road” region can apply to the Stock Exchange for the issuance of “Belt and Road” Panda Bonds. Currently, all Panda Bonds issuers in the stock exchange bond market are non-financial corporations; to date, no financial institution, governmental agency or international development institution has issued Panda Bonds on the stock exchange bond market. We understand that the following list applies to both non-financial corporations and to financial institutions.

根据《交易所熊猫债券通知》,“一带一路”沿线国家(地区)政府机构、一般企业和金融机构均可向交易所申请发行“一带一路”熊猫债券。目前,交易所市场仅有非金融企业发行的先例,无金融机构和外国主权类机构、国际开发机构发行的先例。与银行间债券市场不同,交易所债券市场熊猫债券并未依据发行主体的不同区分主管部门及审批程序,仅因发行方式的不同有所区别:

III.Key Issues for Panda Bond Issuance Applications

申请发行熊猫债券需要关注的主要问题

1. Accounting principles and auditing

会计准则和审计问题

The requirements regarding the accounting principles and auditing applicable to international development institutions, foreign governmental agencies, offshore financial institutions and non-financial corporates, and the filing requirements for offshore accounting firms as specified in the Interbank Panda Bond Measures are as follows:

《银行间熊猫债券办法》对国际开发机构、境外金融机构法人和非金融企业法人适用的会计准则、审计及会计师事务所报备要求如下:

Differences in the accounting principles adopted by Panda Bond issuers and CASBE have been a long-running obstacle deterring many potential Panda Bond issuers. Prior to the promulgation of Interbank Panda Bond Measures, the only accounting principles that had been accredited by the Ministry of Finance as being equivalent to CASBE were the International Financial Reporting Standards adopted by EU listed companies for their consolidated financial reports, and the Hong Kong Accounting Standards for Business Enterprises. Since there are only a limited number of Panda Bond issuers using these equivalent account principles, many potential Panda Bond issuers put their issuance plans on hold. The Interbank Panda Bond Measures allow issuers using non-equivalent accounting principles to apply for public issuance if they provide relevant supplementary information; issuers who find it difficult to provide such supplementary information may choose private placement as an alternative.

一直以来,熊猫债券发行人适用的会计准则与中国企业会计准则的差异处理是诸多熊猫债券发行中的难题。《银行间熊猫债券办法》出台前,经财政部认定已与中国企业会计准则实行等效的会计准则仅包括欧盟成员国上市公司在合并财务报表层面所采用的国际财务报告准则以及香港企业会计准则,而适用上述等效会计准则的熊猫债券发行人数量有限,导致许多有意向发行熊猫债券的发行人的发行计划因此搁置。《银行间熊猫债券办法》出台后,明确了使用非等效会计准则的发行人在公开发行时补充相关信息后可申请发行,同时如发行人认为补充信息有困难的,也可以选择定向发行的方式。

2. Panda Bond Tax Issues

发行和投资熊猫债券的税务问题

(1) Income tax

所得税

Only when the issuer and the investor are both non-PRC resident enterprises can bond interest be exempted from PRC enterprise income tax. For any income earned through the transfer of bonds, if the investor is a PRC resident enterprise, such investor is required to pay Chinese enterprise income tax. It should be noted that if the offshore investor is registered outside of China but has de facto management bodies in China, such investor will still be treated as a PRC resident enterprise and will thus be subject to Chinese enterprise income tax.

对于债息所得,只有发行人和投资者均为中国非居民企业的情况下,才免于中国企业所得税纳税义务;对于转让价差所得,在投资者为中国居民企业的情况下将产生中国企业所得税纳税义务。值得注意的是,境外投资者虽然注册在境外,但如果其实际管理机构位于境内,其仍然构成中国企业所得税法下的中国居民企业,从而产生中国企业所得税纳税义务。

(2) Value-added tax

增值税

Under PRC value-added tax law, an offshore investor’s transfer of Panda Bonds constitutes a financial product transfer service. If the transferee is located outside of China, the offshore investor’s income earned from such transfer is not subject to PRC value-added tax. If the transferee is located within China, the offshore investor’s income earned from such transfer is subject to PRC value-added tax. Certain offshore investors accredited by the PBOC may be exempt from such value-added tax.

境外投资者转让熊猫债券属于提供中国增值税法规规定的金融商品转让服务,如果熊猫债券的受让方在中国境外,境外投资者的转让收入依法不需要缴纳中国增值税;如果熊猫债券的受让方在中国境内,境外投资者的转让收入依法应当缴纳中国增值税,但是境外投资者属于经中国人民银行认可的境外机构,可以免于缴纳增值税。

For further details on Panda Bond-related tax matters, please refer to a previous JunHe Bulletin: Tax Analysis of Offshore Investors’ Investment in Panda Bonds.

关于熊猫债券涉税问题的详细分析,可参考本所此前的研究简讯《境外投资者投资“熊猫债”涉税问题简析》。

When issuing bonds, Panda Bond issuers should also consider the tax laws and regulations of their home country or jurisdiction.

另外,熊猫债券发行人应同时考虑所在国家或地区对债券发行及债券投资的税务征收法律法规。

3. Governing Law and Dispute Resolution

适用法律和争议解决相关问题

The Interbank Panda Bond Measures do not explicitly detail the applicable laws or dispute resolution mechanisms for Panda Bonds. Panda Bond issuers unfamiliar with PRC laws but with extensive experience offering bonds on international capital markets may assume that they can apply non-PRC regulations as the applicable laws and arbitration option should a dispute arise in the course of Panda Bond issuance.

《银行间熊猫债券办法》未明确规定熊猫债券发行及交易文件的适用法律及争议解决机制。部分熊猫债券发行人由于对中国法律不甚了解,且在境外资本市场有丰富的债券发行经验,希望熊猫债券发行及交易文件适用其惯用选择的外国法并在国外进行仲裁。

However, based on the current practice, even though the Interbank Panda Bond Measures do not explicitly detail the applicable laws or dispute resolution mechanisms, the competent authorities still require the transaction documents of Panda Bond issuance to be governed by PRC law and for the resolution of any dispute, including the litigation and arbitration, to be resolved in China.

但是,从目前实践来看,虽《银行间熊猫债券办法》对适用法律和争议解决未作出明确规定,主管机关仍要求熊猫债券发行及交易文件适用中国法律并选择在中国进行争议解决(包括诉讼和仲裁)。

4. Guarantee Structure

担保结构发行相关问题

In order to differentiate the group’s business activities from their financing activities, for the purposes of financing, some corporate groups may establish a special-purpose vehicle (“SPV”) on international markets. The SPV acts as the issuer, the parent company provides a joint liability guarantee for its bond issuance and the proceeds are for the group’s business operations. These issuers may wish to adopt the same guarantee structure when issue Panda Bonds in China.

在国际资本市场,部分集团公司会选择设立特殊目的子公司用于集中融资,将业务活动和融资活动相分离。在此结构下,特殊目的子公司作为发行人发行债券,由集团母公司提供连带责任担保,募集资金用于集团公司业务经营。该等集团公司在中国境内发行熊猫债券,通常也希望采取同样的担保结构发行。

While the Interbank Panda Bond Measures do not specify the option for the above-mentioned guarantee structure, we understand that under certain circumstances, such guarantee structure could possibly be adopted for a bond issue. Since in this structure, the issuer is solely reliant upon the guarantor’s credit to issue bonds, any requirements showing the issuer’s qualifications, their application documents and information disclosure will be equally applicable to the guarantor.

虽然《银行间熊猫债券办法》未明确规定担保结构,但我们理解在一定条件下可以采用上述担保结构发行,由于在此等结构下发行人主要依赖担保人的信用发债,对发行人的资格条件、申请文件和信息披露等要求,担保人应同样适用。

In addition, the proceeds raised by non-financial institutions should not be used as loans to other entities. Under the guarantee structure, proceeds are not normally used by the issuer itself or by its consolidated subsidiaries. Instead, the proceeds are used by the guarantor (generally the parent of the issuer) or the guarantor’s consolidated subsidiaries (i.e. the sister companies of the issuer). There is a need for further clarification from the governing authorities as to what will be the requirements for proceeds loaned to the parent or sister companies.

另外,非金融企业发行债券的募集资金不能用于借贷,在上述担保结构下,募集资金一般并非用于发行人自身或其合并报表范围内子公司,而是用于担保人(一般为发行人的母公司)或其子公司,满足何种标准才能允许该等募集资金使用路径,仍有待与主管机关沟通并进一步澄清。

5. Issuers of Panda Bonds on the Stock Exchanges

交易所熊猫债券的发行主体问题

Pursuant to the Notice on Stock Exchange Panda Bonds, foreign governmental agencies, non-financial corporations and financial institutions may apply to the Stock Exchanges to issue Panda Bonds. Currently, all issuers of Panda Bonds on the Stock Exchanges are offshore non-financial corporations. To date, no offshore financial institution has offered Panda Bonds on the Stock Exchanges, and there are no prevailing laws and regulations to prevent them from doing so. However, in practice, since financial institutions mainly issue bonds on the interbank bond market and the use of proceeds requires pre-approval from the PBOC, if an offshore financial institution plans to issue Panda Bonds on the Stock Exchanges, it should discuss in advance the feasibility of an issuance with the PBOC, the CSRC and the Stock Exchanges.

按照《交易所熊猫债券通知》,政府机构、一般企业和金融机构均可向交易所申请发行熊猫债券,但目前交易所市场发行熊猫债券的主体均为境外非金融机构,尚未有境外金融机构于交易所市场发行熊猫债券的先例。现行法律法规并未禁止境外金融机构于交易所市场发行熊猫债券,但实践中因金融机构主要于银行间债券市场发行债券,且募集资金使用将涉及中国人民银行事先同意等原因,境外金融机构如计划于交易所市场发行熊猫债券,应当提前与中国人民银行、中国证监会及交易所事先沟通发行方案的可行性。

6. Division of Legal Work on Panda Bond Projects

熊猫债券项目律师分工问题

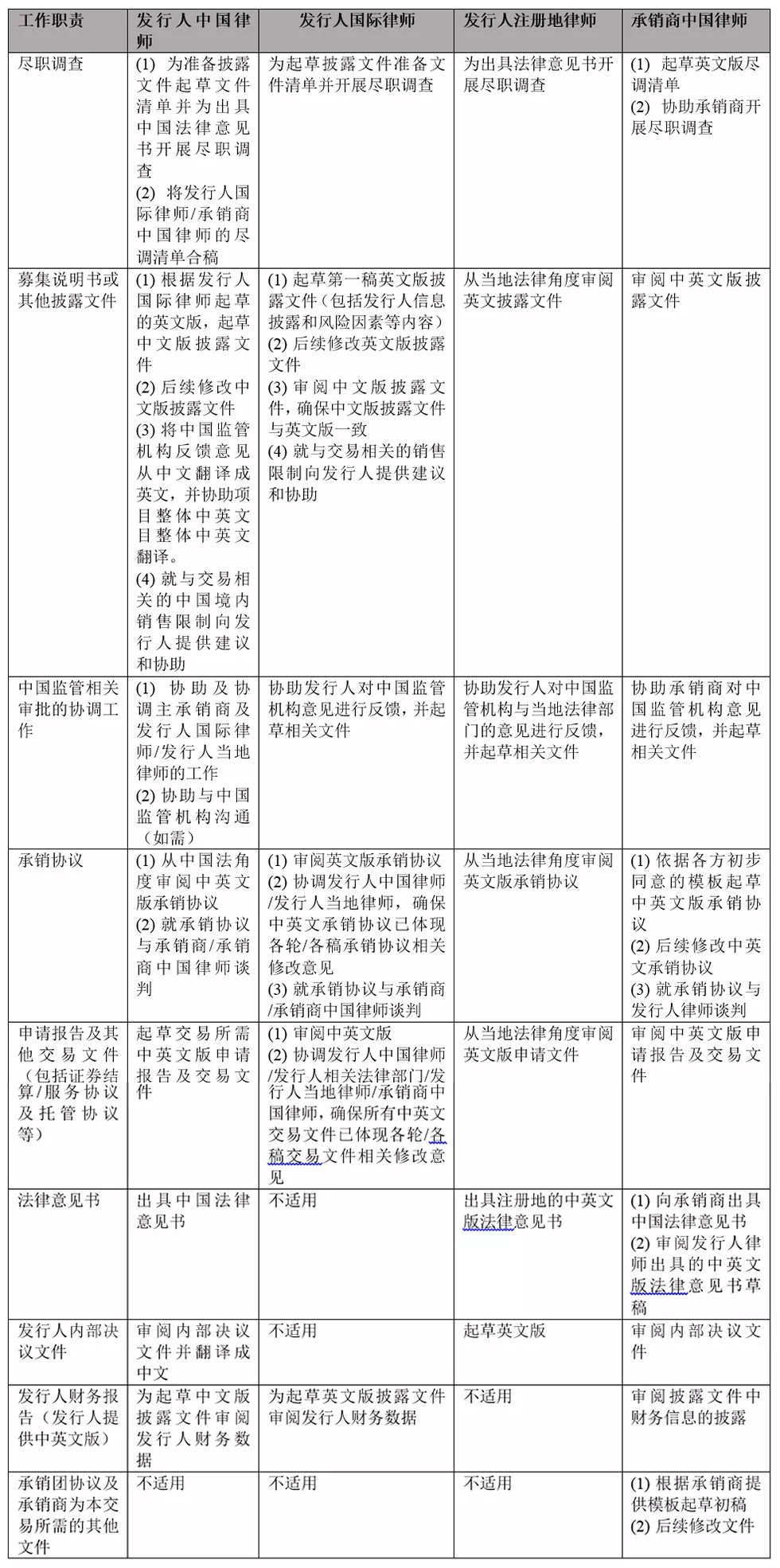

Given that all issuers of Panda Bonds are registered offshore, there will likely be multiple law firms providing legal advice to the issuer. In those cases where the issuer’s place of registration and the place of listing are in different jurisdictions, there could be up to five or more law firms involved, including the issuer’s PRC legal counsel, their international legal counsel, the legal counsel from the issuer’s jurisdiction of incorporation (or internal legal counsel) (the “Local Legal Counsel”), the legal counsel in their place of listing and the underwriter’s PRC legal counsel. In order to manage the legal activities on Panda Bond issues, there would generally be two law firms involved, i.e., the issuer’s PRC legal counsel and their Local legal counsel. Please refer to Appendix I of this article for more details on the responsibilities and division of work among the relevant law firms.

熊猫债券项目因发行人注册在境外,往往会涉及多家律师事务所共同为发行人提供法律服务的情况。在发行人注册地与上市地在不同法域的情况下,可能多达五家律师所,比如发行人境内律师、发行人国际律师、发行人注册地律师(或内部法律顾问)、发行人上市地律师和承销商境内律师,但一般是二家律师所参与,即发行人境内律师和发行人当地律师。各律师所的职责和分工请见本文的附件一。

Appendix I

List of Division of Work amongst Legal Counsels for Panda Bond Issuances

附件一:熊猫债券发行项目中各方律师分工

Under the assumption that the issuer would need both English and Chinese versions of the transaction documents, we have summarized the list of tasks and responsibilities, divided amongst the issuer’s PRC legal counsel, the issuer’s international legal counsel, the issuer’s Local Legal Counsel and Joint Lead Underwriter’s (JLU’s) PRC legal counsel based on the market practice.

在发行人需要所有交易文件均为中英文版的情况下,根据目前市场惯例,我们总结熊猫债券项目中发行人中国律师、发行人注册地律师和发行人国际律师以及承销商中国律师的简要分工。

Points to note:

另外,提示注意以下:

1.In the scenario that the issuer is a foreign governmental agency or an international development institution, the issuer’s Local Legal Counsel work could be undertaken by the issuer’s internal legal counsel.

在发行人为政府类机构或国际开发机构的情况下,发行人注册地律师的工作可由发行人的内部法律顾问承担;

2.In practice, the issuer’s international legal counsel and their Local Legal Counsel may actually be branches of the same law firm, but with offices in different jurisdictions; where the international legal counsel is not engaged by the issuer, any work that is the responsibility of the issuer’s international legal counsel could be undertaken by the issuer’s PRC legal counsel.

发行人国际律师与发行人注册地律师可以为同一家;在没有发行人国际律师的情况下,发行人国际律师的工作将由发行人中国律师和发行人注册地律师或发行人内部法律顾问承担;

3.Publicly-listed issuers will need to engage legal counsel from the jurisdictions of both its incorporation and listing place.

对于已上市的发行人且上市地与注册地不一致的,发行人还需要聘用上市地律师;

4.In practice, the JLU may not engage PRC legal counsel as their internal control department and the legal department of some JLUs may not require the JLU to engage PRC legal counsel.

实践中,如果承销商内审及法律部门没有特别要求,承销商可以不聘用律师。

Division of Work

1. A Panda bond is a Chinese RMB-denominated bond from a non-Chinese issuer